PG&E 2009 Annual Report Download - page 102

Download and view the complete annual report

Please find page 102 of the 2009 PG&E annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

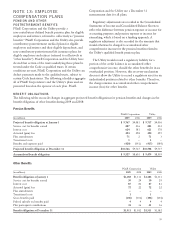

Employee Retirement Income Security Act of 1974. PG&E

Corporation’s and the Utility’s investment policies and

strategies are designed to increase the ratio of trust assets to

plan liabilities at an acceptable level of funded status

volatility.

Interest rate risk and equity risk are the key determinants

of PG&E Corporation’s and the Utility’s funded status

volatility. In addition to affecting the trust’s fixed income

portfolio market values, interest rate changes also influence

liability valuations as discount rates move with current

bond yields. To manage this risk, PG&E Corporation’s and

the Utility’s trusts hold significant allocations to fixed

income investments that include U.S. government

securities, corporate securities, and other fixed income

securities. Although they contribute to funded status

volatility, equity investments are held to reduce long-term

funding costs due to their higher expected return. The

equity investment allocation is implemented through

diversified U.S., non-U.S., and global portfolios that

include common stock and commingled funds across

multiple industry sectors. Absolute return investments

include hedge fund portfolios that are managed to diversify

the plan’s holdings in equity and fixed income investments

by exhibiting returns with low correlation to the direction

of these markets. Over the last three years, target

allocations to equity investments have generally declined in

favor of longer-maturity fixed income investments as a

means of dampening future funded status volatility.

PG&E Corporation and the Utility apply a risk

management framework for managing the risks associated

with employee benefit plan trust assets. The guiding

principles of this risk management framework are the clear

articulation of roles and responsibilities, appropriate

delegation of authority, and proper accountability and

documentation. Trust investment policies and investment

manager guidelines include provisions to ensure prudent

diversification, manage risk through appropriate use of

physical direct asset holdings and derivative securities, and

identify permitted and prohibited investments.

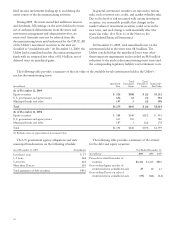

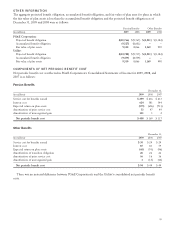

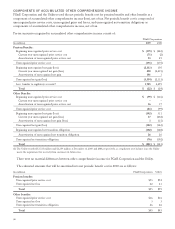

The target asset allocation percentages for major categories of trust assets for pension and other benefit plans at

December 31, 2010, 2009, and 2008 are as follows:

Pension Benefits Other Benefits

2010 2009 2008 2010 2009 2008

U.S. Equity 26% 32% 31% 26% 37% 35%

Non-U.S. Equity 14% 18% 17% 13% 18% 16%

Global Equity 5% 5% 3% 3% 3% 2%

Absolute Return 5% 5% 4% 3% 3% 3%

Fixed Income 50% 40% 42% 54% 34% 34%

Cash Equivalents 0% 0% 3% 1% 5% 10%

Total 100% 100% 100% 100% 100% 100%

Equity securities include a small amount (less than 0.1%

of total plan assets) of PG&E Corporation common stock.

The maturity of fixed income securities at December 31,

2009 ranged from less than one year to 88 years and the

average duration of the bond portfolio was approximately

10.6 years. The maturity of fixed income securities at

December 31, 2008 ranged from zero to 59 years and the

average duration of the bond portfolio was approximately

12.2 years.

98