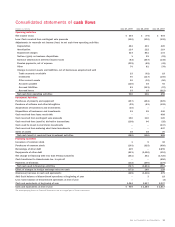

Sara Lee 2009 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2009 Sara Lee annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

ations involving the interpretation of complex income tax laws in

the context of our fact patterns. Any adjustment to a tax reserve

impacts the corporation’s tax expense in the period in which the

adjustment is made.

As a global commercial enterprise, the corporation’s tax rate from

period to period can be affected by many factors. The most significant

of these factors are changes in tax legislation, the corporation’s

global mix of earnings, the tax characteristics of the corporation’s

income, the timing and recognition of goodwill impairments, acquisi-

tions and dispositions, adjustments to the corporation’s reserves

related to uncertain tax positions, changes in valuation allowances,

and the portion of the income of foreign subsidiaries that is expected

to be remitted to the U.S. and be taxable. It is reasonably possible

that the following items can have a material impact on income tax

expense, net income and liquidity in future periods:

•The spin off of the Hanesbrands business that was completed

in 2007 has resulted in, and may continue to result in, an increase

in the corporation’s effective tax rate in future years as the opera-

tions that were spun off had, historically, a lower effective tax rate

than the remainder of the business and generated a significant

amount of operating cash flow. The elimination of this cash flow

has required the corporation to remit a greater portion of the future

foreign earnings to the U.S. than has historically been the case and

resulted in higher levels of tax expense and cash taxes paid. The

tax provision associated with the repatriation of foreign earnings for

fiscal years 2009, 2008, and 2007 was $58 million, $118 million,

and $194 million, respectively. However, a significant portion of the

corporation’s foreign earnings are permanently reinvested in its

foreign subsidiaries. In its determination of which foreign earnings

are permanently reinvested, the corporation considers numerous

factors, including the financial requirements of the U.S. parent

company, the financial requirements of its foreign subsidiaries, and

the tax consequences of remitting the foreign earnings to the U.S.

Variability in the corporation’s effective tax rate will occur over time

as a result of these and other factors which could materially change

the estimated cost of future repatriation actions.

•Tax legislation in the jurisdictions in which the corporation does

business may change in future periods. While such changes cannot

be predicted, if they occur, the impact on the corporation’s tax

assets and obligations will need to be measured and recognized

in the financial statements.

•The corporation has ongoing U.S. and foreign tax audits for various

tax periods. The U.S. federal tax years from 2005 onward remain

subject to audit. Fiscal years remaining open to examination in the

Netherlands include 2003 forward. Other foreign jurisdictions remain

open to audits ranging from 1999 forward. With few exceptions,

the corporation is no longer subject to state and local income tax

examinations by tax authorities for years before 2003. The tax

reserves for uncertain tax positions recorded in the financial state-

ments reflect the expected finalization of worldwide examinations.

The corporation regularly reviews its tax positions based on the

individual facts, circumstances, and technical merits of each tax

position. If the corporation determines it is more likely than not that

it is entitled to the economic benefits associated with a tax position,

it then considers the amounts and probabilities of the outcomes

that could be realized upon ultimate settlement with a taxing

authority, taking into consideration all available facts, circumstances,

and information. The corporation believes that it has sufficient

cash resources to fund the settlement of these audits.

As a result of audit resolutions, expirations of statutes of limita-

tions, and changes in estimate on tax contingencies in 2009 and

2008, the corporation recognized tax benefits of $16 million

and $96 million, respectively. However, audit outcomes and the

timing of audit settlements are subject to significant uncertainty.

The corporation estimates reserves for uncertain tax positions, but

is not able to control or predict the extent to which tax authorities

will examine specific periods, the outcome of examinations, or the

time period in which examinations will be conducted and finalized.

Favorable or unfavorable past audit experience in any particular tax

jurisdiction is not indicative of the outcome of future examinations

by those tax authorities. Based on the nature of uncertain tax

positions and the examination process, management is not able

to predict the potential outcome with respect to tax periods that have

not yet been examined or the impact of any potential reserve

adjustments on the corporation’s tax rate or net earnings trends. As

of the end of 2009, the corporation believes that it is reasonably

possible that the liability for unrecognized tax benefits will decrease by

approximately $100 million to $160 million over the next 12 months.

•Facts and circumstances may change that cause the corporation

to revise the conclusions on its ability to realize certain net operating

losses and other deferred tax attributes. The corporation regularly

reviews whether it will realize its deferred tax assets. Its review

consists of determining whether sufficient taxable income of the

appropriate character exists within the carryback and carryforward

period available under respective tax statutes. The corporation

considers all available evidence of recoverability when evaluating

its deferred tax assets; however, the corporation’s most sensitive

and critical factor in determining recoverability of deferred tax

assets is the existence of historical and projected profitability in a

particular jurisdiction. As a result, changes in actual and projected

results of the corporation’s various legal entities can create variability,

Sara Lee Corporation and Subsidiaries 43