Chevron 2004 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2004 Chevron annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

|

|

CHEVRONTEXACO CORPORATION 2004 ANNUAL REPORT 69

NEW ACCOUNTING STANDARDS – Continued

introducedaprescriptiondrugbenefitunderMedicare,aswellas

afederalsubsidytosponsorsofretireehealthcareplansthatpro-

videabenefitthatisatleastactuariallyequivalenttoMedicare

PartD.InMay2004,theFASBissuedFSPFAS106-2.OneU.S.

subsidiarywasdeemedatleastactuariallyequivalentandeligible

forthefederalsubsidy.Theeffectonthecompany’spostretire-

mentbenefitobligationandtheassociatedannualexpensewas

deminimis.

FASBStatementNo.151,“InventoryCosts,anAmendmentofARB

No.43,Chapter4”(FAS151)InNovember2004,theFASBissued

FAS151whichiseffectiveforthecompanyonJanuary1,2006.

ThestandardamendstheguidanceinAccountingResearchBul-

letin(ARB)No.43,Chapter4,“InventoryPricing,”toclarifythe

accountingforabnormalamountsofidlefacilityexpense,freight,

handlingcostsandspoilage.Inaddition,thestandardrequiresthat

allocationoffixedproductionoverheadstothecostsofconversion

bebasedonthenormalcapacityoftheproductionfacilities.The

companyiscurrentlyevaluatingtheimpactofthisstandard.

FASBStatementNo.123R,“Share-BasedPayment”(FAS123R)

InDecember2004,theFASBissuedFAS123R,whichrequires

thatcompensationcostsrelatingtoshare-basedpaymentsbe

recognizedinthecompany’sfinancialstatements.Thecompany

currentlyaccountsforthosepaymentsundertherecognitionand

measurementprinciplesofAccountingPrinciplesBoard(APB)

OpinionNo.25,“AccountingforStockIssuedtoEmployees,”and

relatedinterpretations.Thecompanyispreparingtoimplement

thisstandardeffectiveJuly1,2005.Althoughthetransition

methodtobeusedtoadoptthestandardhasnotbeenselected,

theimpactofadoptionisexpectedtohaveaminimalimpact

onthecompany’sresultsofoperations,financialpositionand

liquidity.RefertoNote1,beginningonpage54,forthecompany’s

calculationoftheproformaimpactonnetincomeofFAS123,

whichwouldbesimilartothatunderFAS123R.

FASBStatementNo.153,“ExchangesofNonmonetaryAssets,–an

AmendmentofAPBOpinionNo.29”(FAS153)InDecember

2004,theFASBissuedFAS153,whichiseffectiveforthecom-

panyforasset-exchangetransactionsbeginningJuly1,2005.

UnderAPB29,assetsreceivedincertaintypesofnonmonetary

exchangeswerepermittedtoberecordedatthecarryingvalue

oftheassetsthatwereexchanged(i.e.,recordedonacarryover

basis).AsamendedbyFAS153,assetsreceivedinsomecircum-

stanceswillhavetoberecordedinsteadattheirfairvalues.Inthe

past,ChevronTexacohasnotengagedinalargenumberofnon-

monetaryassetexchangesforsignificantamounts.

RefertoNote1onpage54inthesection“Properties,Plantand

Equipment”foradiscussionofthecompany’saccountingpolicy

forthecostofexploratorywells.Thecompany’ssuspendedwells

arereviewedinthiscontextonaquarterlybasis.

TheSECissuedcommentlettersduring2004andinFebru-

ary2005toanumberofcompaniesintheoilandgasindustry

relatedtotheaccountingforsuspendedexploratorywells,partic-

ularlyforthosesuspendedundercertaincircumstancesformore

thanoneyear.InFebruary2005,theFASBissuedaproposedFSP

toamendFAS19,“FinancialAccountingandReportingbyOiland

GasProducingCompanies.”UndertheprovisionsofthedraftFSP,

exploratorywellcostswouldcontinuetobecapitalizedafterthe

completionofdrillingwhen(a)thewellhasfoundasufficient

quantityofreservestojustifycompletionasaproducingwell

and(b)theenterpriseismakingsufficientprogressassessing

thereservesandtheeconomicandoperatingviabilityofthe

project.Ifeitherconditionisnotmetorifanenterpriseobtains

informationthatraisessubstantialdoubtabouttheeconomicor

operationalviabilityoftheproject,theexploratorywellwouldbe

assumedtobeimpaired,anditscosts,netofanysalvagevalue,

wouldbechargedtoexpense.TheFSPprovidedanumberofindi-

catorsneedingtobepresenttodemonstratesufficientprogress

wasbeingmadeinassessingthereservesandeconomicviability

oftheproject.

Thecompanywillmonitorthecontinuingdeliberationsof

theFASBonthismatterandthepossibleimplications,ifany,to

thecompany’saccountingpolicyandtheamountscapitalized

forsuspended-wellcosts.Thedisclosuresanddiscussionbelow

addressthosesuggestedinthedraftFSPandintheadditional

guidanceissuedbytheSECinitsFebruary2005commentletter

tocompaniesintheoilandgasindustry.

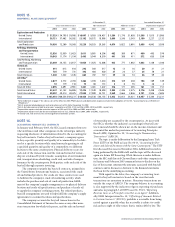

Thefollowingtableindicatesthechangestothecompany’s

suspendedexploratory-wellcostsforthethreeyearsended

December31,2004:

Year ended December 31

2003 2002

Beginning balance at January 1 $ 478 $ 655

Additions to capitalized exploratory

well costs pending the determination

of proved reserves 346 209

Reclassifications to wells, facilities

and equipment based on the

determination of proved reserves (145) (310)

Capitalized exploratory well costs

charged to expense (128) (46)

Other reductions* (2) (30)

Ending balance at December 31 $ 549 $ 478

* Represents a property sale in 2003 and a retirement due to a legal settlement in 2002.

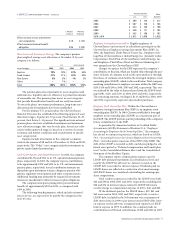

Thefollowingtableprovidesanagingofcapitalizedwellcosts,

basedonthedatethedrillingwascompleted,andthenumberof

projectsforwhichexploratorywellcostshavebeencapitalizedfora

periodgreaterthanoneyearsincethecompletionofdrilling:

Year ended December 31

2003 2002

Exploratory well costs capitalized

for a period of one year or less $ 181 $ 170

Exploratory well costs capitalized

for a period greater than one year 368 308

Balance at December 31 $ 549 $ 478

Number of projects with exploratory

well costs that have been capitalized

for a period greater than one year* 22 27

* Certain projects have multiple wells or fields or both.

Ofthe$671ofsuspendedcostsatDecember31,2004,

approximately$290relatedto30wellsinareasrequiringamajor

capitalexpenditurebeforeproductioncouldbeginandforwhich

additionaldrillingeffortswerenotunderwayorfirmlyplanned