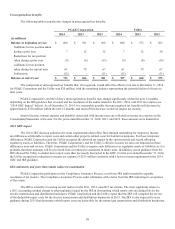

PG&E 2014 Annual Report Download - page 112

Download and view the complete annual report

Please find page 112 of the 2014 PG&E annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

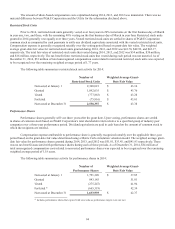

|

|

104

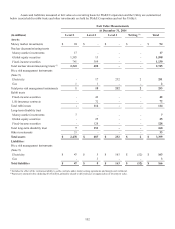

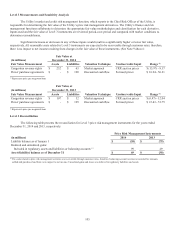

Valuation Techniques

The following describes the valuation techniques used to measure the fair value of the assets and liabilities shown in

the tables above. Investments, primarily consisting of equity securities, that are valued using a net asset value per share can be

redeemed quarterly with notice not to exceed 90 days. Equity investments valued at net asset value per share utilize investment

strategies aimed at matching the performance of indexed funds. Transfers between levels in the fair value hierarchy are recognized

as of the end of the reporting period. There were no material transfers between any levels for the year ended December 31, 2014

and 2013.

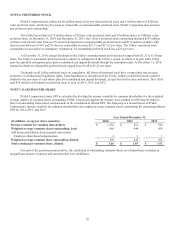

Trust Assets

Nuclear decommissioning trust assets and other trust assets are composed primarily of equity securities, debt securities,

and life insurance policies. In general, investments held in the trusts are exposed to various risks, such as interest rate, credit, and

market volatility risks.

Global equity securities primarily include investments in common stock that are valued based on quoted prices in active

markets and are classified as Level 1. Equity securities also include commingled funds that are composed of equity securities

traded publicly on exchanges across multiple industry sectors in the U.S. and other regions of the world. Investments in these funds

are classified as Level 2 because price quotes are readily observable and available.

Debt securities are primarily composed of U.S. government and agency securities, municipal securities, and other fixed-

income securities, including corporate debt securities. U.S. government and agency securities primarily consist of U.S. Treasury

securities that are classified as Level 1 because the fair value is determined by observable market prices in active markets. A

market approach is generally used to estimate the fair value of debt securities classified as Level 2 using evaluated pricing data

such as broker quotes, for similar securities adjusted for observable differences. Significant inputs used in the valuation model

generally include benchmark yield curves and issuer spreads. The external credit ratings, coupon rate, and maturity of each security

are considered in the valuation model, as applicable.

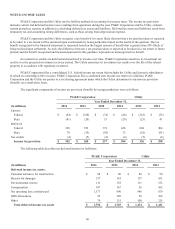

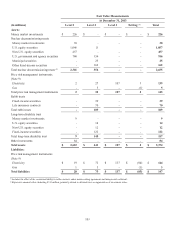

Price Risk Management Instruments

Price risk management instruments include physical and financial derivative contracts, such as power purchase

agreements, forwards, swaps, options, and CRRs that are traded either on an exchange or over-the-counter.

Power purchase agreements, forwards, and swaps are valued using a discounted cash flow model. Exchange-traded

forwards and swaps that are valued using observable market forward prices for the underlying commodity are classified as Level 1.

Over-the-counter forwards and swaps that are identical to exchange-traded forwards and swaps, or are valued using forward prices

from broker quotes that are corroborated with market data are classified as Level 2. Exchange-traded options are valued using

observable market data and market-corroborated data and are classified as Level 2.

Long-dated power purchase agreements that are valued using significant unobservable data are classified as Level 3.

These Level 3 contracts are valued using either estimated basis adjustments from liquid trading points or techniques, including

extrapolation from observable prices, when a contract term extends beyond a period for which market data is available. Market and

credit risk management utilizes models to derive pricing inputs for the valuation of the Utility’s Level 3 instruments using pricing

inputs from brokers and historical data.

The Utility holds CRRs to hedge the financial risk of CAISO-imposed congestion charges in the day-ahead market. CRRs

are classified as Level 3 and are valued based on CRR auction prices, including historical prices. Limited market data is available

in the CAISO auction and between auction dates; therefore, the Utility uses models to forecast CRR prices for those periods not

covered in the auctions.