Xerox 2005 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2005 Xerox annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

|

|

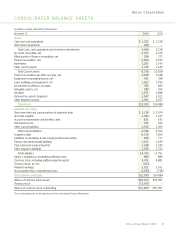

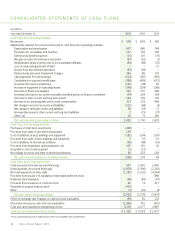

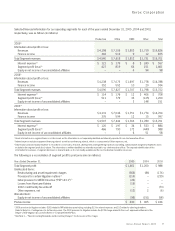

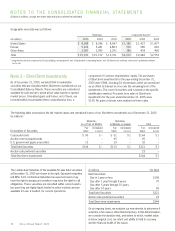

Xerox Corporation

51

Changes in Estimates: In the ordinary course of accounting

for items discussed above, we make changes in estimates

as appropriate, and as we become aware of circumstances

surrounding those estimates. Such changes and refinements

in estimation methodologies are reflected in reported results

of operations in the period in which the changes are made

and, if material, their effects are disclosed in the Notes to the

Consolidated Financial Statements.

New Accounting Standards and Accounting Changes:

During the two years ended December 31, 2005, the Financial

Accounting Standards Board (“FASB”) issued several pronounce-

ments of significance to the Company which are discussed in

detail below. In addition, the FASB issued several other pronounce-

ments, including standards on inventory (SFAS No. 151 “Inventory

Costs, an amendment of ARB 43, Chapter 4”), exchanges of

nonmonetary assets (SFAS No. 153 “Exchanges of Nonmonetary

Assets”) and accounting changes (SFAS No. 154 “Accounting

Changes and Error Corrections”), which we either currently

comply with or arenot anticipating to have a significant impact

on our future financial condition or results of operations.

In June 2005, the FASB issued Staff Position No. FAS 143-1,

“Accounting for Electronic Equipment Waste Obligations”

(“FSP 143-1”), which provided guidance on the accounting for

obligations associated with the European Union (“EU”) Directive

on Waste Electrical and Electronic Equipment (the “WEEE

Directive”). FSP 143-1 provided guidance on how to account for

the effects of the WEEE Directive with respect to historical waste

and waste associated with products on the market on or before

August 13, 2005. As of December 31, 2005, the WEEE Directive

had been adopted into law by the EU member countries in which

we have significant operations, with the exception of the United

Kingdom. Accordingly, in 2005, we recorded an initial after-tax

charge of $18 ($26 pre-tax) in Other expenses, net in the

accompanying Consolidated Statement of Income representing

the disposal obligation primarily related to our leased equipment

population in service as of the date the EU member countries

adopted the WEEE Directive. The adoption of the WEEE Directive

by an EU member country created a legal disposal obligation

and accordingly we are now required to accrue the cost of that

obligation at the time the equipment is placed in service. We will

be required to record a similar charge for the United Kingdom

when it adopts the WEEE Directive, which is expected to be no

more than $10. The ongoing quarterly expense resulting from

compliance with the WEEE Directive associated with our leased

equipment will generally be charged to cost of sales when

equipment is placed in service and is not expected to have a

material effect on our financial condition or results of operations.

In March 2005, the FASB issued Interpretation No. 47, “Accounting

for Conditional Asset Retirement Obligations – an interpretation

of FASB Statement No. 143” (“FIN 47”). FIN 47 requires an entity

to recognize a liability for the fair value of a conditional asset

retirement obligation if the fair value can be reasonably estimated.

Aconditional asset retirement obligation is a legal obligation to

perform an asset retirement activity in which the timing or method

of settlement are conditional upon a future event that may or

may not be within control of the entity. The adoption of FIN 47 in

2005 resulted in an after-tax charge of $8 ($12 pre-tax) and was

recorded as a cumulative effect of change in accounting principle.

This charge represents conditional asset retirement obligations

associated with leased facilities where we are required to remove

certain leasehold improvements and restore the facility to its

original condition at lease termination. Previously, we recorded

costs associated with this obligation upon lease termination when

the costs were known. On a prospective basis, this accounting

change requires recognition of these costs ratably over the lease

term. We believe that the adoption of this interpretation will not

have a material effect on our financial condition or results of oper-

ations. The pro forma effect of applying this guidance in all prior

periods presented, as well as the effect on our Consolidated

Balance Sheet, was not material.

Stock-Based Compensation: In December 2004, the FASB issued

Statement of Financial Accounting Standards No. 123(R), “Share-

Based Payment” (“FAS 123(R)”), an amendment of FAS No. 123,

“Accounting for Stock-Based Compensation,” which requires com-

panies to recognize compensation expense using a fair-value-based

method for costs related to share-based payments, including stock

options. As permitted by the SEC, the requirements of FAS 123(R)

areeffective for our fiscal year beginning January 1, 2006. Upon

adoption, we will elect to apply the modified prospective transition

method and therefore we will not restate the results of prior periods.

During May 2005, we approved the accelerated vesting of approx-

imately 3.6 million unvested employee stock options granted in

2004, that would have been scheduled to vest January 1, 2007, to

December 31, 2005. These accelerated options had a weighted

average exercise price of $13.71 as of the accelerated vesting date.

The primary purpose of this accelerated vesting was to eliminate

compensation expense we would recognize in our results of

operations upon the adoption of FAS 123(R). The acceleration is

expected to reduce our pre-tax stock option compensation expense

in 2006 that otherwise would have been recognized by approxi-

mately $31 or $0.02 per diluted share and, accordingly, increase

our 2005 pro forma expense disclosed below. After the effects

of the accelerated vesting, the implementation of FAS 123(R) is

expected to be immaterial. In addition, in 2005 in lieu of stock

options, we began granting time- and performance-based restricted

stock awards, which are already reflected as compensation expense

in our results of operations. Therefore, the acceleration of vesting

for substantially all previously awarded stock options effectively

completes the transition to the new stock-based award program.

Xerox Annual Report 2005