Xerox 2005 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2005 Xerox annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

|

|

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

(Dollars in millions, except per-share data and unless otherwise indicated)

68

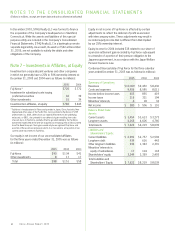

Credit Facility: In June 2003, we entered into the 2003 Credit

Facility. The 2003 Credit Facility consists of a fully drawn $300

term loan and a $700 revolving credit facility that includes a $200

letter of credit sub-facility. This facility expires on September 30,

2008. As of December 31, 2005, the $300 term loan and $15 of

letters of credit were outstanding and there were no outstanding

borrowings under the revolving credit facility. Since inception

of the 2003 Credit Facility in June 2003, there have been no

borrowings under the revolving credit facility. Xerox is the only

borrower of the term loan.

Subject to certain limits described in the following paragraph,

the obligations under the 2003 Credit Facility are secured by liens

on substantially all the assets of Xerox and each of our U.S. sub-

sidiaries that have a consolidated net worth from time to time of

$100 or more (the “Material Subsidiaries”), excluding Xerox Credit

Corporation (“XCC”) and certain other finance subsidiaries, and

areguaranteed by certain Material Subsidiaries. At December 31,

2005, Xerox is the only borrower under the 2003 Credit Facility.

Under the terms of certain of our outstanding public bond

indentures, the amount of obligations under the 2003 Credit

Facility that can be (1) secured by assets (the “Restricted Assets”)

of (a) Xerox and (b) our non-financing subsidiaries that have a

consolidated net worth of at least $100, without (2) triggering a

requirement to also secure those indentures, is limited to the

excess of (x) 20% of our consolidated net worth (as defined in the

public bond indentures) over (y) the outstanding amount of certain

other debt that is secured by the Restricted Assets. Accordingly,

the amount of 2003 Credit Facility debt secured by the Restricted

Assets will vary from time to time with changes in our consolidated

net worth. The amount of security provided under this formula

accrues ratably to the benefit of both the term loan and revolving

loans under the 2003 Credit Facility.

The term loan and the revolving loans bear interest at LIBOR plus

aspread that varies between 1.75% and 3.00% or, at our election,

at a base rate plus a spread that depends on the then-current

Leverage Ratio, as defined, in the 2003 Credit Facility. The

interest rate on the debt as of December 31, 2005 was 6.22%.

The 2003 Credit Facility contains affirmative and negative covenants

as well as financial maintenance covenants. Subject to certain

exceptions, we cannot pay cash dividends on our common stock

during the facility term, although we can pay cash dividends on

our preferred stock, provided there is then no event of default.

Among defaults customary for facilities of this type, defaults on

our other debt, bankruptcy of certain of our legal entities, or a

change in control of Xerox Corporation, would all constitute

events of default. At December 31, 2005, we werein compliance

with the covenants of the 2003 Credit Facility and we expect

to remain in compliance for at least the next twelve months.

The Senior Notes also contain negative covenants (but no financial

maintenance covenants) similar to those contained in the 2003

Credit Facility. However, they generally provide us with more flexi-

bility than the 2003 Credit Facility covenants, except that payment

of cash dividends on the Series C Mandatory Convertible Preferred

Stock is subject to the conditions that there is then no default

under the Senior Notes, that the fixed-charge coverage ratio (as

defined) is greater than 2.25 to 1.00, and that the amount of the

cash dividend does not exceed the then amount available under

the restricted payments basket (as defined). The Senior Notes are

guaranteed by our wholly owned subsidiary Xerox International

Joint Marketing, Inc.

Debt Repayments and Maturities: During 2005, we repaid

$140 of public unsecured debt prior to its scheduled maturity

in addition to $1,020 in scheduled public debt maturities.

Guarantees: At December 31, 2005, we have guaranteed $17

of indebtedness of our foreign subsidiaries. This debt is included

in our Consolidated Balance Sheet as of such date. In addition, as

of December 31, 2005, $32 of letters of credit have been issued

in connection with insurance guarantees.

Interest: Interest paid on our short-term debt, long-term debt and

liabilities to subsidiary trusts issuing preferred securities amounted

to $555, $710 and $867 for the years ended December 31,

2005, 2004 and 2003, respectively.

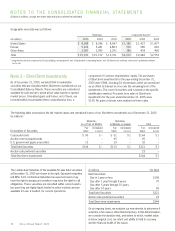

Interest expense and interest income for the three years ended

December 31, 2005 was as follows (in millions):

Years Ended December 31, 2005 2004 2003

Interest expense(1) $ 557 $ 708 $ 884

Interest income(2) (1,013) (1,009) (1,062)

(1) Includes Equipment financing interest expense, as well as non-financing interest

expense included in Other expenses, net in the Consolidated Statements of

Income.

(2) Includes Finance income, as well as other interest income that is included in

Other expenses, net in the Consolidated Statements of Income.

Equipment financing interest is determined based on an

estimated cost of funds applied against an estimated level

of debt required to support our financed receivables. The

estimated cost of funds is primarily based on our secured

borrowing rates. The estimated level of debt is based on an

assumed 7 to 1 leverage ratio of debt/equity as compared

to our average finance receivables. This methodology has

been consistently applied for all periods presented.

Xerox Annual Report 2005