Capital One 2002 Annual Report Download - page 9

Download and view the complete annual report

Please find page 9 of the 2002 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

|

|

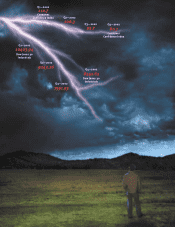

Our to auto lending

is … well … turning a lot of keys.

Capital One

®

is successfully putting its credit card expertise to work in the broader consumer

lending market, where we see big opportunities for profitable long-term growth.

Auto finance, with more than $1 trillion in loans outstanding, is nearly twice the size of the credit card

market. After two acquisitions and four years of making auto loans, Capital One has a $7 billion portfolio

with steadily improving profitability. Our skill in analyzing credit risk and pricing each loan accordingly creates a

win-win situation for us and our customers: we minimize lending risk, they get the best deal. As we’ve built scale,

we’ve dramatically cut operating costs, from nearly 10% of loans outstanding in 1999 to 3.57% in 2002.

Our superprime auto finance business continues to grow rapidly despite the auto industry’s offers of low- or

no-interest financing. Many consumers who do the math realize that they’ll come out ahead by combining

a car manufacturer’s offer of a cash rebate with financing from Capital One Auto Finance. The largest Internet

originator of auto loans, Capital One Auto Finance gives superprime borrowers no-hassle service and convenient

access to financing, features that are generating exceptionally high levels of customer satisfaction.

In the $175 billion installment lending business, we market personal loans to superprime borrowers,

high-income people with long and stellar credit histories. The low risk allows us to offer the loans at an

exceptionally low fixed rate—7.9% in many cases, which is five percentage points below the industry average.

Installment lending has added $4 billion in blue-chip assets to Capital One’s managed loans.

In 2002, we entered the small-business lending sector. With a Capital One business credit card, a small

entrepreneur has hassle-free access to loans for operating capital—a big help in smoothing out cash flow and

meeting extraordinary expenses. Our small-business lending is growing rapidly and yielding above-average returns.

The auto finance, installment and small-business lending markets are highly fragmented, presenting opportunitie

s

for significant gains in market share. We believe our information-based strategy will allow us to transform these

businesses through direct marketing, innovative products and customization. The payoffs: better deals and less

hassle for borrowers and new sources of profitable growth for Capital One.

turnkey approach

7