PG&E 2009 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2009 PG&E annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

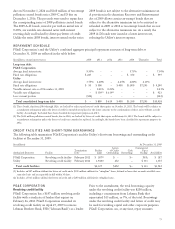

outstanding in whole or in part. At PG&E Corporation’s

request and at the sole discretion of each lender, the

revolving credit facility may be extended for additional

periods. PG&E Corporation has the right to increase, in

one or more requests given no more than once a year, the

aggregate facility by up to $100 million provided that

certain conditions are met. The fees and interest rates that

PG&E Corporation pays under the revolving credit facility

vary depending on the Utility’s unsecured debt ratings

issued by Standard & Poor’s (“S&P”) ratings service and

Moody’s Investors Service (“Moody’s”).

The revolving credit facility includes usual and

customary covenants for credit facilities of this type,

including covenants limiting liens, mergers, sales of all or

substantially all of PG&E Corporation’s assets, and other

fundamental changes. In general, the covenants,

representations, and events of default mirror those in the

Utility’s revolving credit facility, discussed below. In

addition, the revolving credit facility also requires that

PG&E Corporation maintain a ratio of total consolidated

debt to total consolidated capitalization of at most 65%

and that PG&E Corporation own, directly or indirectly, at

least 80% of the common stock and at least 70% of the

voting securities of the Utility. At December 31, 2009,

PG&E Corporation met both of these tests.

UTILITY

Revolving credit facility

The Utility has a $1.94 billion revolving credit facility with

a syndicate of lenders that expires on February 26, 2012.

The Utility amended its revolving credit facility on

April 27, 2009 to remove Lehman Bank as a lender. Prior

to the amendment, the total borrowing capacity under the

revolving credit facility was $2.0 billion, including a

commitment from Lehman Bank that represented $60

million, or 3%, of the total. Borrowings under the

revolving credit facility and letters of credit are used

primarily for liquidity and to provide credit enhancements

to counterparties for natural gas and energy procurement

transactions. The Utility treats the amount of its

outstanding commercial paper as a reduction to the

amount available under its revolving credit facility so that

liquidity from the revolving credit facility is available to

repay outstanding commercial paper.

The revolving credit facility includes usual and

customary covenants for credit facilities of this type,

including covenants limiting liens to those permitted under

the senior notes’ indenture, mergers, sales of all or

substantially all of the Utility’s assets, and other

fundamental changes. In addition, the revolving credit

facility also requires that the Utility maintain a debt to

capitalization ratio of at most 65% as of the end of each

fiscal quarter. At December 31, 2009, the Utility met this

ratio test.

Commercial Paper Program

The Utility has a $1.75 billion commercial paper program, the

borrowings from which are used primarily to cover

fluctuations in cash flow requirements. Liquidity support for

these borrowings is provided by available capacity under the

Utility’s revolving credit facility, as described above. The

commercial paper may have maturities up to 365 days and

ranks equally with the Utility’s other unsubordinated and

unsecured indebtedness. Commercial paper notes are sold at

an interest rate dictated by the market at the time of issuance.

At December 31, 2009, the average yield was 0.31%.

NOTE 5: ENERGY RECOVERY

BONDS

In 2005, PG&E Energy Recovery Funding, LLC (“PERF”), a

wholly owned consolidated subsidiary of the Utility, issued

two separate series of ERBs in the aggregate amount of $2.7

billion to refinance a regulatory asset that the Utility

recorded in connection with the Chapter 11 Settlement

Agreement. The proceeds of the ERBs were used by PERF

to purchase from the Utility the right, known as “recovery

property,” to be paid a specified amount from a dedicated

rate component (“DRC”) to be collected from the Utility’s

electricity customers. DRC charges are authorized by the

CPUC under state legislation and will be paid by the

Utility’s electricity customers until the ERBs are fully

retired. Under the terms of a recovery property servicing

agreement, DRC charges are collected by the Utility and

remitted to PERF for payment of principal, interest, and

miscellaneous expenses associated with the bonds.

The first series of ERBs issued on February 10, 2005

included five classes aggregating to a $1.9 billion principal

amount with scheduled maturities ranging from

September 25, 2006 to December 25, 2012. Interest rates

on the remaining three outstanding classes range from

4.14% for the earliest maturing class to 4.47% for the latest

maturing class. The proceeds of the first series of ERBs

were paid by PERF to the Utility and were used by the

Utility to refinance the remaining unamortized after-tax

balance of the settlement regulatory asset. The second

series of ERBs, issued on November 9, 2005, included

three classes aggregating to an $844 million principal

amount, with scheduled maturities ranging from June 25,

2009 to December 25, 2012. Interest rates on the remaining

two classes are 5.03% for the earliest maturing class and

5.12% for the latest maturing class. The proceeds of the

second series of ERBs were paid by PERF to the Utility to

pre-fund the Utility’s tax liability that will be due as the

Utility collects the DRC charges from customers.

74