Capital One 2002 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2002 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

|

|

40

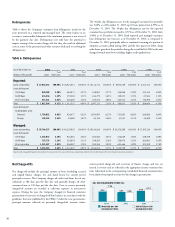

part of the ongoing supervision of the Bank and the Savings Bank, the

Company will periodically report to, and consult with, the regulators on all

the matters addressed under the informal memorandum of understanding.

While the Company has delivered on the principal requirements of the

informal memorandum of understanding, it expects its regulators to monitor

its ongoing execution for some period of time. Hence, the Company is

unable to predict the exact timing for conclusion or termination of the

informal memorandum of understanding.

FFIEC

On January 8, 2003 the FFIEC released Account Management and Loss

Allowance Guidance (the “Guidance”). The Guidance applies to all credit

lending of regulated financial institutions and generally requires that banks

properly manage several elements of their credit-card lending programs, including

line assignments, over-limit practices, minimum payment and negative

amortization, workout and settlement programs and the accounting

methodology used for various assets and income items related to credit card loans.

The Company believes that its credit card account management and loss

allowance practices are prudent and appropriate and, therefore, consistent

with the Guidance. Based on this review and these discussions, the Company

believes the Guidance will not have a material adverse effect on its financial

condition or results of operations. The Company cautions, however, that

similar to the Subprime Guidelines, the Guidance provides wide discretion to

bank regulatory agencies in the application of the Guidance to any particular

institution and its account management and loss allowance practices.

Accordingly, under the Guidance, bank examiners could require changes in

the Company’s account management or loss allowance practices in the future.

Sarbanes-Oxley

On July 30, 2002, the Sarbanes-Oxley Act of 2002 (the “Sarbanes-Oxley

Act”) was passed into law. The Sarbanes-Oxley Act applies to all companies

that are required to file periodic reports with the Securities Exchange

Commission (“SEC”) and contains a number of significant changes relating to

the responsibilities of directors and officers and reporting and governance

obligations of SEC reporting companies. Certain provisions of the Sarbanes-

Oxley Act were effective immediately without action by the SEC; however

many provisions became effective over the months following its passage and

required the SEC to issue implementing rules. Following the passage of the

Sarbanes-Oxley Act, the Company has taken steps which it believes places it in

substantial compliance with the effective provisions of the Sarbanes-Oxley Act

and it continues to monitor SEC rulemaking to determine if additional

changes are needed to comply with provisions that will become effective over

the following months. During the course of its compliance efforts, the

Company has identified no significant changes which must be made to its

organizational and control structures or existing processes as a result of this

legislation and the currently effective rules issued by the SEC and other

regulatory bodies.

In August 2000, the Bank received regulatory approval and established a

subsidiary bank in the United Kingdom. In connection with the approval of

its former branch office in the United Kingdom, the Company committed to

the Federal Reserve that, for so long as the Bank maintains a branch or

subsidiary bank in the United Kingdom, the Company will maintain a

minimum Tier 1 Leverage ratio of 3.0%. As of December 31, 2002 and

2001, the Company’s Tier 1 Leverage ratio was 11.95% and 11.93%,

respectively.

Additionally, federal banking law limits the ability of the Bank and Savings

Bank to transfer funds to the Corporation. As of December 31, 2002,

retained earnings of the Bank and the Savings Bank of $924.4 million and

$408.4 million, respectively, were available for payment of dividends to the

Corporation without prior approval by the regulators. The Savings Bank,

however, is required to give the OTS at least 30 days advance notice of any

proposed dividend and the OTS, in its discretion, may object to such

dividend.

Additional information regarding capital adequacy can be found in Note O

to the Consolidated Financial Statements.

Dividend Policy

Although the Company expects to reinvest a substantial portion of its earnings

in its business, the Company also intends to continue to pay regular quarterly

cash dividends on its common stock. The declaration and payment of dividends,

as well as the amount thereof, are subject to the discretion of the Board of

Directors of the Company and will depend upon the Company’s results of

operations, financial condition, cash requirements, future prospects and other

factors deemed relevant by the Board of Directors. Accordingly, there can be no

assurance that the Corporation will declare and pay any dividends. As a holding

company, the ability of the Corporation to pay dividends is dependent upon the

receipt of dividends or other payments from its subsidiaries. Applicable banking

regulations and provisions that may be contained in borrowing agreements of

the Corporation or its subsidiaries may restrict the ability of the Corporation’s

subsidiaries to pay dividends to the Corporation or the ability of the

Corporation to pay dividends to its stockholders.

LEGISLATIVE AND REGULATORY MATTERS

Informal Memorandum of Understanding

As described in the Company’s report on Form 10-Q, dated August 13,

2002, the Company has entered into an informal memorandum of

understanding with the bank regulatory authorities with respect to certain

issues, including capital, allowance for loan losses, finance charge and fee

reserves and policies, procedures, systems and controls. A memorandum of

understanding is characterized by regulatory authorities as an informal

action, that is not published or publicly available. The Company has

implemented levels of capital, reserves and allowances that it believes satisfy

the memorandum of understanding.

In addition, as required under the memorandum of understanding, the

Company has continued to take actions, among others, to enhance its

enterprise risk management framework and legal entity business plans. As