Pitney Bowes 2009 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2009 Pitney Bowes annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

25

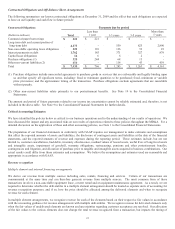

revenue recognition. Revenue is allocated to the meter rental and equipment maintenance agreement elements first using their

respective fair values, which are determined based on prices charged in standalone and renewal transactions. Revenue is then

allocated to the equipment based on the present value of the remaining minimum lease payments. We then compare the allocated

equipment fair value to the range of cash selling prices in standalone transactions during the period to ensure the allocated equipment

fair value approximates average cash selling prices.

We provide lease financing for our products primarily through sales-type leases. We classify our leases in accordance with the lease

accounting guidance. The vast majority of our leases qualify as sales-type leases using the present value of minimum lease payments

classification criteria. We believe that our sales-type lease portfolio contains only normal collection risk. Accordingly, we record the

fair value of equipment as sales revenue, the cost of equipment as cost of sales and the minimum lease payments plus the estimated

residual value as gross finance receivables. The difference between the gross finance receivable and the equipment fair value is

recorded as unearned income and is amortized as income over the lease term using the interest rate implicit in the lease.

Equipment residual values are determined at inception of the lease using estimates of equipment fair value at the end of the lease term.

Estimates of future equipment fair value are based primarily on our historical experience. We also consider forecasted supply and

demand for our various products, product retirement and future product launch plans, end of lease customer behavior, regulatory

changes, remanufacturing strategies, used equipment markets, if any, competition and technological changes. We evaluate residual

values on an annual basis or as changes to the above considerations occur.

See Note 1 to the Consolidated Financial Statements for our accounting policies on revenue recognition.

Allowances for doubtful accounts and credit losses

Allowance for doubtful accounts

We estimate our accounts receivable risks and provide allowances for doubtful accounts accordingly. We evaluate the adequacy of

the allowance for doubtful accounts based on our historical loss experience, length of time receivables are past due, adverse situations

that may affect a customer’s ability to pay and prevailing economic conditions. We make adjustments to our allowance if our

evaluation of allowance requirements differs from our actual aggregate reserve. This evaluation is inherently subjective because our

estimates may be revised as more information becomes available.

Allowance for credit losses

We estimate our finance receivables risks and provide allowances for credit losses accordingly. We establish credit approval limits

based on the credit quality of our customers and the type of equipment financed. We charge finance receivables to the allowance for

credit losses after collection efforts are exhausted and we deem the account uncollectible. We base credit decisions primarily on a

customer’s financial strength. We believe that our concentration of credit risk for finance receivables in our internal financing

division is limited because of our large number of customers, small account balances and customer geographic and industry

diversification. Our general policy for finance receivables contractually past due for over 120 days is to discontinue revenue

recognition. We resume revenue recognition when payments reduce the account to 60 days or less past due.

We evaluate the adequacy of allowance for credit losses based on our historical loss experience, the nature and volume of our

portfolios, adverse situations that may affect a customer’s ability to pay, estimated value of any underlying collateral and prevailing

economic conditions. We make adjustments to our allowance for credit losses if the evaluation of reserve requirements differs from

the actual aggregate reserve. This evaluation is inherently subjective because our estimates may be revised as more information

becomes available.

Accounting for income taxes

We are subject to income taxes in the U.S. and numerous foreign jurisdictions. When we prepare our consolidated financial

statements, we are required to estimate our income taxes in each of the jurisdictions in which we operate. We record this amount as a

provision for our taxes in accordance with the accounting for income taxes guidance.

In 2007, we adopted guidance addressing accounting for uncertainty in income taxes. The guidance defines the confidence level that a

tax position must meet in order to be recognized in the financial statements. The guidance requires a two-step approach under which

the tax effect of a position is recognized only if it is “more-likely-than-not” to be sustained and the amount of the tax benefit

recognized is equal to the largest tax benefit that is greater than 50 percent likely of being realized upon ultimate settlement of the tax

position. This is a different standard for recognition than the approach previously required. Both approaches require us to exercise

considerable judgment and estimates are inherent in both processes.