Motorola 2010 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2010 Motorola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

|

|

89

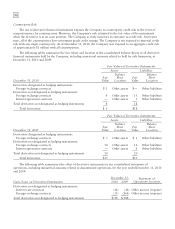

Company’s non-functional currency receivables and payables, which are primarily denominated in major currencies

that can be traded on open markets. The Company typically uses forward contracts and options to hedge these

currency exposures. In addition, the Company enters into derivative contracts for some forecasted transactions,

which are designated as part of a hedging relationship if it is determined that the transaction qualifies for hedge

accounting under the provisions of the authoritative accounting guidance for derivative instruments and hedging

activities. A portion of the Company’s exposure is from currencies that are not traded in liquid markets and these

are addressed, to the extent reasonably possible, by managing net asset positions, product pricing and component

sourcing.

At December 31, 2010, the Company had outstanding foreign exchange contracts totaling $1.5 billion,

compared to $1.7 billion outstanding at December 31, 2009. Management believes that these financial instruments

should not subject the Company to undue risk due to foreign exchange movements because gains and losses on these

contracts should generally offset losses and gains on the underlying assets, liabilities and transactions, except for the

ineffective portion of the instruments, which are charged to Other within Other income (expense) in the Company’s

consolidated statements of operations.

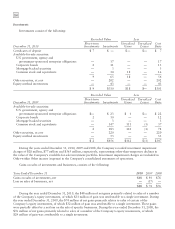

The following table shows the five largest net notional amounts of the positions to buy or sell foreign currency

as of December 31, 2010 and the corresponding positions as of December 31, 2009:

Notional Amount

Net Buy (Sell) by Currency

December 31,

2010

December 31,

2009

Brazilian Real $(429) $(342)

Chinese Renminbi (409) (297)

Euro (249) (377)

Malaysian Ringgit 64 16

British Pound 185 143

For the year ended December 31, 2010, income representing the ineffective portions of changes in the fair value

of cash flow hedge positions was $1 million compared to de minimus income for the year ended December 31, 2009

and expense of $2 million for the year ended December 31, 2008. These amounts are included in Other within

Other income (expense) in the Company’s consolidated statements of operations. The above amounts include the

change in the fair value of derivative contracts related to the changes in the difference between the spot price and the

forward price. These amounts are excluded from the measure of effectiveness. Expense (income) related to cash flow

hedges that were discontinued for the years ended December 31, 2010, 2009 and 2008 are included in the amounts

noted above.

During the years ended December 31, 2010, 2009 and 2008, on a pre-tax basis, income (expense) of

$(6) million, $(18) million and $3 million, respectively, was reclassified from equity to earnings in the Company’s

consolidated statements of operations.

At December 31, 2010, the maximum term of derivative instruments that hedge forecasted transactions was

12 months. The weighted average duration of the Company’s derivative instruments that hedge forecasted

transactions was six months.

Interest Rate Risk

At December 31, 2010, the Company has $2.8 billion of long-term debt, including the current portion of long-

term debt, which is primarily priced at long-term, fixed interest rates.

As part of its liability management program, one of the Company’s European subsidiaries has an outstanding

interest rate agreement (“Interest Agreement”) relating to a Euro-denominated loan. The interest on the Euro-

denominated loan is variable. The Interest Agreement changes the characteristics of interest rate payments from

variable to maximum fixed-rate payments. The Interest Agreement is not accounted for as a part of a hedging

relationship and, accordingly, the changes in the fair value of the Interest Agreement is included in Other income

(expense) in the Company’s consolidated statements of operations. The weighted average fixed rate payment on the

Interest Agreement was 5.18%. At December 31, 2010 and 2009, the fair value of the Interest Agreement put the

Company in a liability position of $3 million and $4 million, respectively.