HSBC 2006 Annual Report Download - page 146

Download and view the complete annual report

Please find page 146 of the 2006 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

|

|

HSBC HOLDINGS PLC

Report of the Directors: Financial Review (continued)

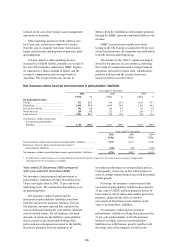

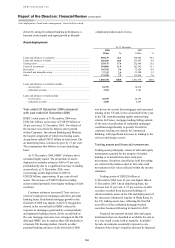

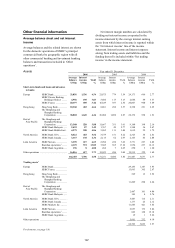

Asset deployment / Funds under management / Assets held in custody

144

driven by strong investment banking performance, a

buoyant stock market and rapid growth in Shariah-

compliant products and services.

Asset deployment

At 31 December

2006 2005

US$m % US$m %

Loans and advances to customers .......................................................... 868,133 46.6 740,002 49.3

Loans and advances to banks ................................................................. 185,205 10.0 125,965 8.4

Trading assets ......................................................................................... 328,147 17.6 232,909 15.5

Financial investments ............................................................................. 204,806 11.0 182,342 12.1

Derivatives .............................................................................................. 103,702 5.6 73,928 4.9

Goodwill and intangible assets ............................................................... 37,335 2.0 33,200 2.2

Other ....................................................................................................... 133,430 7.2 113,624 7.6

1,860,758 100.0 1,501,970 100.0

Loans and advances to customers include:

– reverse repos ................................................................................... 18,755 14,610

– settlement accounts ........................................................................ 3,254 2,142

Loans and advances to banks include:

– reverse repos ................................................................................... 45,019 24,754

– settlement accounts ........................................................................ 2,028 2,669

Year ended 31 December 2006 compared

with year ended 31 December 2005

HSBC’s total assets at 31 December 2006 were

US$1,861 billion, an increase of US$359 billion or

24 per cent since 31 December 2005. Two thirds of

the increase was driven by balance sheet growth

within Corporate, Investment Banking and Markets,

the largest component of which was trading assets.

Acquisitions added US$13 billion to total assets. On

an underlying basis, total assets grew by 17 per cent.

The commentary that follows is on an underlying

basis.

At 31 December 2006, HSBC’s balance sheet

remained highly liquid. The proportion of assets

deployed in customer advances fell to 47 per cent,

predominantly due to a significant increase in trading

assets which, at 31 December 2006, were

2 percentage points higher than in 2005 at

US$328 billion, representing 18 per cent of total

assets. The increase of US$95 billion in trading

assets resulted primarily from higher holdings of debt

securities.

Customer advances increased 17 per cent as a

result of expansion in mortgages and other personal

banking loans. Residential mortgage growth in the

first half of 2006 was mainly in the US, though this

slowed in the second half as HSBC reduced its

exposure to mortgages generated by correspondents

and tightened lending criteria. In the second half of

the year mortgage increases were strongest in the UK

although HSBC saw its market share fall modestly in

a buoyant UK housing market. Growth in other

personal banking advances in the first half of 2006

was driven by second lien mortgages and unsecured

lending in the US and, in the second half of the year,

in the UK, notwithstanding tighter underwriting

criteria. In France, mortgage lending falling outside

of the strict classification of residential mortgages

contributed significantly to growth. Growth in

corporate lending was mainly in Commercial

Banking, with significant increases in lending to the

services and energy sectors.

Trading assets and financial investments

Trading assets principally consist of debt and equity

instruments acquired for the purpose of market

making or to benefit from short-term price

movements. Securities classified as held for trading

are carried in the balance sheet at fair value with

movements in fair value reflected within the income

statement.

Trading assets of US$328 billion at

31 December 2006 were 41 per cent higher than at

31 December 2005. On an underlying basis, the

increase was 32 per cent. A 27 per cent rise in debt

securities resulted from increased holdings of

shorter-maturity assets in the UK and deployment of

the increased commercial surplus in Hong Kong. In

the US, trading assets rose, reflecting the first full

year effect of the residential mortgage-backed

securities business following its launch in 2005.

Financial investments include debt and equity

instruments that are classified as available for sale or,

to a very small extent, held to maturity. Available-

for-sale investments essentially represent a core

element of the Group’s liquidity and may be disposed