Foot Locker 2005 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2005 Foot Locker annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

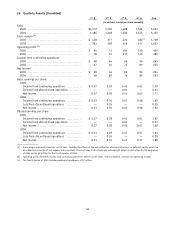

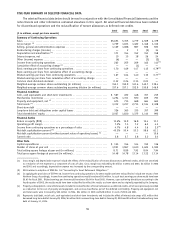

|

|

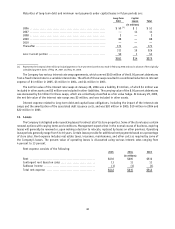

Foreign Currency Exchange Rates

The table below presents the fair value, notional amounts, and weighted-average exchange rates of foreign exchange

forward and option contracts outstanding at January 28, 2006.

Fair Value

(US in millions)

Contract Value

(US in millions)

Weighted-Average

Exchange Rate

Inventory

Buy e/Sell British £ ........................................ $— $ 34 0.6848

Buy British £/Sell e........................................ — (4) 0.6860

Buy $US/Sell e............................................. — (8) 1.2187

—22

Earnings

Buy e/Sell $US ............................................. $— $ 18 1.1500

—18

Intercompany

Buy e/Sell $US ............................................. $(1) $ 49 1.2173

Buy $US/Sell e............................................. — (18) 1.2394

Buy e/Sell British £ ........................................ — 21 0.6948

Buy British £/Sell e........................................ — (3) 0.6926

(1) 49

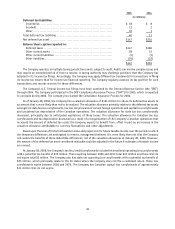

Interest Rate Risk Management

The Company has employed various interest rate swaps to minimize its exposure to interest rate fluctuations. These

swaps, which mature in 2022, have been designated as a fair value hedge of the changes in fair value of $100 million

of the Company’s 8.50 percent debentures payable in 2022 attributable to changes in interest rates and effectively convert

the interest rate on the debentures from 8.50 percent to a 1-month variable rate of LIBOR plus 3.45 percent.

The fair value of the swaps, included as an addition to other liabilities, was approximately $1 million at January 28, 2006,

and the fair value of the swaps, included as an addition to other assets was approximately $2 million at January 29, 2005.

The following table presents the Company’s outstanding interest rate derivatives:

2005 2004 2003

(in millions)

Interest Rate Swaps:

Fixed to Variable ($US) — notional amount ............. $ 100 $ 100 $ 100

Average pay rate ...................................... 8.00% 6.46% 5.07%

Average receive rate .................................. 8.50% 8.50% 8.50%

Variable to variable ($US) — notional amount ........... $ 100 $ 100 $ —

Average pay rate ...................................... 4.82% 2.73% —%

Average receive rate .................................. 4.79% 3.25% —%

Interest Rates

The Company’s major exposure to market risk is to changes in interest rates, primarily in the United States.

The table below presents the fair value of principal cash flows and related weighted-average interest rates by maturity

dates, including the effect of the interest rate swaps outstanding at January 28, 2006, of the Company’s long-term

debt obligations.

2006 2007 2008 2009 2010 Thereafter

Jan. 28,

2006

Total

Jan. 29,

2005

Total

($ in millions)

Long-term debt ..................... $ 50 — 2 88 — 190 $330 $368

Weighted-average interest rate ....... 7.3% 7.3% 7.3% 7.9% 8.2% 8.2%

Fair Value of Financial Instruments

The carrying value and estimated fair value of long-term debt was $311 million and $330 million, respectively, at

January 28, 2006 and $351 million and $368 million, respectively, at January 29, 2005. The carrying value and estimated

fair value of long-term investments and notes receivable was $33 million and $33 million, respectively, at January 28,

2006, and $32 million and $33 million, respectively, at January 29, 2005. The carrying values of cash and cash equivalents,

short-term investments and other current receivables and payables approximate their fair value.

47