Honeywell 2011 Annual Report Download - page 12

Download and view the complete annual report

Please find page 12 of the 2011 Honeywell annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

|

|

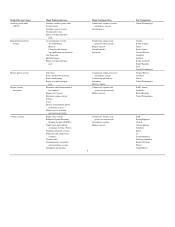

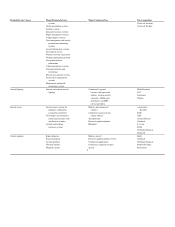

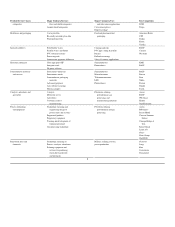

Transportation Systems

Our Transportation Systems segment is one of the leading manufacturers of engine boosting systems for passenger cars and commercial vehicles, as well as a

leading provider of braking products.

Product/Service Classes Major Products/Services Major Customers/Uses Key Competitors

Charge-air systems Turbochargers for gasoline

and diesel engines

Passenger car, truck and

off-highway OEMs

Engine manufacturers

Aftermarket distributors and

dealers

Borg-Warner

Holset

IHI

MHI

Thermal systems Exhaust gas coolers

Charge-air coolers

Aluminum radiators

Aluminum cooling modules

Passenger car, truck and

off-highway OEMs

Engine manufacturers

Aftermarket distributors and

dealers

Behr

Modine

Valeo

Brake hard parts and other

friction materials

Disc brake pads and shoes

Drum brake linings

Brake blocks

Disc and drum brake

components

Brake hydraulic components

Brake fluid

Aircraft brake linings

Railway linings

Automotive and heavy vehicle

OEMs, OES, brake

manufacturers and

aftermarket channels

Installers

Railway and commercial/military

aircraft OEMs and brake

manufacturers

Advics

Akebono

Continental

Federal-Mogul

ITT Corp

JBI

Nisshinbo

TRW

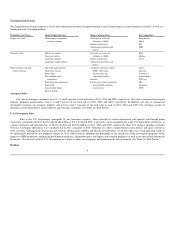

Aerospace Sales

Our sales to aerospace customers were 31, 33, and 36 percent of our total sales in 2011, 2010 and 2009, respectively. Our sales to commercial aerospace

original equipment manufacturers were 6, 6 and 7 percent of our total sales in 2011, 2010 and 2009, respectively. In addition, our sales to commercial

aftermarket customers of aerospace products and services were 11 percent of our total sales in each of 2011, 2010 and 2009. Our Aerospace results of

operations can be impacted by various industry and economic conditions. See "Item 1A. Risk Factors."

U.S. Government Sales

Sales to the U.S. Government (principally by our Aerospace segment), acting through its various departments and agencies and through prime

contractors, amounted to $4,276, $4,354 and $4,288 million in 2011, 2010 and 2009, respectively, which included sales to the U.S. Department of Defense, as

a prime contractor and subcontractor, of $3,374, $3,500 and $3,455 million in 2011, 2010 and 2009, respectively. Base U.S. defense spending (excludes

Overseas Contingent Operations) was essentially flat in 2011 compared to 2010. Although we expect a slight decline in our defense and space revenue in

2012 (see Item 7 Management's Discussion and Analysis of Financial Condition and Results of Operations), we do not expect our overall operating results to

be significantly affected by any proposed changes in 2012 federal defense spending due principally to the varied mix of the government programs which

impact us (OEM production, engineering development programs, aftermarket spares and repairs and overhaul programs) as well as our diversified commercial

businesses. Our contracts with the U.S. Government are subject to audits, investigations, and termination by the government. See "Item 1A. Risk Factors."

Backlog

9