Dollar General 2015 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2015 Dollar General annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

|

|

Proxy

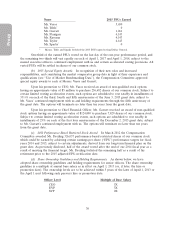

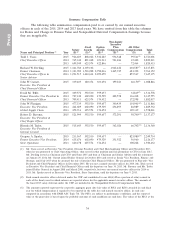

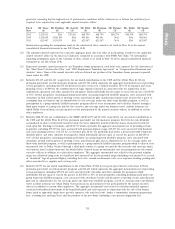

Considerations Associated with Regulatory Requirements

Under Section 162(m) of the Internal Revenue Code, we generally may not take a tax

deduction for individual compensation over $1 million paid in any taxable year to each of the persons

who were, at the end of the fiscal year, our CEO or one of the other named executive officers (other

than our Chief Financial Officer). As a result, we may not deduct any salary, signing bonus or other

annual compensation paid or imputed to such covered officers that causes non-performance-based

compensation to exceed the $1 million limit. Certain performance-based compensation is exempt from

the deduction limit.

We believe that our Amended and Restated 2007 Stock Incentive Plan and our Amended and

Restated Annual Incentive Plan currently satisfy the requirements of Section 162(m). As a result, we

may deduct compensation expense realized in connection with any (1) payments made under our

Teamshare program, (2) stock options and stock appreciation rights, and (3) performance-based

restricted stock and RSU awards. However, restricted stock or RSUs that solely vest over time are not

‘‘performance-based compensation’’ under Section 162(m), and we will be unable to deduct

compensation expense realized in connection with those time-vested awards to persons covered by

Section 162(m) to the extent their non-performance-based compensation exceeds $1 million. Our

policies do not restrict the Compensation Committee from exercising discretion to approve

compensation packages that may result in certain non-deductible compensation expenses but that the

Committee nonetheless determines to be in our shareholders’ best interests.

The Committee administers our executive compensation program with the good faith intention

of complying with Section 409A of the Internal Revenue Code, which relates to the taxation of

nonqualified deferred compensation arrangements.

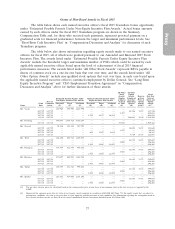

Compensation Committee Report

The Compensation Committee of our Board of Directors reviewed and discussed with

management the Compensation Discussion and Analysis required by Item 402(b) of Regulation S-K

and, based on such review and discussions, the Compensation Committee recommended to the Board

that the Compensation Discussion and Analysis be included in this document.

This report has been furnished by the members of the Compensation Committee:

• Warren F. Bryant, Chairman

• Patricia D. Fili-Krushel

• William C. Rhodes, III

The above Compensation Committee Report does not constitute soliciting material and should not

be deemed filed or incorporated by reference into any other Dollar General filing under the Securities Act of

1933 or the Securities Exchange Act of 1934, except to the extent Dollar General specifically incorporates

this report by reference therein.

33