HSBC 2006 Annual Report Download - page 128

Download and view the complete annual report

Please find page 128 of the 2006 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

|

|

HSBC HOLDINGS PLC

Report of the Directors: Financial Review (continued)

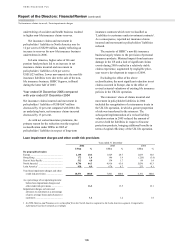

Net fee income

126

products. HSBC responded by launching new

investment products and increasing promotional

activity, which contributed to higher unit trust,

broking and custody fees.

• There was an increase in cards in issue, which

drove higher transaction volumes and balances

and led to a 16 per cent rise in card fee income,

principally in the US;

• Strong equity market performance also

benefited HSBC’s asset management activities.

Funds under management grew by 16 per cent

and performance fees rose strongly, most

notably in HSBC’s BRIC (Brazil, Russia, India

and China) funds and in the Hermitage Fund, a

leading fund investing in Russia.

• The successful promotion of packaged account

products which, together with increased

customer numbers and higher transaction

volumes, led to a 13 per cent rise in account

services fees. Higher cross-border currency

flows led to increased remittance income.

• Reduced sales of creditor insurance products in

the UK were largely offset by higher fees in

HSBC’s Latin American insurance businesses,

particularly in Argentina and Brazil.

• Increased taxpayer services fees, higher income

from investment and other services provided by

HSBC’s insurance businesses, and increased

corporate and WTAS advisory fees in the US

contributed to the increase in other fee income.

In Europe, account service fees increased as a

result of customer acquisition, higher sales of

packaged products and increased transaction

volumes. Rising stock markets led to higher sales of

investment products and growth in funds under

management, while product mix improvements and

service enhancements also contributed to a rise in

investment fees. Higher performance fees in respect

of the Hermitage Fund contributed an additional

US$23 million in fee income, net of performance

fees paid to the fund’s investment advisor. Offsetting

these increases, HSBC’s decision to constrain

unsecured lending growth in the UK resulted in

lower creditor protection insurance fees.

In Hong Kong, a buoyant IPO market together

with product launches and enhancements contributed

to higher sales of investment products; this was

augmented by increased transaction volumes

following strong growth in local and regional equity

markets. As global customers continued to seek

investment opportunities in emerging markets, funds

under management increased. Growth in cards in

issue led to higher card fees.

In the Rest of Asia-Pacific, higher trade and

remittance flows led to increased payments and cash

management income. Investment flows into

emerging market funds triggered growth in custody

and funds administration fees, while rising equity

markets and product launches contributed to

increased investor demand and higher income from

custody, brokerage and the sale of investments.

In North America, card fees increased as a result

of higher balances and improved interchange rates,

while private label card fees benefited from

renegotiations with a number of merchants.

Increases in 2006 were partly offset by the effect of

FFIEC guidance, which limits certain fee billings for

non-prime credit card accounts. Following its launch

in 2005, activity within HSBC’s mortgage-backed

securities business increased rapidly during 2006. As

a result, a greater proportion of loans originated by

HSBC were sold to the secondary market and

mortgage servicing fees grew accordingly, while

income in the mortgage-backed securities business

also rose. Tariff increases contributed to higher

account service fees. Higher business volumes led to

a rise in taxpayer services fees, while the WTAS

business progressed strongly, expanding its customer

base and reporting significantly higher fee income.

In Latin America, increased cards in circulation

and improvements in activation times led to higher

card issuing fees, while growth in the merchant

customer base led to a rise in card acquiring income.

Account servicing fees benefited from higher

packaged account sales, enhancements to other

current account products, price increases and greater

transaction volumes. The expansion of HSBC’s

ATM network in Mexico drove higher ATM fees.

Year ended 31 December 2005 compared

with year ended 31 December 2004

Net fee income of US$14,456 million was

US$1,508 million or 12 per cent higher than in 2004.

Under IFRSs, a greater proportion of fees relating to

the provision of credit facilities is now amortised and

accounted for in net interest income as part of an

effective interest rate calculation than was the case

before 1 January 2005. This resulted in a reduction

in reported net fee income of approximately 4 per

cent. Excluding this effect and on an underlying

basis, growth in net fee income was 14 per cent and

the comments that follow are presented on this basis.

The principal drivers of this growth were:

• the increase in card fee income, reflecting strong

growth in personal credit card sales across the

Group and increased transaction volumes;