HSBC 2006 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2006 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

|

|

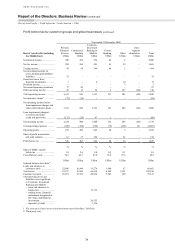

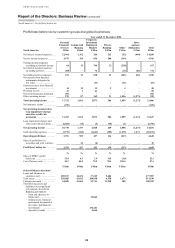

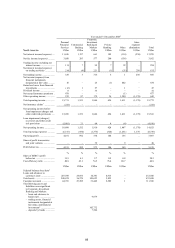

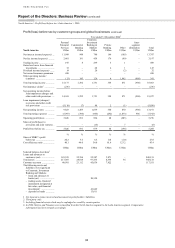

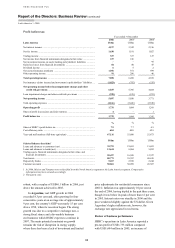

HSBC HOLDINGS PLC

Report of the Directors: Business Review (continued)

North America > 2005

84

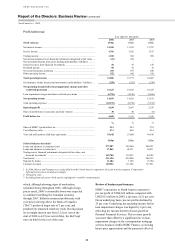

businesses. These volume benefits were largely

offset by narrowing spreads as yields fell due to

changes in product mix and higher funding costs.

Prime mortgages originated in 2005 were

largely sold into the large government-sponsored

mortgage associations, reflecting a strategic decision

to focus on loans originated through the retail

channel and reduce HSBC’s reliance on lower

spread business generated by the network of

mortgage correspondents. The improvements in

retail channel sales were achieved by capitalising on

the HSBC brand, and the newly expanded branch

network and customer base. As interest rates rose,

demand for ARM products in 2005 declined as

customers migrated towards longer-term fixed rate

mortgages. ARM-originated loans fell from 67 per

cent of all loans originated in 2004 to 30 per cent in

2005. Spreads narrowed on prime mortgages, largely

because of higher funding costs and marginally

lower yields, the latter due to the full year effect of

the strong growth of lower-yielding ARMs

originated in 2004.

HSBC continued to grow its sub-prime and

near-prime mortgage portfolios, primarily within the

mortgage services and branch-based consumer

lending businesses. The mortgage services business,

which purchases mortgage loans from a network of

correspondents, recorded strong average loan growth

of 42 per cent to US$39.1 billion, of which

US$1.7 billion related to mortgages held for resale.

Continued focus on growing the second lien

portfolio, widening the first lien product offering and

expanding sources for the purchase of loans from

‘flow’ correspondents contributed further to the

increase. Within the branch-based consumer lending

business, average mortgage balances grew by 19 per

cent to US$35.7 billion, reflecting a combination of

increased marketing activity and higher sales

volumes of near-prime mortgages and ARMs, first

introduced in the second half of 2004. In addition,

the consumer lending business purchased

US$1.7 billion of largely sub-prime mortgage loans

through a portfolio acquisition programme. The

benefits of higher sub-prime and near-prime

balances were largely offset by lower spreads. Yields

fell due to the combined effects of strong refinancing

activity, significant amounts of older higher-yielding

loans seasoning, continued product expansion into

the near-prime customer segments and competitive

pricing pressures. The higher cost of funds due to

rising interest rates also contributed to the decline in

spreads.

Average loan balances within the consumer

finance credit cards business rose by 7 per cent to

US$19.8 billion, despite the highly competitive

environment, where overall market growth remained

weak. By increasing the level of marketing

promotions, HSBC was able to grow organically the

HSBC branded prime, Union Privilege and non-

prime portfolios. The benefit of higher balances was

more than offset by higher funding costs. Yields,

however, improved due to a combination of higher-

yielding sub-prime receivable balances, increased

pricing on variable rate products and other re-pricing

initiatives.

In the retail services cards business, average

loan balances grew by 7 per cent to US$15.9 billion.

This growth was driven by new loan originations and

the agreement of new merchant relationships with

The Neiman Marcus Group Inc, Bon Ton Stores Inc

and OfficeMax, which contributed US$506 million

of the overall increase. The benefit of higher loan

balances was more than offset by lower spreads.

Spreads declined as a large proportion of the loan

book, priced at fixed rates, was affected by higher

funding costs as interest rates rose. Spreads also

narrowed as changes in the product mix reflected

strong growth of lower-yielding recreational vehicle

balances and external pricing pressures. Changes in

contractual obligations associated with a merchant

also had an adverse effect, but this resulted in lower

merchant fees payable.

The vehicle finance business reported strong

organic growth, with a 14 per cent increase in

average loan balances, largely due to increases in the

near-prime portfolio. This growth in balances was

mainly driven by a combination of higher new loan

originations acquired from the dealer network, in

part due to the success of the ‘employee pricing’

incentive programmes introduced by a number of the

large car manufacturers, and strong growth in the

consumer direct loan programme. A new strategic

alliance helped grow loans further, generating

US$234 million of new balances. These volume

benefits were largely offset by lower spreads, due to

higher funding costs and lower yields. Yields fell

due to product expansion into the near-prime

portfolio, coupled with competitive pricing pressures

due to excess market capacity.

Personal non-credit card average loan balances

in the consumer finance business grew by 8 per cent

to US$16.0 billion, reflecting the success of several

large direct mail campaigns and increased

availability of this product in the US market.

Improvements in underwriting processes, aided by

continued improvements in the US economy, also

contributed to the increase. These benefits were

partly offset by lower spreads, due to higher funding

costs.