HSBC 2006 Annual Report Download - page 423

Download and view the complete annual report

Please find page 423 of the 2006 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

413 -

414

414 -

415

415 -

416

416 -

417

417 -

418

418 -

419

419 -

420

420 -

421

421 -

422

422 -

423

423 -

424

424 -

425

425 -

426

426 -

427

427 -

428

428 -

429

429 -

430

430 -

431

431 -

432

432 -

433

433 -

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

|

|

421

Approximately US$17 billion (2005: US$18 billion) of the consideration received has been sold or repledged in

connection with stock borrowing transactions.

(a) Pension and post-retirement costs

On 31 December 2006, HSBC adopted the recognition and disclosure provisions of SFAS 158 ‘Employers’

Accounting for Defined Benefit Pension and Other Post-retirement Plans – an amendment of FASB Statements

No. 87, 88, 106 and 132(R)’ (SFAS 158), SFAS 158 requires HSBC to recognise the funded status of its pension

plans in a manner similar to IAS 19.

The provisions of SFAS 87 ‘Employers’ accounting for pensions’ and SFAS 158 have been applied to HSBC’s

main defined benefit pension plans, which make up approximately 96 per cent of all HSBC’s schemes by plan

assets. For non-US schemes, HSBC has applied SFAS 87 with effect from 30 June 1992 as it was not feasible to

apply as at 1 January 1989, the date specified in the standard.

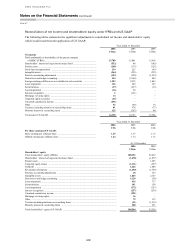

The transition adjustments for adoption of SFAS 158 for pensions and post-retirement costs were as follows:

Before

application of

Statement 158 Adjustments

After

application of

Statement 158

US$m US$m US$m

Other assets (including prepayments and accrued income) ................... 47,589 56 47,533

Total assets .............................................................................................. 1,712,683 56 1,712,627

Retirement benefit liabilities ................................................................... 7,555 2,000 5,555

Provisions ................................................................................................ 15,951 (650) 16,601

Total liabilities ........................................................................................ 1,596,836 (1,350) 1,598,186

Total shareholders’ equity ...................................................................... 109,946 1,406 108,540

Components of net periodic benefit cost related to HSBC’s defined benefit pension plans and post-retirement

benefits other than pensions under US GAAP were as follows:

2006 2005 2004

US$m US$m US$m

Components of net periodic benefit cost

Service cost ............................................................................................. 779 684 590

Interest cost ............................................................................................. 1,485 1,377 1,305

Expected return on plan assets ................................................................ (1,601) (1,365) (1,317)

Amortisation of transition obligation ..................................................... – 8 12

Amortisation of prior service cost .......................................................... 7 (6) 5

Amortisation of recognised net actuarial loss ........................................ 211 165 142

Curtailment .............................................................................................. (8) (4) 225

Net periodic pension cost under US GAAP ........................................... 873 859 962

Net periodic pension cost under IFRSs .................................................. 664 684 837

In 2007, components of net periodic benefit cost will include US$7 million for the amortisation of prior service

cost and US$164 million for amortisation of recognised net actuarial loss.

Under the provisions of SFAS 87, when a pension plan’s accumulated benefit obligation (the value of the

benefits accrued based on employee service up to the balance sheet date) exceeds the fair value of its assets, an

additional minimum pension liability equal to this excess is recognised by the employer to the extent that the

excess is greater than any accrual which has already been established for unfunded pension costs.

Simultaneously, an intangible asset is established equal to the lower of the liability recognised for the unfunded

benefit obligation and the amount of any unrecognised prior service cost.

At 31 December 2006, HSBC recognised an additional minimum pension liability of US$3,130 million prior to

adoption of FAS158 (2005: US$3,206 million) in respect of its unfunded accumulated benefit obligation.