HSBC 2006 Annual Report Download - page 100

Download and view the complete annual report

Please find page 100 of the 2006 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

|

|

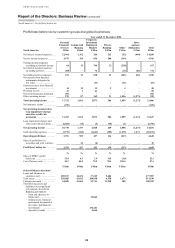

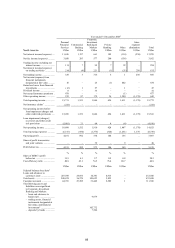

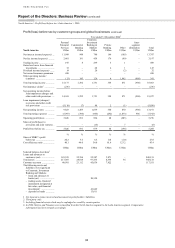

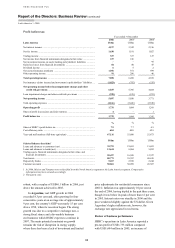

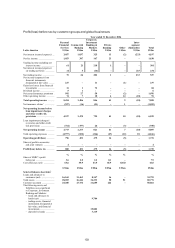

HSBC HOLDINGS PLC

Report of the Directors: Business Review (continued)

Latin America > 2005

98

In Brazil, the cyclical slowdown which began in

late 2004 continued throughout 2005, with full-year

GDP growth of 2.3 per cent compared with 4.9 per

cent in 2004. This modest performance was the result

of tight monetary policy, political uncertainty and the

appreciation of the Brazilian real. External demand

provided support, with exports growing by 23 per

cent in 2005 to record levels, helping to create trade

and current account surpluses of US$45 billion and

US$14 billion respectively, and increasing net

international reserves by 96 per cent to

US$54 billion. The tight monetary policy, with real

interest rates among the highest in the world at

10.5 per cent, slowed inflation from 7.6 per cent in

2004 to 5.7 per cent in 2005, in line to achieve the

Central Bank’s 4.5 per cent inflation target for 2006.

Having established its anti-inflationary credentials,

the Central Bank cut interest rates by 175 basis points

between September and the end of 2005 in order to

stimulate growth and ease the pressure on the real.

In Argentina, the recovery from the crisis of

2001 continued in 2005, helped by a favourable

external environment and the success of the offer to

exchange replacement discount bonds issued in June

for defaulted debt. Average GDP growth was 9.1 per

cent in 2005. Fiscal performance remained strong,

with the public sector posting an overall surplus of

approximately 3.3 per cent of GDP. This surplus

helped to offset the expansionary effect on money

supply growth of the large foreign exchange

interventions of the Central Bank, which continued to

pursue a nominal rate policy of near stability against

the US dollar despite strong upward pressure on the

Argentine peso. This policy was supported by newly

introduced controls on capital inflows. Inflation

remained a concern, however, having accelerated to

12.3 per cent in December 2005. Following the

example of Brazil, at the end of the year the

authorities decided to make an early repayment of

Argentina’s US$9.8 billion debt owed to the IMF.

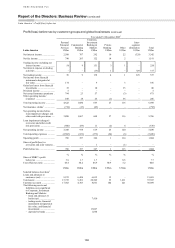

Review of business performance

HSBC’s operations in Latin America reported a pre-

tax profit of US$1,604 million, compared with

US$1,242 million in 2004, representing an increase

of 29 per cent. On an underlying basis, pre-tax profits

grew by 19 per cent and represented around

8 per cent of HSBC’s equivalent total profit. Growth

was achieved, in part, as a result of a US$89 million

gain on the sale of Brazil’s property and casualty

insurance business. In Mexico, robust balance sheet

growth drove higher profit before tax and HSBC in

Argentina benefited from a strong economic recovery

and certain one-off items including the receipt of

compensation bonds.

The commentary that follows is on an underlying

basis.

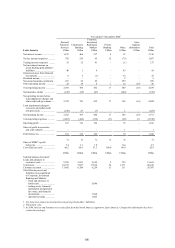

Personal Financial Services reported a pre-tax

profit of US$786 million, an increase of 13 per cent.

In Mexico, excluding the transfer of some customers

to the Commercial Banking segment, pre-tax profits

rose. This was driven by strong revenue growth from

higher deposit balances and widening spreads, strong

loan growth and higher fee income, partly offset by

the non-recurrence in 2005 of loan impairment

provision releases in 2004.

The rise in pre-tax profits in Brazil was partly as

a result of gains on the sale of the property and

casualty insurance business, with the remaining

increase driven by strong loan growth in vehicle

finance and personal lending, together with record

credit card sales. The cost efficiency ratio improved

by 2 percentage points as higher income was partly

offset by increased costs incurred in supporting

business expansion and developing alternative sales

channels. Loan impairment charges increased

reflecting, in Brazil, lending growth and an increase

in delinquency rates in the consumer finance business

and, in Mexico, higher charges from increased

lending and the non-recurrence in 2005 of loan

impairment provision releases in 2004. In 2005, the

Brazilian insurance business was transferred from

‘Other’ to Personal Financial Services. Profit before

tax increased by US$16 million as a result, though

individual account lines showed much larger

variances: where appropriate, the reasons are noted

below.

Net interest income rose by 27 per cent

compared with 2004. Consumer demand for credit

remained strong, fuelled by lower unemployment

across the region and declining inflation in Brazil and

Mexico. This contributed to significant growth in

personal lending, mortgages, vehicle finance loans

and credit cards.

In Mexico, net interest income rose, primarily

from strong deposit and loan growth and the

widening of deposit spreads. In 2005, HSBC in

Mexico widened its competitive funding advantage,

maintaining the lowest funding cost in the market.

There was strong growth in consumer lending,

although asset spreads declined, reflecting a

reduction in yields in an increasingly competitive

market. Funding costs rose, due to higher average

interest rates.

HSBC in Mexico continued to lead the market in

customer deposit growth, with a 1.5 per cent increase

in market share to 15.9 per cent despite a highly

competitive market place. This was largely due to the

success of ‘Tu Cuenta’, the only integrated financial