Foot Locker 2005 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2005 Foot Locker annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

|

|

method, whereby compensation expense is recognized for all awards granted subsequent to the effective date of this

statement, as well as for the unvested portion of awards outstanding as of the effective date. The Company is currently

evaluating the impact SFAS No. 123(R), however, based upon preliminary analysis an additional $6–$8 million, or

$0.03–$0.05 per diluted share, of compensation expense will be recorded during the fiscal year ending February 3, 2007

as a result of this new accounting standard. This estimate is based upon many factors such as the market value and the

amount of share-based payments granted in future periods.

On October 18, 2005, the FASB issued FSP No. SFAS 123(R)-2, “Practical Accommodation to the Application of Grant

Date as Defined in FASB Statement No. 123(R),” to provide guidance on determining the grant date for an award as defined

in SFAS No. 123(R). This FSP stipulates that assuming all other criteria in the grant date definition are met, a mutual

understanding of the key terms and conditions of an award to an individual employee is presumed to exist upon the award’s

approval in accordance with the relevant corporate governance requirements, provided that the key terms and conditions

of an award (a) cannot be negotiated by the recipient with the employer because the award is a unilateral grant, and (b)

are expected to be communicated to an individual recipient within a relatively short time period from the date of approval.

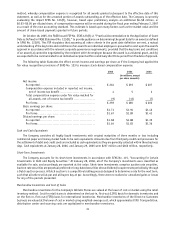

The following table illustrates the effect on net income and earnings per share as if the Company had applied the

fair value recognition provisions of SFAS No. 123 to measure stock-based compensation expense:

2005 2004 2003

(in millions, except

per share amounts)

Net income:

As reported............................................... $ 264 $ 293 $ 207

Compensation expense included in reported net income,

net of income tax benefit.............................. 4 5 2

Total compensation expense under fair value method for

all awards, net of income tax benefit .................. (9) (13) (7)

Pro forma ................................................ $ 259 $ 285 $ 202

Basic earnings per share:

As reported............................................... $1.71 $1.94 $1.46

Pro forma ................................................ $1.67 $1.89 $1.43

Diluted earnings per share:

As reported............................................... $1.68 $1.88 $1.39

Pro forma ................................................ $1.64 $1.83 $1.36

Cash and Cash Equivalents

The Company considers all highly liquid investments with original maturities of three months or less including

commercial paper and money market funds to be cash equivalents. Amounts due from third party credit card processors for

the settlement of debit and credit cards are included as cash equivalents as they are generally collected within three business

days. Cash equivalents at January 28, 2006, and January 29, 2005 were $237 million and $166 million, respectively.

Short-Term Investments

The Company accounts for its short-term investments in accordance with SFAS No. 115, “Accounting for Certain

Investments in Debt and Equity Securities.” At January 28, 2006, all of the Company’s investments were classified as

available for sale, and accordingly are reported at fair value. Short-term investments comprise auction rate securities.

Auction rate securities are perpetual preferred or long-dated securities whose dividend/coupon resets periodically through

a Dutch auction process. A Dutch auction is a competitive bidding process designed to determine a rate for the next term,

such that all sellers sell at par and all buyers buy at par. Accordingly, there were no realized or unrealized gains or losses

for any of the periods presented.

Merchandise Inventories and Cost of Sales

Merchandise inventories for the Company’s Athletic Stores are valued at the lower of cost or market using the retail

inventory method. Cost for retail stores is determined on the last-in, first-out (LIFO) basis for domestic inventories and

on the first-in, first-out (FIFO) basis for international inventories. Merchandise inventories of the Direct-to-Customers

business are valued at the lower of cost or market using weighted-average cost, which approximates FIFO. Transportation,

distribution center and sourcing costs are capitalized in merchandise inventories.

31