TCF Bank 2015 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2015 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

|

|

61

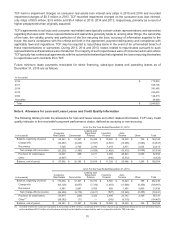

Loans and leases are charged off to the extent they are deemed to be uncollectible. Charge-offs related to losses are

utilized in the historical data in calculating the allowance for loan and lease losses. Consumer real estate loans are

charged off to the estimated fair value of underlying collateral, less estimated selling costs, no later than 150 days

past due. Additional review of the fair value, less estimated costs to sell, compared with the recorded value occurs

upon foreclosure and additional charge-offs are recorded if necessary. Commercial loans, leasing and equipment

finance loans and leases and inventory finance loans which are considered collateral dependent are charged off to

estimated fair value, less estimated selling costs when it becomes probable, based on current information and events,

that all principal and interest amounts will not be collectible in accordance with contractual terms. Auto loans will be

charged-off in full no later than 120 days past due, unless repossession is reasonably assured and in process, in

which case the loan would be charged-off to the fair value of the collateral, less estimated selling costs. Auto loans

in bankruptcy status may be partially charged-off to the fair value of the collateral prior to 120 days past due based

on specific criteria. Deposit account overdrafts are reported in other loans. Net losses on uncollectible overdrafts are

reported as net charge-offs in the allowance for loan and lease losses within 60 days from the date of overdraft. Loans

which are not collateral dependent are charged off when deemed uncollectible based on specific facts and

circumstances.

The amount of the allowance for loan and lease losses significantly depends upon management's estimates of variables

affecting valuation, appraisals of collateral, evaluations of performance and status and the amounts and timing of

future cash flows expected to be received. Such estimates, appraisals, evaluations and cash flows may be subject

to frequent adjustments due to changing economic prospects of borrowers, lessees or properties. These estimates

are reviewed periodically and adjustments, if necessary, are recorded in the provision for credit losses in the periods

in which they become known.

Lease Financing TCF provides various types of commercial lease financing that are classified for accounting purposes

as direct financing, sales-type or operating leases. Leases that transfer substantially all of the benefits and risks of

ownership to the lessee are classified as direct financing or sales-type leases and are included in loans and leases.

Direct financing and sales-type leases are carried at the combined present value of future minimum lease payments

and lease residual values. The determination of lease classification requires various judgments and estimates by

management including the fair value of the equipment at lease inception, useful life of the equipment under lease,

estimate of the lease residual value and collectability of minimum lease payments.

Sales-type leases generate dealer profit which is recognized at lease inception by recording lease revenue net of

lease cost. Lease revenue consists of the present value of the future minimum lease payments. Lease cost consists

of the leased equipment's book value, less the present value of its residual. Interest income on direct financing and

sales-type leases is recognized using methods which approximate a level yield over the fixed, non-cancelable term

of the lease. TCF receives pro rata rent payments for the interim period until the lease contract commences and the

fixed, non-cancelable lease term begins. TCF recognizes these interim payments in the month they are earned and

records the income in interest income on direct finance leases. Management has policies and procedures in place

for the determination of lease classification and review of the related judgments and estimates for all lease financings.

Some lease financings include a residual value component, which represents the estimated fair value of the leased

equipment at the expiration of the initial term of the transaction. The estimation of residual values involves judgment

regarding product and technology changes, customer behavior, shifts in supply and demand and other economic

assumptions. TCF reviews residual assumptions on the portfolio at least annually and downward adjustments, if

necessary, are charged to non-interest expense in the periods in which they become known.

TCF may sell minimum lease payments primarily as a credit risk reduction tool to third-party financial institutions at

fixed rates on a non-recourse basis with its underlying equipment as collateral. For those transactions which achieve

sale treatment, the related lease cash flow stream and the non-recourse financing are derecognized. For those

transactions which do not achieve sale treatment, the underlying lease remains on TCF's Consolidated Statements

of Financial Condition and non-recourse debt is recorded in the amount of the proceeds received. TCF retains servicing

of these leases and bills, collects and remits funds to the third-party financial institution. Upon default by the lessee,

the third-party financial institutions may take control of the underlying collateral which TCF would otherwise retain as

residual value.