Kroger 2010 Annual Report Download - page 119

Download and view the complete annual report

Please find page 119 of the 2010 Kroger annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

|

|

A-39

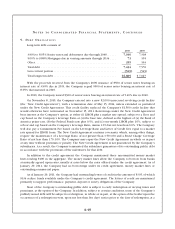

NO T E S T O CO N S O L I D A T E D FI N A N C I A L ST A T E M E N T S , CO N T I N U E D

value of the division’s goodwill. Goodwill impairment is recognized for any excess of the carrying value of

the division’s goodwill over the implied fair value. Results of the goodwill impairment reviews performed

during 2010, 2009 and 2008 are summarized in Note 2 to the Consolidated Financial Statements.

Impairment of Long-Lived Assets

The Company monitors the carrying value of long-lived assets for potential impairment each quarter

based on whether certain trigger events have occurred. These events include current period losses

combined with a history of losses or a projection of continuing losses or a significant decrease in the

market value of an asset. When a trigger event occurs, an impairment calculation is performed, comparing

projected undiscounted future cash flows, utilizing current cash flow information and expected growth

rates related to specific stores, to the carrying value for those stores. If the Company identifies impairment

for long-lived assets to be held and used, the Company compares the assets’ current carrying value to

the assets’ fair value. Fair value is based on current market values or discounted future cash flows. The

Company records impairment when the carrying value exceeds fair market value. With respect to owned

property and equipment held for sale, the value of the property and equipment is adjusted to reflect

recoverable values based on previous efforts to dispose of similar assets and current economic conditions.

Impairment is recognized for the excess of the carrying value over the estimated fair market value, reduced

by estimated direct costs of disposal. The Company recorded asset impairments in the normal course of

business totaling $25, $48 and $26 in 2010, 2009 and 2008, respectively. Included in the 2009 amount

are asset impairments recorded totaling $24 for a southern California reporting unit. Costs to reduce the

carrying value of long-lived assets for each of the years presented have been included in the Consolidated

Statements of Operations as “Operating, general and administrative” expense.

Store Closing Costs

The Company provides for closed store liabilities relating to the present value of the estimated

remaining noncancellable lease payments after the closing date, net of estimated subtenant income. The

Company estimates the net lease liabilities using a discount rate to calculate the present value of the

remaining net rent payments on closed stores. The closed store lease liabilities usually are paid over the

lease terms associated with the closed stores, which generally have remaining terms ranging from one to

20 years. Adjustments to closed store liabilities primarily relate to changes in subtenant income and actual

exit costs differing from original estimates. Adjustments are made for changes in estimates in the period

in which the change becomes known. Store closing liabilities are reviewed quarterly to ensure that any

accrued amount that is not a sufficient estimate of future costs, or that no longer is needed for its originally

intended purpose, is adjusted to income in the proper period.

Owned stores held for disposal are reduced to their estimated net realizable value. Costs to reduce the

carrying values of property, equipment and leasehold improvements are accounted for in accordance with

the Company’s policy on impairment of long-lived assets. Inventory write-downs, if any, in connection with

store closings, are classified in “Merchandise costs.” Costs to transfer inventory and equipment from closed

stores are expensed as incurred.