HSBC 2006 Annual Report Download - page 231

Download and view the complete annual report

Please find page 231 of the 2006 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

|

|

229

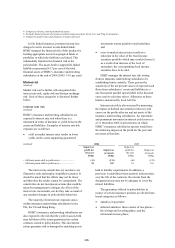

Following the disposal of the non-life insurance

portfolio in Brazil in 2005, credit non-life business

now represents the largest single class and is

concentrated in the US and the UK. This business is

originated in conjunction with the provision of loans.

Insurance risk

(Audited)

The principal insurance risk faced by HSBC is that

the cost of claims combined with acquisition and

administration costs may exceed the aggregate

amount of premiums received and investment

income. HSBC manages its insurance risks through

the application of formal underwriting, reinsurance

and claims procedures designed to ensure

compliance with regulations.

The Group manages insurance risk by

diversifying insurance business by type and

geography and by focusing on risks that are

straightforward to manage which, in the main, are

related to core underlying banking activities (for

example, credit life products). The following tables

provide an analysis of the insurance risk exposures

by geography and by type of business. These tables

demonstrate the Group’s diversification of risk.

Personal lines tend to be higher volume and with

lower individual value than commercial lines, which

further diversifies the risk. Compared to non-life

business, life business tends to be longer term in

nature and frequently involves an element of savings

and investment in the contract. Separate tables are

therefore provided for life and non-life business,

reflecting their very distinct risk characteristics. The

life insurance risk table provides an analysis of

insurance liabilities as the best available overall

measure of the insurance exposure. The table for

non-life business uses written premiums as

representing the best available measure of risk

exposure.

Both life and non-life business insurance risks

are controlled through high level procedures set

centrally, and can be supplemented with procedures

set locally which take account of specific local

market conditions and regulatory requirements. For

example, central authorisation is required to write

certain classes of business, with restrictions applying

particularly to commercial and liability non-life

insurance. For life business in particular, local

ALCOs monitor the risk exposures.

As indicated in the specific comments relating

to particular classes, use is also made of reinsurance

as a means of further mitigating exposure, in

particular to aggregations of catastrophe risk.

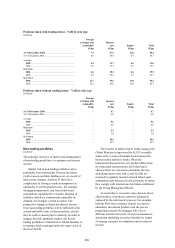

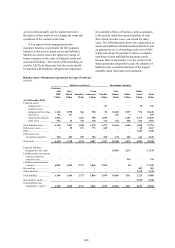

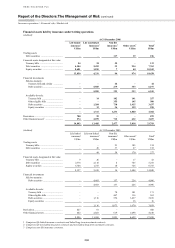

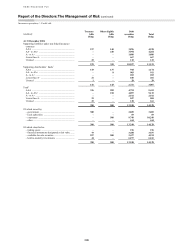

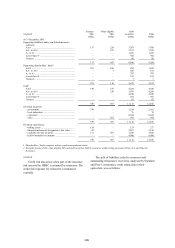

Analysis of life insurance risk – policyholder liabilities

(Audited)

Europe

Hong

Kong

Rest of

Asia-

Pacific

North

America

Latin

America

Total

US$m US$m US$m US$m US$m US$m

At 31 December 2006

Life (non-linked)

Insurance contracts with DPF1 ....................... 195 6,001 193 – – 6,389

Credit life ........................................................ 130 – – 200 – 330

Annuities ........................................................ 271 – 26 1,106 1,370 2,773

Term assurance and other long-term

contracts ..................................................... 1,134 75 89 – 236 1,534

Total life (non-linked) ........................................ 1,730 6,076 308 1,306 1,606 11,026

Life (linked) ........................................................ 1,270 765 402 – 1,248 3,685

Investment contracts with DPF1 ......................... – – 20 – – 20

Life insurance policyholders’ liabilities ............. 3,000 6,841 730 1,306 2,854 14,731

At 31 December 2005 (restated2)

Life (non-linked)

Insurance contracts with DPF1 ........................... 155 3,886 152 – – 4,193

Credit life ........................................................ 156 – – 196 – 352

Annuities ........................................................ 202 – 22 1,075 1,091 2,390

Term assurance and other long-term

contracts ..................................................... 1,063 68 82 – 221 1,434

Total life (non-linked) ........................................ 1,576 3,954 256 1,271 1,312 8,369

Life (linked) ........................................................ 1,201 536 332 – 826 2,895

Investment contracts with DPF1 ......................... – – 9 – – 9

Life insurance policyholders’ liabilities ............. 2,777 4,490 597 1,271 2,138 11,273