Dollar General 2015 Annual Report Download - page 109

Download and view the complete annual report

Please find page 109 of the 2015 Dollar General annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

|

|

10-K

improvements, fixtures and equipment; the construction of new stores; costs to support and enhance

our supply chain initiatives including new and existing distribution center facilities; technology

initiatives; as well as routine and ongoing capital requirements.

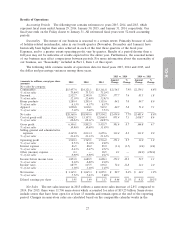

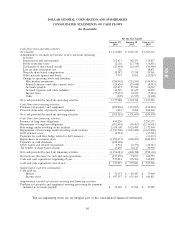

Cash flows from financing activities. In 2015, we repurchased 17.6 million outstanding shares of

our common stock at a total cost of $1.3 billion. We made repayments of $500.0 million on the balance

of the Term Facility, and had proceeds of $499.2 million from the issuance of senior notes. Net

borrowings under the Revolving Facility during 2015 were $251.0 million.

In 2014, we repurchased 14.1 million outstanding shares of our common stock at a total cost of

$800.1 million. We made repayments of $75.0 million on the balance of the Term Facility. Borrowings

and repayments under the Revolving Facility during the 2014 period were the same amount, resulting

in no net increase to amounts outstanding under the Revolving Facility during 2014.

The 2013 cash flows from financing activities reflect a refinancing in April 2013, including the

issuance of long-term obligations which includes the $1.0 billion unsecured Term Facility and the

issuance of Senior Notes totaling approximately $1.3 billion. Proceeds from these transactions were

used to repay our previous secured term loan and revolving credit facilities which had balances of

$1.96 billion and $155.6 million when refinanced. Net repayments under the Revolving Facility were

$130.9 million during 2013. We paid debt issuance costs and hedging fees totaling $29.2 million in 2013

related to the refinancing. Also in 2013, we repurchased 11.0 million outstanding shares of our common

stock at a total cost of $620.1 million.

Accounting Standards

In February 2016, the FASB issued new guidance related to lease accounting. This guidance

requires a dual approach for lessee accounting under which a lessee will account for leases as finance

leases or operating leases. Both finance leases and operating leases will result in the lessee recognizing

a right-of-use asset and a corresponding lease liability on its balance sheet, with differing methodology

for income statement recognition. This guidance is effective for public business entities for fiscal years,

and interim periods within those years, beginning after December 15, 2018, and early adoption is

permitted. A modified retrospective approach is required for all leases existing or entered into after the

beginning of the earliest comparative period in the consolidated financial statements. We are currently

assessing the impact that adoption of this guidance will have on our consolidated financial statements,

and we are anticipating a material impact because of our significant volume of lease contracts.

Critical Accounting Policies and Estimates

The preparation of financial statements in accordance with generally accepted accounting

principles in the United States (‘‘U.S. GAAP’’) requires management to make estimates and

assumptions that affect reported amounts and related disclosures. In addition to the estimates

presented below, there are other items within our financial statements that require estimation, but are

not deemed critical as defined below. We believe these estimates are reasonable and appropriate.

However, if actual experience differs from the assumptions and other considerations used, the resulting

changes could have a material effect on the financial statements taken as a whole.

Management believes the following policies and estimates are critical because they involve

significant judgments, assumptions, and estimates. Management has discussed the development and

selection of the critical accounting estimates with the Audit Committee of our Board of Directors, and

the Audit Committee has reviewed the disclosures presented below relating to those policies and

estimates. See Note 1 to the consolidated financial statements for a detailed discussion of our principal

accounting policies.

35