PG&E 2014 Annual Report Download - page 109

Download and view the complete annual report

Please find page 109 of the 2014 PG&E annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

101

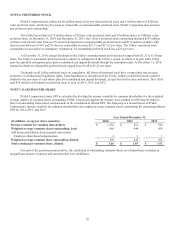

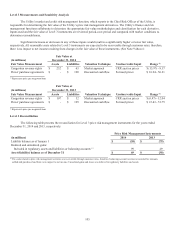

Cash inflows and outflows associated with derivatives are included in operating cash flows on the Utility’s Consolidated

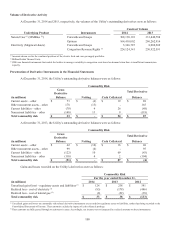

Statements of Cash Flows.

The majority of the Utility’s derivatives contain collateral posting provisions tied to the Utility’s credit rating from each

of the major credit rating agencies. At December 31, 2014, the Utility’s credit rating was investment grade. If the Utility’s credit

rating were to fall below investment grade, the Utility would be required to post additional cash immediately to fully collateralize

some of its net liability derivative positions.

The additional cash collateral that the Utility would be required to post if the credit risk-related contingency features were

triggered was as follows:

Balance at December 31,

(in millions) 2014 2013

Derivatives in a liability position with credit risk-related

contingencies that are not fully collateralized $ (47) $ (79)

Related derivatives in an asset position - 4

Collateral posting in the normal course of business related to

these derivatives 44 65

Net position of derivative contracts/additional collateral

posting requirements (1) $ (3) $ (10)

(1) This calculation excludes the impact of closed but unpaid positions, as their settlement is not impacted by any of the Utility’s credit risk-related contingencies.

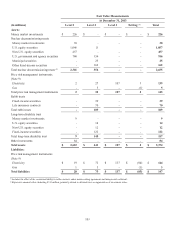

NOTE 10: FAIR VALUE MEASUREMENTS

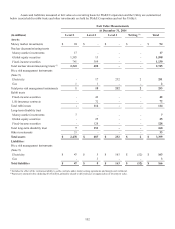

PG&E Corporation and the Utility measure their cash equivalents, trust assets, price risk management instruments, and

other investments at fair value. A three-tier fair value hierarchy is established that prioritizes the inputs to valuation methodologies

used to measure fair value:

Level 1 – Observable inputs that reect quoted prices (unadjusted) for identical assets or liabilities in active markets.

Level 2 – Other inputs that are directly or indirectly observable in the marketplace.

Level 3 – Unobservable inputs which are supported by little or no market activities.

The fair value hierarchy requires an entity to maximize the use of observable inputs and minimize the use of unobservable

inputs when measuring fair value.