HSBC 2006 Annual Report Download - page 139

Download and view the complete annual report

Please find page 139 of the 2006 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

|

|

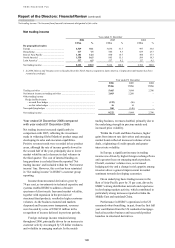

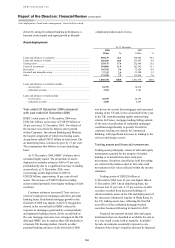

137

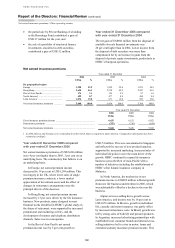

Year ended 31 December

2006

US$m

2005

US$m

2004

US$m

Loan impairment charges1

New allowances net of allowance releases ................................................. 11,326 8,354 7,606

Recoveries of amounts previously written off ............................................ (779) (494) (913)

10,547 7,860 6,693

Individually assessed allowances .................................................................... 458 518 –

Collectively assessed allowances .................................................................... 10,089 7,342 –

General provisions ........................................................................................... – – (498)

Other credit risk provisions ............................................................................. 26 (59) (4)

Total loan impairment charges and other credit risk provisions ..................... 10,573 7,801 6,191

Customer impaired loans ................................................................................. 13,785 11,446 12,427

Customer loan impairment allowances ........................................................... 13,578 11,357 12,542

1 Loan impairment charges in 2004 refer to specific provisions.

Year ended 31 December 2006 compared

with year ended 31 December 2005

The charge for loan impairments and other credit

risk provisions was US$10,573 million, a 36 per cent

increase over that reported in 2005. The analysis that

follows is on an underlying basis.

On an underlying basis, charges increased by

30 per cent. This reflected:

• increased loss experience in the US mortgage

services business, particularly in second lien,

portions of first lien and adjustable rate

mortgages acquired from correspondent brokers

and banks in 2005 and in the first half of 2006;

• 10 per cent underlying lending growth

(excluding lending to the financial sector and

settlement accounts), notably in the UK, the US,

Mexico, Brazil and Asia;

• the continuing effect in the UK of consumer

recourse to formal debt mitigation

arrangements;

• credit deterioration, principally in the first half

of 2006, in unsecured personal and credit card

lending in Taiwan and Indonesia; offset by

• the non-recurrence of a surge in bankruptcy

filings in the US in the fourth quarter of 2005

and the effect of hurricane Katrina; and

• a continued benign commercial and corporate

credit environment.

In Europe, net loan impairment charges rose by

10 per cent to US$2,155 million. In the UK, net

charges rose by a modest 4 per cent as growth in the

personal customer impairment charge, which was

broadly in line with lending growth, was partially

offset by favourable movements on the impairment

charge for commercial loans in a robust corporate

credit environment. The personal sector continued to

experience higher levels of IVA and bankruptcy

filings, following an easing of bankruptcy

regulations in 2004, growth in consumer

indebtedness and a rise in unemployment. This was

mitigated by action taken on underwriting and

collections. In France, the non-recurrence of several

significant recoveries in 2005 resulted in an increase

in net loan impairment charges in 2006.

Loan impairment charges in Hong Kong

remained low at US$172 million, underpinned by

robust personal and commercial credit quality in a

strong economy with low unemployment.

In the Rest of Asia-Pacific, loan impairment

charges rose sharply to US$512 million. Taiwan and

Indonesia experienced credit deterioration during

2006, although the problem peaked in the first half

of the year. Taiwan was affected by the imposition

of a mandatory government debt renegotiation

scheme which allowed customers to extend and

heavily discount repayment terms, leading to

market-wide credit losses. Indonesia was also

affected by regulations, specifically with respect to

minimum re-payment terms which compounded

higher impairments brought about by a reduction in

fuel subsidies. Elsewhere in the Rest of Asia-Pacific

credit quality was stable.

In North America, the net loan impairment

charge increased significantly, by 32 per cent to

US$6,796 million, largely in the second half of

2006, driven by the credit deterioration in US sub-

prime mortgages described in the first bullet point

above. The effects of the decline in US house price

inflation and rising interest rates during 2006 were

accentuated by the increased percentage of second

lien loan originations to total loans originated in

2005 and the first half of 2006, and the underwriting

of stated income (low documentation) products. The

US net loan impairment charges increased by 37 per

cent after taking into account the most recent trends