Xcel Energy 2011 Annual Report Download - page 120

Download and view the complete annual report

Please find page 120 of the 2011 Xcel Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

|

|

110

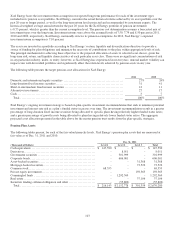

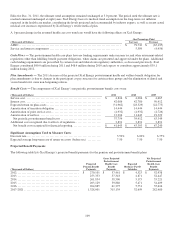

Multiemployer Plans

NSP-Minnesota and NSP-Wisconsin each contribute to several union multiemployer pension and other postretirement benefit

plans, none of which are individually significant. These plans provide pension and postretirement health care benefits to certain

union employees, including electrical workers, boilermakers, and other construction and facilities workers who may perform

services for more than one employer during a given period and do not participate in the NSP-Minnesota and NSP-Wisconsin

sponsored pension and postretirement health care plans. Contributing to these types of plans creates risk that differs from

providing benefits under NSP-Minnesota and NSP-Wisconsin sponsored plans, in that if another participating employer ceases to

contribute to a multiemployer plan, additional unfunded obligations may need to be funded over time by remaining participating

employers.

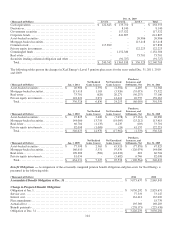

Contributions to multiemployer plans were as follows for the years ended Dec. 31, 2011, 2010 and 2009. There were no

significant changes to the nature or magnitude of the participation of NSP-Minnesota and NSP-Wisconsin in multiemployer plans

for the years presented:

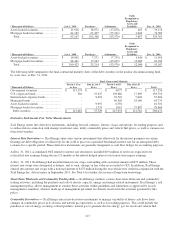

(Thousands of Dollars) 2011 2010 2009

Multiemployer pension contributions:

NSP-Minnesota ...................................................... $

17,811 $

13,461 $

11,348

NSP-Wisconsin ...................................................... 169 170 116

Total .............................................................. $

17,980 $

13,631 $

11,464

Multiemployer other postretirement benefit contributions:

NSP-Minnesota ...................................................... $

336 $

153 $

140

Total .............................................................. $

336 $

153 $

140

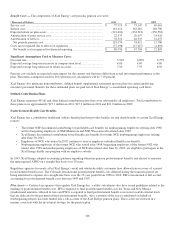

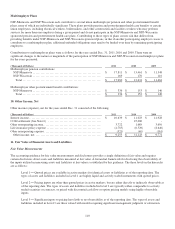

10. Other Income, Net

Other income (expense), net for the years ended Dec. 31 consisted of the following:

(Thousands of Dollars) 2011 2010 2009

Interest income ......................................................... $

10,639 $

11,023 $

14,928

COLI settlement (See Note 6) .......................................... - 25,000 -

Other nonoperating income.............................................. 3,722 1,689 3,650

Life insurance policy expense ........................................... (4,785) (6,529) (8,646)

Other nonoperating expense ............................................. (321) (40) (161)

Other income, net..................................................... $

9,255 $

31,143 $

9,771

11. Fair Value of Financial Assets and Liabilities

Fair Value Measurements

The accounting guidance for fair value measurements and disclosures provides a single definition of fair value and requires

certain disclosures about assets and liabilities measured at fair value. A hierarchal framework for disclosing the observability of

the inputs utilized in measuring assets and liabilities at fair value is established by this guidance. The three levels in the hierarchy

are as follows:

Level 1 — Quoted prices are available in active markets for identical assets or liabilities as of the reporting date. The

types of assets and liabilities included in Level 1 are highly liquid and actively traded instruments with quoted prices.

Level 2 — Pricing inputs are other than quoted prices in active markets, but are either directly or indirectly observable as

of the reporting date. The types of assets and liabilities included in Level 2 are typically either comparable to actively

traded securities or contracts, or priced with discounted cash flow or option pricing models using highly observable

inputs.

Level 3 — Significant inputs to pricing have little or no observability as of the reporting date. The types of assets and

liabilities included in Level 3 are those valued with models requiring significant management judgment or estimation.