TCF Bank 2015 Annual Report Download - page 4

Download and view the complete annual report

Please find page 4 of the 2015 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

|

|

their needs. During the year, we expanded our fleet of ATMs

by 28 percent through the addition of more than 200 ATMs

in Target® retail stores in Minnesota, Chicago and Michigan.

We introduced an entirely new website experience that

provides fingertip access to the information our customers

need the most. In addition, we introduced the latest mobile

payment solutions — Apple PayTM, Samsung PayTM and

Android PayTM — providing new and more secure ways to

pay for purchases. We also focused on enhancing our prod-

uct lineup to broaden our ability to support the financial

needs of our customers. We introduced a credit card and

made significant progress in supporting the introduction

of a suite of services to serve the needs of millennials and

those preferring nontraditional banking products. Our

customers have embraced these new product offerings and

the feedback we have received gives us confidence going

forward that we can gain a greater share of their wallet and

continue to grow our deposit funding base.

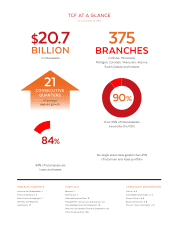

Our lending businesses had another strong year, with

originations of $15.3 billion, up 13.1 percent from 2014. This

marks our fourth consecutive year of double-digit loan

origination growth. Our diverse portfolio of loans and leases

finished the year at $17.4 billion, up 6.3 percent from 2014,

led by 38.3 percent growth in auto finance and 14.4 percent

growth in inventory finance. Our unique combination of

lending businesses gives us the ability to shift originations

in response to market conditions. We do not need to make

concessions on price or credit quality to obtain the growth

we want.

As our strong loan-origination engine delivered consistent

growth, we also continued to strengthen our ability to

generate incremental revenues through core loan sales and

securitizations. In 2015, we sold $2.7 billion of loans, primarily

composed of consumer auto loans and consumer real estate

loans, for a gain of $72.1 million. This included three auto

loan securitizations. Equally important, we continued to

service the loans we sold, which resulted in $31.2 million of

servicing fee income.

Anchored by a stable foundation of high quality loans in

diverse industries, our credit quality continued to stabilize in

2015. Following the sale of $405.9 million of consumer real

estate troubled debt restructuring loans in late 2014, non-

performing assets declined 11.3 percent in 2015. In addition,

net charge-offs as a percentage of average loans and leases

declined 19 basis points to 0.30 percent, a more normalized

level as we begin 2016. We have been vigilant in executing

our diversification strategy since the last recession. With new

economic concerns, such as China and the energy markets,

we believe we are now much better positioned for a potential

economic downturn.

The diversification of our revenue sources through loan

servicing and sales has made it possible to decrease our

reliance on banking fees to fuel our profitability. Banking fees

made up just 50 percent of non-interest income in 2015,

down from 77 percent in 2010. This change in revenue mix

has helped to reduce our exposure to increased regulatory

scrutiny of these fees through enforcement of Regulation E

and the Durbin Amendment as well as potential future

action by the Consumer Financial Protection Bureau on

industry-wide overdraft fee practices.

In December 2015, the Federal Reserve raised interest rates

for the first time since 2006. This was welcome news and

positions us well to increase shareholder value due to the ac-

tions we have taken over the past several years to make our

balance sheet more asset sensitive. We are more profitable

in a rising rate environment because 81 percent of our assets

are variable/adjustable rate or short/medium duration fixed

rate. As an asset-sensitive bank, we expect to benefit from

a rising rate environment; however, there are other factors

that can affect the margin, such as competition and portfolio

mix changes. As a result, we may see the benefit of a higher

interest rate environment in the form of higher net interest

income as opposed to a lift in the margin.

LOOKING AHEAD: CRAIG DAHL OUTLINES A

STRATEGIC VISION FOR 2016 AND BEYOND

Let me begin by saying that I’m honored and grateful to be

TCF’s new chief executive officer. I appreciate the support of

our chairman, Bill Cooper, and the entire board of directors

as we look to accelerate the momentum we have achieved

over the past several years. I am deeply committed to

continuing our focus on driving shareholder value. I believe

that we have significant opportunities to further scale our

businesses and create operating leverage that will achieve

consistent earnings growth. We believe we will be successful

by adhering to our conservative banking philosophy that has

made our company strong and focusing our organization

on a clear strategy. I am also fortunate to be surrounded by

a very talented team of senior executives who bring diverse

perspective, industry knowledge and a fundamental under-

standing of the unique cultural aspects of our company. Our

management team is poised to execute our strategy and

take full advantage of the marketplace opportunities that are

in front of us. I am optimistic about the journey ahead of us.

Nowhere is the future of our company more strongly on

display than in our new brand that was introduced last June.

I believe that presenting one message and image to the mar-

ket that connects all of the best elements of our businesses

together will strengthen our opportunities. For much of our

2