HSBC 2006 Annual Report Download - page 98

Download and view the complete annual report

Please find page 98 of the 2006 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

|

|

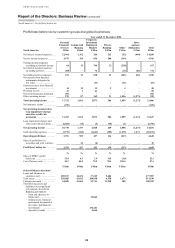

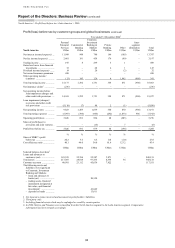

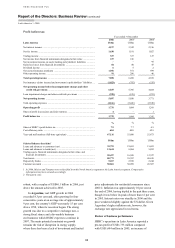

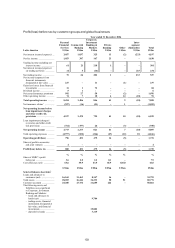

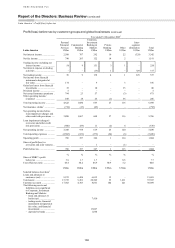

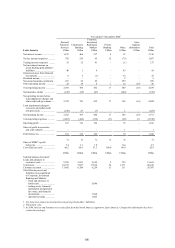

HSBC HOLDINGS PLC

Report of the Directors: Business Review (continued)

Latin America > 2006 / 2005

96

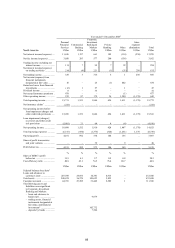

primarily driven by small and middle market

customers. The recruitment of additional relationship

managers and sales staff, investments made in

receivables financing and greater levels of

promotional activity all combined to build HSBC’s

position in this market segment. There was ongoing

success from the ‘giro fácil’ product, offering both

revolving loan and overdraft facilities, with average

balances recording a 13 per cent increase. Spreads

widened as interest rates fell, further augmenting the

income benefits of higher lending volumes.

A 42 per cent rise in net interest income in

Argentina was primarily attributable to strong asset

and liability growth. Average lending and deposit

balances increased by 39 per cent and 19 per cent

respectively, as customer numbers rose, particularly

to the small and micro businesses, helped by

favourable economic conditions and investment in

new sales channels. Asset spreads declined, however,

due to competitive market pressures on pricing, partly

offsetting the income benefits of higher lending

volumes. By contrast, deposit spreads improved.

Net fee income was 36 per cent higher, driven by

robust increases across Mexico, Brazil and Argentina.

In Mexico, fee income rose by 28 per cent with

notable success in increasing cross-sales activity.

Growth in customer numbers contributed to higher

transactional volumes which, combined with an

expanded and improved product offering plus

increased marketing activity and re-pricing

initiatives, led to a 41 per cent rise in income from

payments and cash management services. The

‘Estimulo’ product offering, comprising a packaged

suite of seven different products including a loan

facility, continued to perform well with fee income

nearly trebling compared with 2005. During the third

quarter, a similar product, ‘Estimulo Empresarial’,

was launched, targeting upper-end small business

customers. This product encompasses a suite of

eleven different services and since its introduction

more than 165 clients have been signed, generating

US$50 million of new loans. HSBC’s share of the

trade services market continued to grow, building on

the Group’s international network and product

capabilities. Fees from international factoring and

domestic invoicing payment products also rose, as

new products were successfully piloted and marketed

to existing clients. The signing of new merchant

customers led to higher transaction volumes and a

subsequent 60 per cent rise in card acquiring fees.

In Brazil, fee income rose by 47 per cent as

effective cross-selling led to an increase in the

average number of products held per customer.

Current account fee income grew from higher levels

of transactional activity and tariff increases

implemented in 2005. Pricing changes introduced

part-way through 2006 led to higher revenues from

payment and cash management services. There was

improved fee income from assets under management,

and additional marketing to promote trade products

led to a rise in trade services fees.

Fee income in Argentina was 27 per cent higher,

primarily from increases in account and trade

services along with payments and cash management

fees.

Loan impairment charges and other credit risk

provisions doubled, reflecting strong lending growth,

a higher proportion of small and micro business

lending, and the seasoning of the portfolio.

In Mexico, strong growth in the lower-end small

and micro business lending balances led to increased

loan impairment charges during the year.

A 41 per cent rise in Brazil again reflected large

increases in small and micro business lending

balances and higher delinquency rates as the portfolio

seasoned. This led to a 12 basis point increase in the

proportion of impaired loans to assets. Various

actions were undertaken to manage the effects of the

weakening credit environment, with debt collection

operations enhanced and closer cooperation forged

between sales and collections staff. Changes were

also made to underwriting criteria, coupled with

revisions to sales staff incentive schemes. Following

these measures, an improvement in credit quality was

seen and charges reduced in the second half of the

year compared with the first half. In Argentina,

releases were lower than in 2005.

Operating expenses of US$822 million were

21 per cent higher than in 2005, as businesses

expanded strongly across Latin America.

In Mexico, operating expenses rose by 26 per

cent, largely driven by higher transactional volumes,

new clients acquired and increased lending activity.

Non-staff costs were higher, reflecting the marketing

and IT-related support to business growth.

In Brazil, expenses grew by 19 per cent,

also largely from higher staff, marketing and

administrative costs. Business expansion activities in

the small and middle market customer segments

followed the recruitment of 270 additional employees

and this, together with union-agreed pay increases,

were the principal drivers behind the 21 per cent rise

in staff costs. Continued enlargement of the branch

network, the opening of an International Banking

Centre and new sales offices combined with increases

in marketing and administration costs in support of

business expansion, contributed further to cost