Xerox 2005 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2005 Xerox annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

|

|

Xerox Corporation

75

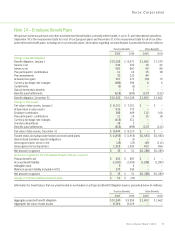

Plan Assets

Current Allocation and Investment Targets: As of the 2005 and 2004 measurement dates, the global pension plan assets were

$8.4 billion and $8.1 billion, respectively. These assets were invested among several asset classes. The amount and percentage of

assets invested in each asset class as of each of these dates is shown below:

Percentage of

Asset Value Total Assets

(in millions) 2005 2004 2005 2004

Asset Category

Equity securities(1) $ 4,830 $ 4,753 57% 58%

Debt securities(1) 2,723 2,592 32 32

Real estate 504 464 6 6

Other 387 301 5 4

Total $8,444 $8,110 100% 100%

(1) None of the investments includes debt or equity securities of Xerox Corporation.

Xerox Annual Report 2005

Investment Strategy: The target asset allocations for our

worldwide plans for 2005 were 54% invested in equities, 39%

invested in fixed income, 6% invested in real estate and 1%

invested in Other. The target asset allocations for our worldwide

plans for 2004 were 59% invested in equities, 34% invested in

fixed income, 6% invested in real estate and 1% invested in Other.

The pension assets outside of the U.S. as of the 2005 and 2004

measurement dates were $4.3 billion and $4.1 billion, respectively.

The target asset allocations for the U.S. pension plan include

64% invested in equities, 30% in fixed income, 5% in real estate

and 1% in other investments. Cash investments are sufficient

to handle expected cash requirements for benefit payments

and will vary throughout the year.The expected long-term rate

of return on the U.S. pension assets is 8.75%.

We employ a total return investment approach whereby a mix

of equities and fixed-income investments are used to maximize

the long-term return of plan assets for a prudent level of risk.

The intent of this strategy is to minimize plan expenses by

exceeding the interest growth in long-term plan liabilities. Risk

tolerance is established through careful consideration of plan

liabilities, plan funded status, and corporate financial condition.

This consideration involves the use of long-term measures that

address both return and risk. The investment portfolio contains

adiversified blend of equity and fixed-income investments.

Furthermore, equity investments are diversified across U.S and

non-U.S. stocks as well as growth, value, and small and large

capitalizations. Other assets such as real estate, private equity

and hedge funds are used to improve portfolio diversification.

Derivatives may be used to hedge market exposurein an efficient

and timely manner; however,derivatives may not be used to

leverage the portfolio beyond the market value of the underlying

investments. Investment risks and returns aremeasured and

monitored on an ongoing basis through annual liability

measurements and quarterly investment portfolio reviews.

Expected Long-Term Rate of Return: We employ a “building block”

approach in determining the long-term rate of return for plan assets.

Historical markets are studied and long-term relationships between

equities and fixed income areassessed. Current market factors

such as inflation and interest rates are evaluated before long-term

capital market assumptions are determined. The long-term portfolio

return is established giving consideration to investment diversifica-

tion and rebalancing. Peer data and historical returns are reviewed

periodically to assess reasonableness and appropriateness.

Contributions: We expect to contribute $106 to our worldwide

pension plans and $130 to our other post-retirement benefit plans

in 2006. The 2006 expected pension plan contributions do not

include any planned contribution for the domestic tax-qualified

plans because thereare no required contributions to these plans

for the 2006 fiscal year. However, once the January 1, 2006

actuarial valuations and projected results as of the end of the

2006 measurement year are available, the desirability of addi-

tional contributions will be assessed. Based on these results,

we may voluntarily decide to contribute to these plans, even

though no contribution is required. In prior years, after making

this assessment, we decided to contribute $230 and $210 in

April 2005 and April 2004, respectively,to our domestic tax-

qualified plans in order to make them 100% funded on a current

liability basis under the ERISA funding rules.

Estimated FutureBenefit Payments: The following benefit

payments, which reflect expected futureservice, as appropriate,

are expected to be paid (in millions):

Pension Benefits Other Benefits

2006 $ 731 $ 130

2007 580 133

2008 531 135

2009 591 134

2010 667 129

Years 2011-2015 3,437 640