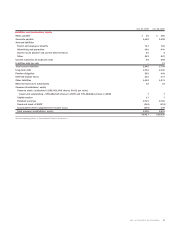

Sara Lee 2009 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2009 Sara Lee annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

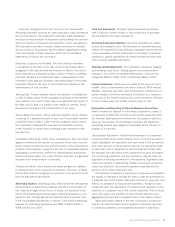

Sales are recognized as the net amount to be received after

deducting estimated amounts for sales incentives, trade allowances

and product returns. The corporation estimates trade allowances

and product returns based on historical results taking into consider-

ation the customer, transaction and specifics of each arrangement.

The corporation provides a variety of sales incentives to resellers

and consumers of its products, and the policies regarding the recog-

nition and display of these incentives within the Consolidated

Statements of Income are as follows:

Discounts, Coupons and Rebates

The cost of these incentives

is recognized at the later of the date at which the related sale is

recognized or the date at which the incentive is offered. The cost of

these incentives is estimated using a number of factors, including

historical utilization and redemption rates. Substantially all cash

incentives of this type are included in the determination of net sales.

Incentives offered in the form of free product are included in the

determination of cost of sales.

Slotting Fees

Certain retailers require the payment of slotting fees

in order to obtain space for the corporation’s products on the retailer’s

store shelves. The cost of these fees is recognized at the earlier of

the date cash is paid or a liability to the retailer is created. These

amounts are included in the determination of net sales.

Volume-Based Incentives

These incentives typically involve rebates

or refunds of a specified amount of cash only if the reseller reaches

a specified level of sales. Under incentive programs of this nature,

the corporation estimates the incentive and allocates a portion

of the incentive to reduce each underlying sales transaction with

the customer.

Cooperative Advertising

Under these arrangements, the corporation

agrees to reimburse the reseller for a portion of the costs incurred

by the reseller to advertise and promote certain of the corporation’s

products. The corporation recognizes the cost of cooperative advertis-

ing programs in the period in which the advertising and promotional

activity first takes place. The costs of these incentives are generally

included in the determination of net sales.

Fixtures and Racks

Store fixtures and racks are given to retailers

to display certain of the corporation’s products. The costs of these

fixtures and racks are recognized as expense in the period in which

they are delivered to the retailer.

Advertising Expense Advertising costs, which include the development

and production of advertising materials and the communication of

this material through various forms of media, are expensed in the

period the advertising first takes place. Advertising expense is rec-

ognized in the “Selling, general and administrative expenses” line

in the Consolidated Statements of Income. Total media advertising

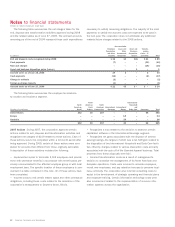

expense for continuing operations was $282 in 2009, $325 in

2008 and $313 in 2007.

Cash and Equivalents All highly liquid investments purchased

with a maturity of three months or less at the time of purchase

are considered to be cash equivalents.

Accounts Receivable Valuation Accounts receivable are stated

at their net realizable value. The allowance for doubtful accounts

reflects the corporation’s best estimate of probable losses inherent

in the receivables portfolio determined on the basis of historical

experience, specific allowances for known troubled accounts and

other currently available information.

Shipping and Handling Costs The corporation recognizes shipping

and handling costs in the “Selling, general and administrative

expenses” line of the Consolidated Statements of Income and

recognized $693 in 2009, $703 in 2008 and $656 in 2007.

Inventory Valuation Inventories are stated at the lower of cost or

market. Cost is determined by the first-in, first-out (FIFO) method.

Rebates, discounts and other cash consideration received from a

vendor related to inventory purchases is reflected as a reduction

in the cost of the related inventory item, and is therefore, reflected

in cost of sales when the related inventory item is sold.

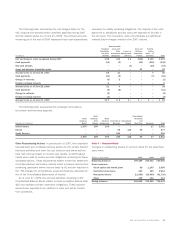

Recognition and Reporting of Planned Business Dispositions

When a decision to dispose of a business component is made, it

is necessary to determine how the results will be presented within

the financial statements and whether the net assets of that busi-

ness are recoverable. The following summarizes the significant

accounting policies and judgments associated with a decision to

dispose of a business.

Discontinued Operations

A discontinued operation is a business

component that meets several criteria. First, it must be possible to

clearly distinguish the operations and cash flows of the component

from other portions of the business. Second, the operations need

to have been sold or classified as held for disposal. Finally, after

the disposal, the cash flows of the component must be eliminated

from continuing operations and the corporation may not have any

significant continuing involvement in the business. Significant judg-

ments are involved in determining whether a business component

meets the criteria for discontinued operation reporting and the

period in which these criteria are met.

If a business component is reported as a discontinued operation,

the results of operations through the date of sale are presented on

a separate line of the income statement. Interest on corporate level

debt is not allocated to discontinued operations. Any gain or loss

recognized upon the disposition of a discontinued operation is also

reported on a separate line of the income statement. Prior to dispo-

sition, the assets and liabilities of discontinued operations are

aggregated and reported on separate lines of the balance sheet.

Gains and losses related to the sale of business components

that do not meet the discontinued operation criteria are reported

in continuing operations and separately disclosed if significant.

Sara Lee Corporation and Subsidiaries 53