Capital One 2002 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2002 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

|

|

31

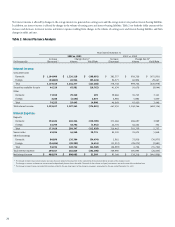

growth. Table 7 shows the Company’s net charge-offs for the years presented

on a reported and managed basis.

The Company takes measures as necessary, including requiring collateral on

certain accounts and other marketing and account management techniques,

to maintain the Company’s credit quality standards and to manage the risk of

loss on existing accounts. See “Risk Adjusted Revenue and Margin” for

further discussion.

For the year ended December 31, 2002, the managed net charge-off rate

increased 59 basis points to 5.24% compared to the prior year. For the year

ended December 31, 2002, the reported net charge-off rate increased 17 basis

points to 4.93%. The increase in both the managed and reported net charge-

off rates was the result of a seasoning of subprime loans added in the fourth

quarter 2001 and early 2002 to the Company’s portfolio and slower loan

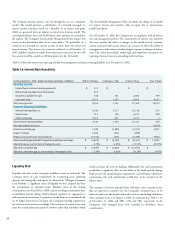

Provision For Loan Losses

The allowance for loan losses is maintained at an amount estimated to be

sufficient to absorb probable losses, net of principal recoveries (including

recovery of collateral), inherent in the existing reported loan portfolio. The

provision for loan losses is the periodic cost of maintaining an adequate

allowance. Management believes that, for all relevant periods, the allowance

for loan losses was adequate to cover anticipated losses in the total reported

consumer loan portfolio under then current conditions, met applicable legal

and regulatory guidance and was consistent with GAAP. There can be no

assurance as to future credit losses that may be incurred in connection with

the Company’s consumer loan portfolio, nor can there be any assurance that

the loan loss allowance that has been established by the Company will be

sufficient to absorb such future credit losses. The allowance is a general

allowance applicable to the reported homogeneous consumer loan portfolio.

The amount of allowance necessary is determined primarily based on a

migration analysis of delinquent and current accounts and forward loss

curves. In evaluating the sufficiency of the allowance for loan losses,

management also takes into consideration the following factors: recent trends

in delinquencies and charge-offs including bankrupt, deceased and recovered

amounts; forecasting uncertainties and size of credit risks; the degree of risk

inherent in the composition of the loan portfolio; economic conditions; legal

and regulatory guidance (including the “Expanded Guidance for Subprime

Lending Programs” (“Subprime Guidelines”) issued by the four federal

banking agencies); credit evaluations and underwriting policies.

For the year ended December 31, 2002, the provision for loan losses

increased to $2.1 billion, or 92%, from the 2001 provision for loan losses of

$1.1 billion. This increase is primarily a result of the 48% increase in average

reported loans, a rise in net charge-offs, the revised application of the Subprime

Guidelines, and the aforementioned one-time impact of the $133.4 million

change in recoveries estimate (see “Change in Recoveries Classification” above).

The Company applied its allowance models, including these factors, and

increased the allowance for loan losses by a total of $880.0 million during 2002.

For the year ended December 31, 2001, the provision for loan losses increased

to $1.1 billion, or 38%, from the 2000 provision for loan losses of $812.9

million. This increase is primarily a result of the 50% increase in average

reported loans, offset by a 70 basis point, or 13%, decrease in the reported net

charge-off rates as a result of the shift in the mix of the composition of the

reported portfolio. As a result of these factors, the Company increased the

allowance for loan losses by $313.0 million during 2001.

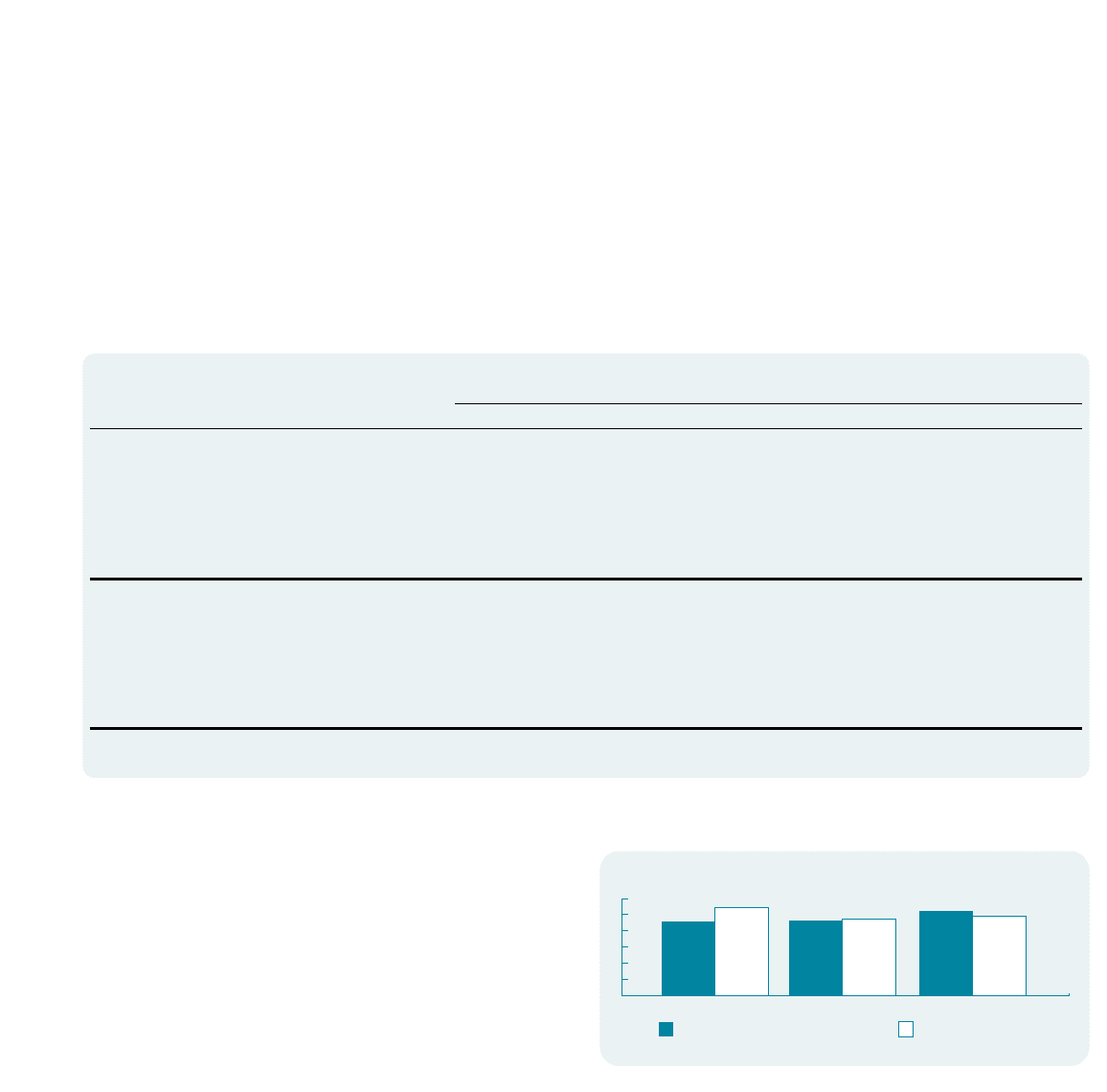

Table 7: Net Charge-offs

Year Ended December 31

(Dollars in Thousands) 2002 2001 2000 1999 1998

Reported:

Average loans outstanding $ 25,539,996 $ 17,284,306 $ 11,487,776 $ 7,667,355 $ 5,348,559

Net charge-offs 1,259,684 822,257 627,312 318,992 248,344

Net charge-offs as a percentage of

average loans outstanding 4.93% 4.76% 5.46% 4.16% 4.64%

Managed:

Average loans outstanding $ 52,799,566 $ 35,612,617 $ 22,634,862 $ 18,046,913 $ 15,209,537

Net charge-offs 2,769,249 1,655,947 1,031,590 782,537 858,955

Net charge-offs as a percentage of

average loans outstanding 5.24% 4.65% 4.56% 4.34% 5.65%

MANAGED NET

CHARGE-OFF RATE

2001

5.24

2002

4.93

4.65 4.76

2000

4.56

5.46

REPORTED NET

CHARGE-OFF RATE

NET CHARGE-OFF RATE (%)