HSBC 2006 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2006 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

|

|

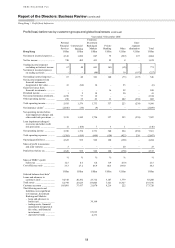

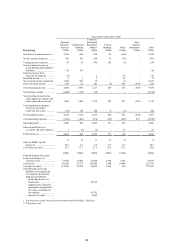

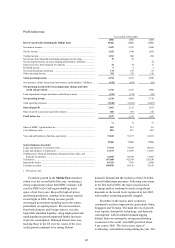

HSBC HOLDINGS PLC

Report of the Directors: Business Review (continued)

Hong Kong > 2005

54

Net fees fell by 6 per cent to US$740 million,

driven mainly by lower sales of unit trusts and

capital guaranteed funds, partly offset by higher

sales of structured deposit products and open-ended

funds. A 34 per cent fall in unit trust fee income was

driven by a change in market sentiment during 2005.

The combined effect of higher interest rates and a

flattening yield curve reduced customer demand for

capital guaranteed funds and longer-term equity-

related investment products. Investors preferred

shorter-term investment products which in turn

generated lower fees. Revenues from open-ended

fund sales reflected this, increasing by 32 per cent to

US$95 million with the introduction of 173 new

funds increasing the choice available to investors.

This was an important strategic initiative to position

HSBC as the leading investment service provider in

Hong Kong, where customers can now choose from

over 300 funds.

Revenues from structured deposit products

grew, with strong sales volumes aided by new

products launched. The success of the Exclusive

Placement Service, launched in 2004 for HSBC

Premier customers, continued with year-on-year

revenue growth of 178 per cent. The service offers

an extensive product range of yield enhancement

options, re-priced daily and linked to foreign

exchange or interest rates. IPO certificate of deposit

offerings doubled. These were partly offset by lower

revenues from ‘Deposit plus’ and ‘Equity linked

note’ products.

Fee income from credit cards grew by 9 per

cent, reflecting a 21 per cent increase in spending

along with a 15 per cent rise in the number of cards

in circulation to four million. In stockbroking and

custody services, new services were launched aimed

at facilitating securities management by customers.

Competitive pricing and a high quality of service on

the internet led to a 15 per cent growth in customers

holding securities with HSBC.

HSBC continued to place significant emphasis

on the growth and development of its insurance

business, and increased the range of products

offered. Insurance revenues grew by 20 per cent,

aided by new products launched which included the

‘Five year excel’ and the ‘Three year express wealth’

joint life insurance and wealth products. HSBC was

Hong Kong’s leading online insurance provider,

offering 12 insurance products. This, coupled with

competitive pricing, led to a 91 per cent growth in

online insurance revenues. Medical insurance

products were enhanced and heavily marketed in

response to the growing public demand for private

medical protection to complement new medical

reforms being introduced.

Improvements in credit conditions, which

benefited from economic growth, higher property

prices and lower bankruptcies, underpinned a net

release of loan impairment charges and other credit

risk provisions of US$11 million in 2005, compared

with a net charge of US$56 million in 2004. This

was mainly driven by continued improvement in

credit quality within the credit card portfolio, and a

collective provision release of US$23 million in

respect of prior year impairment allowances on the

restructured lending portfolio. The strong housing

market enabled individually assessed allowance

releases of US$24 million in the mortgage portfolio.

There was also a release of US$11 million in respect

of collective loan impairment allowances, benefiting

from the improved economic conditions highlighted

above.

Operating expenses fell by 4 per cent to

US$1,305 million. This was largely due to a change

in the method by which centrally incurred costs are

allocated to the customer groups. IT development

costs rose in support of future growth initiatives, and

higher marketing and advertising expenditure was

incurred to underpin organic growth. Staff costs

were marginally lower in 2005. Branch teams were

restructured to dedicate more staff to sales and

customer service, and significant improvements were

made to the reward structure to ensure retention of

high calibre individuals. Overall, headcount in the

branch network fell by 4 per cent, reflecting

operating efficiency improvements and higher

utilisation of the Group Service Centres.

Pre-tax profits in Commercial Banking

increased by 6 per cent to US$955 million. Increased

deposit spreads and a rise in lending and deposit

balances led to higher net interest income, though

this was partly offset by larger loan impairment

charges and the non-recurrence of loan allowance

releases.

Net interest income increased by 60 per cent as

a result of increased deposit spreads and asset and

liability growth. The appointment of a number of

experienced relationship managers to service key

accounts, together with the establishment of core

business banking centres, contributed to growth in

deposits and lending. Interest rate rises led to a

67 basis point increase in deposit spreads and,

together with active management of the deposit base,

contributed to increased customer demand for

savings products which resulted in a 6 per cent

increase in deposit balances to US$28.7 billion. The

introduction of a pre-approved lending programme

for SMEs, together with strong demand for credit in

the property, manufacturing, trading and retail

sectors, contributed to a 29 per cent increase in