HSBC 2006 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2006 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

|

|

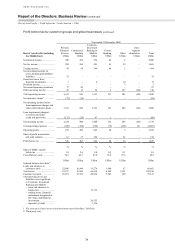

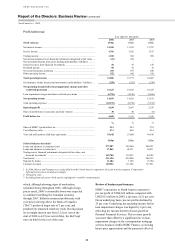

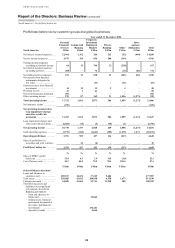

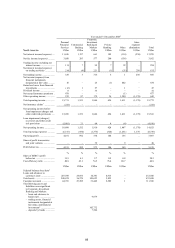

79

portfolio, improved interchange rates and lower fee

charge-offs. Revenues from credit card partnership

enhancement services rose due to greater sales

volumes, expansion into new customer segments and

balance growth.

Within the US retail services business, net fee

income rose, reflecting lower merchant payments, in

part due to changes in contract obligations with

certain merchants. A rise in late fees from growth in

customer account balances and higher fees on

overdue payments contributed further to the

increase.

In the US mortgage-banking business, net fee

income declined. Although mortgage loan service

volumes grew in 2006, contributing additional fee

income from the greater proportion of mortgages

originated and then sold with mortgage servicing

rights retained, these benefits were more than offset

by higher amortisation charges and lower releases of

temporary impairment provisions on mortgage

servicing rights. The taxpayer financial services

business generated higher fee income from increased

loan volumes during the 2006 tax season.

In Canada, net fee income rose by 5 per cent to

US$217 million. Continued growth in the wealth

management business resulted in higher investment

administration fees, and credit card fee income rose,

driven by increased lending.

Trading income fell by 17 per cent, due to lower

income on HSBC Finance’s Decision One mortgage

balances held for resale to secondary market

purchasers. This primarily reflected additional losses

incurred following the repurchase of certain

mortgages previously sold to external third parties

which had subsequently gone into default. Higher

losses on derivatives that did not meet the criteria for

hedge accounting contributed further to the decrease.

A US$20 million gain from the MasterCard

Incorporated IPO was the key reason for the increase

in gains from financial instruments.

Other operating income also rose, primarily

driven by gains on various asset disposals. Most

notably, a US$123 million profit was achieved on

disposal of HSBC’s investment in Kanbay

International Inc, a worldwide information

technology services firm. Income from overnight

and short-term money market investments also rose.

These benefits were partly offset by greater losses

incurred on sales of repossessed properties,

following a 42 per cent rise in such properties as

customers defaulted on their mortgage payments.

Loan impairment charges and other credit risk

provisions of US$6,683 million were 28 per cent

higher than in 2005. In the US, loan impairment

charges rose by 28 per cent despite the non-

recurrence of significant charges which arose in

2005 following hurricane Katrina and increased

levels of bankruptcy filings in the final quarter of the

year. Loan impairment charges were also higher in

the second half of 2006 compared with both the

preceding half and the second half of 2005. The

increase was primarily driven by significantly higher

delinquencies and losses in the mortgage services

correspondent business, concentrated in second lien

and portions of first lien mortgages originated and

purchased in 2005 and 2006. As noted previously,

HSBC witnessed a deterioration in the performance

of these 2005 originations during the first half of

2006. This deterioration continued into the third

quarter and started to affect equivalent loans

originated in 2006. In the final quarter of 2006,

deterioration of these loans, largely the first lien

adjustable rate and second lien loans, worsened

considerably. The heightened risk of loss was

attributable to lower equity in homes as price growth

moderated or reversed, together with a higher

prospective interest burden from ARM resets. As

many of these mortgages were being re-priced in an

environment of higher interest rates, slower asset

price appreciation and tightening credit, HSBC

considers it highly likely that these factors will lead

to increased instances of default in the future on both

first and any associated second lien loans.

Accordingly, a significant increase in loan

impairment charges was recorded in the final

quarter of the year.

Higher lending, the seasoning1 of the loan

portfolio, and a return to more normal historical

levels of delinquency from the exceptionally

favourable credit conditions experienced in recent

periods, all contributed to the overall increase in

impairment charges in the US. This was partly offset

by lower numbers and levels of bankruptcy filings

and the positive effect of low unemployment. The

credit card business, in addition, benefited from

improved recovery rates from loans previously

written off. Notwithstanding the accelerated credit

weakness witnessed in the mortgage services

correspondent business, credit performance as

measured by delinquency and loss in the majority of

the other lending portfolios, including mortgage

balances originated through the branch-based

consumer lending business gradually deteriorated

from the seasoning of a growing portfolio and the

rising proportion of credit card balances. Loan

impairment charges in these portfolios were

1 ‘Seasoning’ describes the emergence of credit

loss

p

atterns in

p

ort

f

olios over time.