HSBC 2006 Annual Report Download - page 126

Download and view the complete annual report

Please find page 126 of the 2006 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

|

|

HSBC HOLDINGS PLC

Report of the Directors: Financial Review (continued)

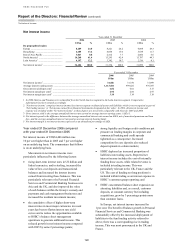

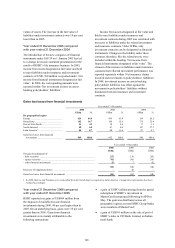

Net interest income / Net fee income

124

growth was 10 per cent. HSBC’s net interest margin

was 3.10 per cent in 2006, compared with 3.14 per

cent in 2005.

Year ended 31 December 2005 compared

with year ended 31 December 2004

Net interest income of US$31,334 million was

US$235 million, or 1 per cent, higher than in 2004.

Under IFRSs, HSBC’s presentation of net

interest income in 2005 was particularly affected by:

• the reclassification of certain preference

dividends within non-equity minority interests

as interest expense;

• the inclusion of certain loan origination fees and

expenses as part of an effective interest rate

calculation instead of being recognised in full on

inception of the loan; and

• external interest income and expense on trading

assets and liabilities now included within ‘Net

trading income’.

Adjusting for these changes and on an

underlying basis, net interest income increased by

12 per cent. The commentary that follows is on this

basis.

The benefit of strong growth in interest-earning

assets globally more than offset the effect of spread

compression from flattening yield curves in the

major currencies. This latter phenomenon reduced

opportunities for HSBC’s balance sheet management

operations to enhance margin by placing the Group’s

surplus liquidity longer term than the

behaviouralised deposit funding base. In addition,

short-term interest rate rises in the US reduced

spreads on consumer finance loans.

In Europe, higher personal and commercial

lending and increased deposit balances led to a

12 per cent increase in net interest income. UK

Personal Financial Services balances grew strongly

in mortgages, unsecured lending and cards, mainly

funded by a 12 per cent increase in deposit and

savings balances. In Turkey, card balances grew

from increased marketing and working with HSBC’s

retail partners. Spreads tightened on UK personal

lending, reflecting the introduction of preferential

pricing for lower-risk and higher-value customers,

and on savings, due to better pricing for customers.

In Commercial Banking in the UK, lending and

overdraft balances increased by 23 per cent, with

growth particularly strong in the property,

distribution and services sectors. Deposit balances

grew by 11 per cent, partly from keen pricing,

though this reduced deposit spreads. Yields on UK

corporate lending, which were lower largely as a

result of competitive pressure, were only partly

offset by higher loan balances, while lower balance

sheet management income reflected the effect of

rising short-term rates and flattening yield curves on

balance sheet management revenues.

In North America, net interest income increased

by 4 per cent. Growth in mortgage, card and

unsecured personal lending balances was strong,

offsetting spread contraction as the cost of funds rose

with progressive interest rate rises. Core deposit

growth benefited from expansion of the branch

network and the launch of new savings products,

including an online savings product which attracted

a significant number of new customers. Treasury

income from balance sheet management within

Corporate, Investment Banking and Markets

diminished as the rise in short-term interest rates

limited opportunities to profit from placing the

liquidity generated from core banking operations

over extended periods.

In Hong Kong, net interest income rose by

17 per cent. Rising interest rates reinvigorated

demand for traditional savings products, driving

increases in personal and commercial savings

balances. Coupled with the rise in deposit spreads,

which increased in line with interest rates, this led to

a sharp rise in net interest income. Mortgage spreads

contracted, however, as the gradual increase in

yields during the year, in line with higher rates, was

more than offset by rising funding costs. There was

little net new lending for residential mortgages as

interest rate rises cooled the residential property

market in the second half of 2005. Economic growth

in mainland China boosted commercial lending to

the trade and manufacturing sectors, and property

lending also increased. Treasury income remained

under pressure, with rising short-term interest rates

and a flat yield curve providing limited opportunities

to profitably deploy surplus liquidity and increasing

funding costs.

In the Rest of Asia-Pacific, net interest income

increased by 24 per cent, reflecting business

expansion and favourable economic conditions

throughout the region. In the Middle East, buoyant

oil-based economies stimulated demand for credit

for property and infrastructure projects. Increasing

personal and corporate wealth contributed to growth

in deposit balances, while interest rate rises led to

higher deposit spreads. General economic expansion

created demand for consumption credit which

boosted credit card lending. For the reasons noted

above, treasury income from balance sheet

management was weaker.