Capital One 2002 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2002 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

|

|

53

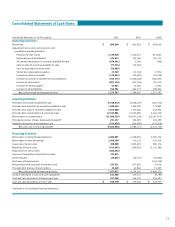

premiums and accretion of discounts to maturity. Such amortization or

accretion is included in interest income. Realized gains and losses on sales of

securities are determined using the specific identification method.

REVENUE RECOGNITION

The Company recognizes earned finance charges and fee income on loans

according to the contractual provisions of the credit agreements. When,

based on historic performance of the portfolio, payment in full of finance

charge and fee income is not expected, the estimated uncollectible portion is

not accrued as income. As discussed below, the 2002 change in recoveries

estimate resulted in an $82.7 million reduction of finance charges and fees

deemed uncollectible for the year ended December 31, 2002. Amounts

collected on previously charged-off accounts related to finance charges and

fees are recognized as income. Costs to recover previously charged-off

accounts are recorded as collection expense in non-interest expenses.

Interchange income is a fee paid by a merchant bank to the card-issuing bank

through the interchange network. Interchange fees are set by MasterCard

International Inc. and Visa U.S.A. Inc. and are based on cardholder purchase

volumes. The Company recognizes interchange income as earned. The

Company offers to its customers certain rewards programs based on purchase

volumes. The provision for the cost of the rewards programs is based upon

points awarded in the current year which are ultimately expected to be

redeemed by program members and the current average cost per point of

redemption. The cost of these rewards programs is deducted from

interchange income. The cost of the rewards programs related to securitized

loans is deducted from servicing and securitizations income.

Annual membership fees and direct loan origination costs are deferred and

amortized over one year on a straight-line basis. Direct loan origination costs

consist of both internal and external costs associated with the origination of a

loan. Deferred fees (net of deferred costs of $45.2 million and $55.1 million

in 2002 and 2001, respectively) were $325.9 million and $291.6 million as

of December 31, 2002 and 2001, respectively.

LOAN SECURITIZATIONS

Loan securitization involves the sale, generally to a trust or other special

purpose entity, of a pool of loan receivables and is accomplished primarily

through the public and private issuance of asset-backed securities by the

special purpose entity. The Company removes loan receivables from the

consolidated balance sheet for those asset securitizations that qualify as sales

in accordance with SFAS 140. The trusts are qualifying special purpose

entities as defined by SFAS 140. For those asset securitizations that qualify as

sales in accordance with SFAS 140, the trusts to which the loans were sold are

not subsidiaries of the Company, and are not included in the Company’s

consolidated financial statements in accordance with GAAP. Gains on

securitization transactions, fair value adjustments and servicing and other

income on the Company’s securitizations are included in servicing and

securitizations non-interest income in the consolidated statements of income

and amounts due from the trusts are included in accounts receivable from

securitizations on the consolidated balance sheets.

In April of 2002, the FASB issued SFAS No. 145, Rescission of FASB

Statements No. 4, 44, and 64, Amendment of FASB Statement No. 13, and

Technical Corrections (“SFAS 145”). SFAS No. 145 rescinds SFAS No. 4,

Reporting Gains and Losses from Extinguishment of Debt, and an amendment of

that Statement, SFAS No. 64, Extinguishments of Debt Made to Satisfy Sinking-

Fund Requirements. This Statement also amends other existing authoritative

pronouncements to make various technical corrections, clarify meanings, or

describe their applicability under changed conditions. SFAS 145 became

effective and was adopted by the Company in May of 2002 and did not have

an impact on the consolidated earnings or financial position of the Company.

In August 2001, the FASB issued SFAS No. 144, Accounting for the

Impairment or Disposal of Long-Lived Assets (“SFAS 144”). SFAS 144

supersedes SFAS No. 121, Accounting for the Impairment of Long-Lived Assets

and for Long-Lived Assets to Be Disposed Of (“SFAS 121”), but retains the

requirements of SFAS 121 to test long-lived assets for impairment and

removes goodwill from its scope. In addition, the changes presented in SFAS

144 require that one accounting model be used for long-lived assets to be

disposed of by sale and broadens the presentation of discontinued operations

to include more disposal transactions. Under SFAS 144, discontinued

operations are no longer measured on a net realizable value basis, and future

operating losses are no longer recognized before they occur. The provisions of

this Statement are effective for financial statements issued for fiscal years

beginning after December 15, 2001. The implementation of SFAS 144 did

not have a material impact on the consolidated earnings or financial position

of the Company.

In June 2001, the FASB issued SFAS No. 141, Business Combinations (“SFAS

141”), effective for business combinations initiated after June 30, 2001, and

SFAS No. 142, Goodwill and Other Intangible Assets (“SFAS 142”), effective

for fiscal years beginning after December 15, 2001. Under SFAS 141, the

pooling of interests method of accounting for business combinations is

eliminated. Under SFAS 142, goodwill and intangible assets deemed to have

indefinite lives will no longer be amortized but will be subject to annual

impairment tests in accordance with the pronouncement. Other intangible

assets will continue to be amortized over their useful lives. Under the

transitional provisions of SFAS 142, the Company identified its reporting

units and performed the first of the required impairment tests of net goodwill

and indefinite-lived intangible assets during 2002. The testing resulted in no

impairment losses to any recorded goodwill of the Company.

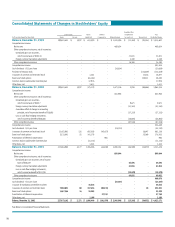

CASH AND CASH EQUIVALENTS

Cash and cash equivalents includes cash and due from banks, federal funds

sold and resale agreements and interest-bearing deposits at other banks. Cash

paid for interest for the years ended December 31, 2002, 2001 and 2000 was

$1.4 billion, $1.1 billion and $.8 billion, respectively. Cash paid for income

taxes for the years ended December 31, 2002, 2001 and 2000 was $585.8

million, $70.8 million and $237.2 million, respectively.

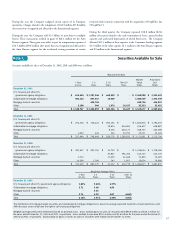

SECURITIES AVAILABLE FOR SALE

The Company classifies all debt securities as securities available for sale. These

securities are stated at fair value, with the unrealized gains and losses, net of

tax, reported as a component of cumulative other comprehensive income.

The amortized cost of debt securities is adjusted for amortization of