HSBC 2006 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 2006 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

|

|

29

whether there is a case for changing the existing

rules for the sale of PPI.

The OFT conducted the follow-up review of the

SME market, prescribed by its report published in

2002. HSBC cooperated with this review and awaits

the findings.

Following MasterCard’s appeal to the

Competition Commission Appeals Tribunal, the OFT

withdrew its original interchange fee case to

concentrate on a new case against both MasterCard

and Visa. The European Commission is also

investigating interchange fees, and HSBC has

responded to its requests for information.

In November the winding down of the Payment

Systems Taskforce was announced, and a new

governance body for payment systems, the Payments

Industry Association, was established. HSBC is

positioned to deliver the faster electronic payments

introduced by the Payment Systems Taskforce and

meets its minimum standards for cheque clearing.

France

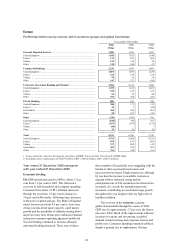

Stable interest rates in the eurozone contributed to a

strong growth in real estate investment in France.

Competition between French banks concentrated on

the promotion of real estate mortgage loans, which

are the principal means by which new customers in

France are acquired. Market activity increased and

consumers continued to enjoy improved pricing to

the detriment of bank margins.

The payment of interest on sight deposits,

authorised from the beginning of 2005, was

introduced by one major mutual French bank, albeit

linked to a quarterly fee for banking services. Market

reaction was muted and, to date, no other leading

French bank has followed suit.

From January 2006 the Banque Postale was able

to offer real estate lending and financial services,

including the sale of investment products

manufactured by third party providers. Given the

scale of Banque Postale’s geographical coverage,

this will increase competition in an already

competitive market.

The French government reformed the household

tax law for 2006/2007, notably introducing a tax

exemption on capital gains on equities sold after an

eight-year holding period and a cap on total

household taxes (including income, wealth and local

taxes) at 60 per cent of income. The higher marginal

tax rate has been limited to 40 per cent. These

reforms will increase disposable income for the

wealthier individuals who form one of HSBC

France’s key customer segments.

At the end of December 2005, French banks

were granted approval, as in the UK, to provide

equity release mortgages. This will assist customers

to invest in real estate and finance consumption.

Hong Kong

There was some improvement in the lending market

in 2006, as the stable interest rate environment,

liquid market, and moderate cost of borrowing

supported growth in consumer spending, and

demand for personal loans and credit cards rose in

consequence.

Competition remained fierce in traditional

mortgage products due to the still subdued property

market. Robust equity markets buoyed sales of

investment products and also benefited investment-

related loans.

The sustained appreciation of the Chinese

currency during 2006 had no marked effect on Hong

Kong’s renminbi deposit business. Instead, funds

were attracted to Chinese stocks listed in Hong

Kong, notably in relation to some of the substantial

Chinese IPOs. Nevertheless, local currency deposits

continued to grow rapidly due to rising household

incomes.

Rest of Asia-Pacific

(including the Middle East)

The competitive environment in the Rest of

Asia-Pacific continued to intensify as international

banks focused on targeted sectors in emerging

markets in pursuit of higher returns. Local banks

also actively expanded their reach and business, both

within countries and across borders. Competition

remained intense throughout the region in all of the

customer groups served by HSBC. Regulations in

certain countries act to limit the ability of foreign-

owned banks to grow both by acquisition and

organically by adding distribution or participating in

shared networks with domestic banks. However, in

many countries the growing sophistication of the

relatively young population and increasing affluence

of the middle class continued to provide HSBC with

further opportunities for growth.

Banks and non-banks, both local and

international, are rapidly building consumer finance

and direct banking businesses in a number of

countries in the region.

North America

In an already highly competitive US financial

services industry, institutions involved in a broad

range of financial products and services continued to