Sara Lee 2009 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2009 Sara Lee annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

|

|

During the third quarter of 2009, the corporation approved a

change to its U.S. postretirement medical plan. Effective January 1,

2010 the corporation will no longer subsidize retiree medical cover-

age for U.S. salaried employees and retirees. After this date, retirees

will have access to medical coverage but will have to pay 100% of

the premium. This change resulted in the recognition of a negative

plan amendment which is discussed in more detail below.

On June 30, 2007, the corporation adopted certain of the

provisions of new accounting rules related to an employers’ account-

ing for defined benefit pension and other postretirement plans. See

Note 2 – “Summary of Significant Accounting Policies” for additional

information regarding the impact of the adoption of these new

accounting rules and the related disclosure requirements.

Measurement Date and Assumptions Beginning in 2009, a fiscal

year end measurement date is utilized to value plan assets and

obligations for the corporation’s postretirement health-care and life-

insurance plans pursuant to the new accounting rules. Previously,

the corporation used a March 31 measurement date. The impact

of adopting the new measurement date provision was recorded in

2009 as an adjustment to beginning of year retained earnings of

$(1), net of tax. The adjustment to retained earnings represents

the net periodic benefit costs for the period from March 28, 2008

to June 28, 2008, the end of the previous fiscal year, which was

determined using the 15-month approach to proportionally allocate

the net periodic benefit cost to this period.

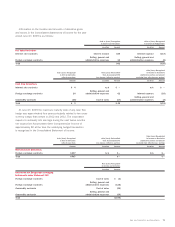

The weighted average actuarial assumptions used in measuring

the net periodic benefit cost and plan obligations for the three

years ending June 28, 2008 were:

2009 2008 2007

Net periodic benefit cost

Discount rate 6.4% 5.7% 5.5%

Plan obligations

Discount rate 6.3 6.4 5.7

Health-care cost trend assumed

for the next year 8.5 9.5 9.5

Rate to which the cost trend is

assumed to decline 5.0 5.5 5.5

Year that rate reaches the

ultimate trend rate 2016 2015 2015

The discount rate is determined by utilizing a yield curve based

on high-quality fixed-income investments that have an AA bond rating

to discount the expected future benefit payments to plan participants.

Assumed health-care trend rates are based on historical experience

and management’s expectations of future cost increases. A one-

percentage-point change in assumed health-care cost trend rates

would have the following effects:

One One

Percentage Percentage

Point Point

Increase Decrease

Effect on total service and interest components $÷2 $÷(2)

Effect on postretirement benefit obligation 15 (13)

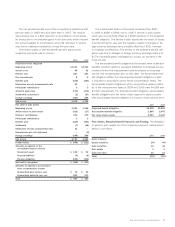

Net Periodic Benefit Cost and Funded Status The components of

the net periodic benefit cost and curtailment gains associated with

continuing operations were as follows:

2009 2008 2007

Components of defined benefit

net periodic cost

Service cost $÷«7 $÷«8 $÷«8

Interest cost 13 16 13

Net amortization and deferral (23) (18) (22)

Net periodic benefit cost (income) $÷(3) $÷«6 $÷(1)

Curtailment (gains) $(17) $÷«– $÷(2)

The reduction in net periodic benefit costs in 2009 was driven

by lower interest costs as a result of the lower accumulated benefit

obligation at the start of the year as compared to the prior year,

and an increase in net amortization and deferral income due to an

increase in amortization of unamortized prior service cost credits

and a reduction in amortization related to the net initial asset.

The amount of the prior service credits, net actuarial loss

and net initial asset that is expected to be amortized from accumu-

lated other comprehensive income and reported as a component

of net periodic benefit cost during 2010 is $5 of income, nil and

nil, respectively.

Sara Lee Corporation and Subsidiaries 79