Capital One 2002 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2002 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

|

|

43

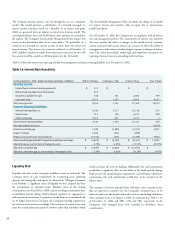

improvement is in spite of the weakness in the U.S. economy over the last

few years, as well as softness in the prices of used cars the company has been

able to garner in the wholesale used car market when selling repossessed

vehicles. However, U.S. unemployment statistics have been rising recently,

which could have an adverse impact on our default rates going forward.

Despite these pressures, Capital One remains cautiously optimistic that it can

continue to steadily and profitably grow market share and profits in the auto

finance segment.

International Segment

This segment consists of $5.4 billion of credit card receivables, principally

originated and operated in the U.K. and Canada. Additionally, the Company

has been testing and plans to continue to test new geographic markets.

The improvement in the Company’s financial performance over the past

twelve months is due to the maturation of the Company’s businesses in the

U.K. and Canada. Both of these businesses are generating profitable portfolio

growth, realizing lower operating expenses and steadily improving risk

management. Additionally, price competition in the superprime card

business in 2002 appears to have subsided somewhat from the intense levels

experienced in 2001 and 2000.

In 2002, the Company also launched its “What’s in Your Wallet?” and “No-

Hassle” brand campaigns in the U.K. This strong focus on brand marketing

activity, combined with industry leading rates and products, has enabled our

U.K. business to continually rank among the top three issuers of new credit

cards in the U.K. market in terms of managed loans outstanding.

The Company is highly committed to diversifying into new geographies and

sees the continued success of our International segment as an indication of

the global potential of our core IBS strategy.

Likewise, the Company’s credit card products marketed to consumers with

less established or higher risk credit profiles continue to experience steady

competition. These products generally feature higher annual percentage rates,

lower credit lines, and annual membership fees. Additionally, since these

borrowers are viewed by issuers as higher risk, they tend to be more likely to

pay late or exceed their credit limit, which results in additional fees assessed

to their accounts. The Company’s strategy has been, and is expected to

continue to be, to offer APRs and annual membership, late and overlimit fees

on these accounts that are below those of its competition.

Auto Finance Segment

This segment consists of $7.0 billion of U.S. auto loan receivables, marketed

to both superprime and subprime customers, via direct and indirect

marketing channels. The Company originated approximately two-thirds of

our 2002 auto loan growth via direct channels such as the Internet and direct

mail, and the remaining one-third via the indirect auto dealer channel. The

Company is also testing the auto lending prime market and have an

immaterial amount of receivables in this portion of the credit spectrum at

this time. It is the Company’s goal to become a full spectrum auto finance

lender, much like it has achieved in the U.S. credit card industry. In addition

to the competitive advantages of being a full credit spectrum lender discussed

above, the scale sensitive nature of the auto finance business generates

additional economic leverage for full spectrum competitors. Additionally in

2002, the Company sold $1.5 billion of superprime auto assets in whole loan

sale transactions to multiple buyers. The high credit quality of these

borrowers leads to very low loss rates on these assets (averaging 15-20 basis

points per annum). Additionally, the Company is continuing to service these

assets for a fee.

In the fourth quarter of 2002, the Company entered into a forward flow

agreement with a purchaser to sell subprime auto loans originated via our

subprime auto dealer network. These assets are sold at a premium, servicing

released, no recourse, and have an additional performance payment in the

future depending on asset performance over time. These assets are originated

using the Company’s underwriting policies, and allow for the sale of $65.0

million to $110.0 million of assets per month. The Company expects to sell

between $500.0 million and $900.0 million of subprime auto loans under

this agreement in 2003.

Going forward, the Company anticipates that it will continue to sell auto

loans. The benefits of selling our excess origination volume are twofold. First,

the Company continues to generate more scale economies from the

additional volume. Second, the Company is able to sell loans for a price that

exceed the cost of origination, thus whole loan sales have become a profit

center for Capital One.

Credit quality in the superprime auto finance segment has remained strong,

with net chargeoffs in the 15-20bp range in 2003. Net chargeoffs in the sub-

prime auto segment have continued to improve, on a static pool basis, in

each year that Capital One has participated in the sector. This steady