TCF Bank 2015 Annual Report Download - page 2

Download and view the complete annual report

Please find page 2 of the 2015 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

|

|

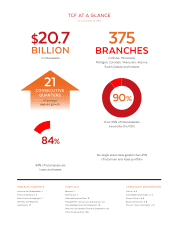

TCF AT A GLANCE

TABLE OF CONTENTS

Letter to Our Shareholders 1

Financial Summary 6

Select Financial Highlights 7

The New TCF Brand 8

Community 10

$20.7

BILLION

in total assets

375

BRANCHES

in Illinois, Minnesota,

Michigan, Colorado, Wisconsin, Arizona,

South Dakota and Indiana

84% of total assets are

loans and leases

FORM 10-K

Business 1

Risk Factors 7

Selected Financial Data 19

Management’s Discussion and Analysis 20

Consolidated Financial Statements 55

Notes to Consolidated Financial Statements 60

Other Financial Data 108

CORPORATE INFORMATION

Offices A-2

Stockholder Information A-3

Senior Officers A-6

Board of Directors A-8

Mission, Vision and Values A-9

21

CONSECUTIVE

QUARTERS

of average

deposit growth 90%

Over 90% of total deposits

insured by the FDIC

<25%

No single asset class greater than 25%

of total loan and lease portfolio

(As of December 31, 2015)

84%