Aflac 2006 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2006 Aflac annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

|

|

59

investment. If, based on our reviews, we determine that the

issuer has the ability to continue to service our investment; we

conclude that the investment is temporarily impaired. Because

we have the ability and intent to hold these investments until

a recovery of fair value, which may be maturity, we do not

consider these investments to be other-than-temporarily

impaired at December 31, 2006.

Included in the unrealized losses on Other corporate fixed-

maturity securities is an unrealized loss of $56 million on Aflac

Japan’s $201 million (¥24 billion) investment in Tollo Shipping

Company S.A. Our investment is guaranteed by the issuer’s

parent, Compañia Sudamericana de Vapores S.A. (CSAV). The

decline in fair value of the security was primarily caused by

two factors: depressed revenue due to competitive pricing

pressures in the container shipping industry and weaker

operating margins due to sharply increased fuel costs. The

contractual terms of this investment do not permit the issuer

or its parent to settle the security at a price less than the

amortized cost of the investment, and give priority to

repayment of our investment under certain circumstances.

While CSAV’s credit rating has decreased from BBB- to BB+

(S&P), we currently believe it is probable that we will collect all

amounts due according to the contractual terms of the

investment. Therefore, it is expected that our investment

would not be settled at a price less than the amortized cost of

the investment. Because we have the intent and ability to hold

this investment until a recovery of fair value, which may be

maturity, we do not consider it to be other-than-temporarily

impaired as of December 31, 2006.

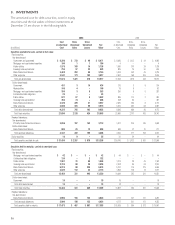

The net effect on shareholders’ equity of unrealized gains and

losses from investment securities at December 31 was as

follows:

(In millions) 2006 2005

Unrealized gains on securities available for sale $ 1,783 $ 2,452

Unamortized unrealized gains on securities transferred

to held to maturity 378 430

Deferred income taxes (711) (965)

Shareholders’ equity, unrealized gains

on investment securities $ 1,450 $ 1,917

We attempt to match the duration of our assets with the

duration of our liabilities. The following table presents the

approximate duration of our yen-denominated assets and

liabilities, along with premiums, as of December 31.

(In years) 2006 2005

Yen-denominated debt securities 13 12

Policy benefits and related expenses to be paid in future years 13 13

Premiums to be received in future years on policies in force 10 10

Currently, when our debt securities mature, the proceeds may

be reinvested at a yield below that of the interest required for

the accretion of policy benefit liabilities on policies issued in

earlier years. However, our strategy of developing and

marketing riders to our older policies has helped offset the

negative investment spread. In spite of the negative

investment spreads, overall profit margins in Aflac Japan’s

aggregate block of business are adequate because of profits

that continue to emerge from changes in mix of business and

favorable mortality, morbidity, and expenses.

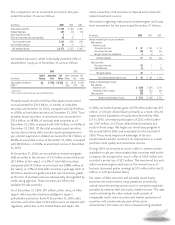

The contractual maturities of our investments in fixed

maturities at December 31, 2006, were as follows:

Aflac Japan Aflac U.S.

Amortized Fair Amortized Fair

(In millions) Cost Value Cost Value

Available for sale:

Due in one year or less $ 584 $ 603 $ 20 $ 20

Due after one year through five years 3,371 3,858 357 382

Due after five years through 10 years 2,943 3,381 486 536

Due after 10 years 13,542 13,888 5,152 5,496

Mortgage- and asset-backed securities 312 314 229 225

Total fixed maturities

available for sale $ 20,752 $ 22,044 $ 6,244 $ 6,659

Held to maturity:

Due in one year or less $ 43 $ 44 $ – $ –

Due after one year through five years 480 518 – –

Due after five years through 10 years 1,042 1,129 – –

Due after 10 years 11,857 11,617 19 19

Mortgage- and asset-backed securities 42 42 – –

Total fixed maturities

held to maturity $ 13,464 $ 13,350 $ 19 $ 19

The Parent Company has a portfolio of investment-grade

available-for-sale fixed-maturity securities totaling $103 million

at amortized cost and $102 million at fair value, which is not

included in the preceding table.

Expected maturities may differ from contractual maturities

because some issuers have the right to call or prepay

obligations with or without call or prepayment penalties.

We own subordinated perpetual debenture securities. These

securities are subordinated to other debt obligations of the

issuer, but rank higher than equity securities. Although these

securities have no contractual maturity, the interest coupons

that were fixed at issuance subsequently change to a floating

short-term interest rate of 125 to 300 basis points above

market rates, generally by the 25th year after issuance, thereby

creating an economic maturity date. The economic maturities

of our investments in perpetual debentures at December 31,

2006, were as follows in the table at the top of the next page: