Dollar General 2015 Annual Report Download - page 112

Download and view the complete annual report

Please find page 112 of the 2015 Dollar General annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

|

|

10-K

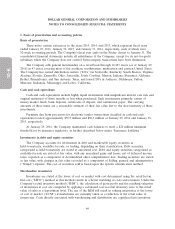

which includes an analysis of whether such loss estimates are probable, reasonably possible, or remote.

We re-evaluate these assessments on a quarterly basis or as new and significant information becomes

available to determine whether a liability should be established or if any existing liability should be

adjusted. The actual cost of resolving a claim or proceeding ultimately may be substantially different

than the amount of the recorded liability. In addition, because it is not permissible under U.S. GAAP

to establish a litigation liability until the loss is both probable and estimable, in some cases there may

be insufficient time to establish a liability prior to the actual incurrence of the loss (upon verdict and

judgment at trial, for example, or in the case of a quickly negotiated settlement).

Lease Accounting and Excess Facilities. Many of our stores are subject to build-to-suit

arrangements with landlords, which typically carry a primary lease term of up to 15 years with multiple

renewal options. We also have stores subject to shorter-term leases and many of these leases have

renewal options. Certain of our stores have provisions for contingent rentals based upon a percentage

of defined sales volume. We recognize contingent rental expense when the achievement of specified

sales targets is considered probable. We record minimum rental expense on a straight-line basis over

the base, non-cancelable lease term commencing on the date that we take physical possession of the

property from the landlord, which normally includes a period prior to store opening to make necessary

leasehold improvements and install store fixtures. When a lease contains a predetermined fixed

escalation of the minimum rent, we recognize the related rent expense on a straight-line basis and

record the difference between the recognized rental expense and the amounts payable under the lease

as deferred rent. Tenant allowances, to the extent received, are recorded as deferred incentive rent and

amortized as a reduction to rent expense over the term of the lease. We reflect as a liability any

difference between the calculated expense and the amounts actually paid. Improvements of leased

properties are amortized over the shorter of the life of the applicable lease term or the estimated

useful life of the asset.

Share-Based Payments. Our stock option awards are valued on an individual grant basis using the

Black-Scholes-Merton closed form option pricing model. We believe that this model fairly estimates the

value of our stock option awards. The application of this valuation model involves assumptions that are

judgmental in the valuation of stock options, which affects compensation expense related to these

options. These assumptions include the term that the options are expected to be outstanding, the

historical volatility of our stock price, applicable interest rates and the dividend yield of our stock.

Other factors involving judgments that affect the expensing of share-based payments include estimated

forfeiture rates of share-based awards. Historically, these estimates have been materially accurate;

however, if our estimates differ materially from actual experience, we may be required to record

additional expense or reductions of expense, which could be material to our future financial results.

Fair Value Measurements. Accounting standards for the measurement of fair value of assets and

liabilities establish a fair value hierarchy that distinguishes between market participant assumptions

based on market data obtained from sources independent of the reporting entity (observable inputs

that are classified within Levels 1 and 2 of the hierarchy) and the reporting entity’s own assumptions

about market participant assumptions (unobservable inputs classified within Level 3 of the hierarchy).

Therefore, Level 3 inputs are typically based on an entity’s own assumptions, as there is little, if any,

related market activity, and thus require the use of significant judgment and estimates. Currently, we

have no assets or liabilities that are valued based solely on Level 3 inputs.

Our fair value measurements are primarily associated with our outstanding debt instruments. We

use various valuation models in determining the values of these liabilities. We believe that in recent

years these methodologies have produced materially accurate valuations.

38