Xcel Energy 2011 Annual Report Download - page 113

Download and view the complete annual report

Please find page 113 of the 2011 Xcel Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

|

|

103

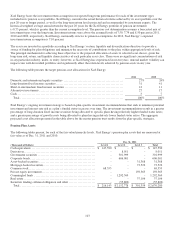

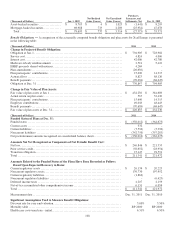

Xcel Energy bases the investment-return assumption on expected long-term performance for each of the investment types

included in its pension asset portfolio. Xcel Energy considers the actual historical returns achieved by its asset portfolio over the

past 20-year or longer period, as well as the long-term return levels projected and recommended by investment experts. The

historical weighted average annual return for the past 20 years for the Xcel Energy portfolio of pension investments

is 8.73 percent, which is greater than the current assumption level. The pension cost determination assumes a forecasted mix of

investment types over the long term. Investment returns were above the assumed levels of 7.50, 7.79 and 8.50 percent in 2011,

2010 and 2009, respectively. Xcel Energy continually reviews its pension assumptions. In 2012, Xcel Energy’s expected

investment return assumption is 7.10 percent.

The assets are invested in a portfolio according to Xcel Energy’s return, liquidity and diversification objectives to provide a

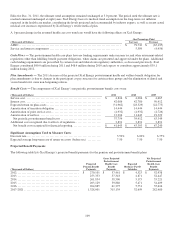

source of funding for plan obligations and minimize the necessity of contributions to the plan, within appropriate levels of risk.

The principal mechanism for achieving these objectives is the projected allocation of assets to selected asset classes, given the

long-term risk, return, and liquidity characteristics of each particular asset class. There were no significant concentrations of risk

in any particular industry, index, or entity; however, as Xcel Energy has experienced in recent years, unusual market volatility can

impact even well-diversified portfolios and significantly affect the return levels achieved by pension assets in any year.

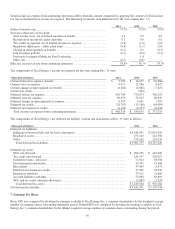

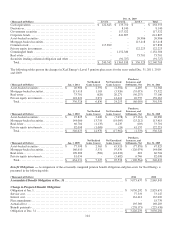

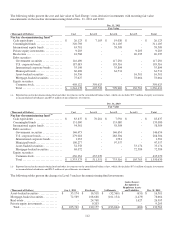

The following table presents the target pension asset allocations for Xcel Energy:

2011 2010

Domestic and international equity securities ................................

...............

27%

24

%

Long-duration fixed income securities ................................

.....................

31 41

Short-to-intermediate fixed income securities ................................

..............

12 11

Alternative investments ................................................................

..

27 17

Cash................................................................

....................

3 7

Total ................................................................

.................

100%

100

%

Xcel Energy’s ongoing investment strategy is based on plan-specific investment recommendations that seek to minimize potential

investment and interest rate risk as a plan’s funded status increases over time. The investment recommendations result in a greater

percentage of long-duration fixed income securities being allocated to specific plans having relatively higher funded status ratios,

and a greater percentage of growth assets being allocated to plans having relatively lower funded status ratios. The aggregate

projected asset allocation presented in the table above for the master pension trust results from the plan-specific strategies.

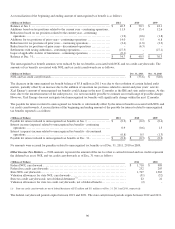

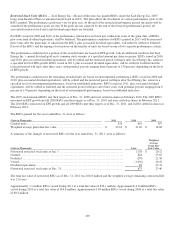

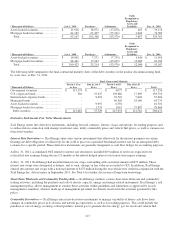

Pension Plan Assets

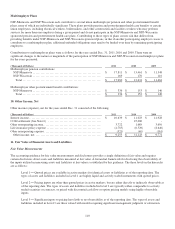

The following tables present, for each of the fair value hierarchy levels, Xcel Energy’s pension plan assets that are measured at

fair value as of Dec. 31, 2011 and 2010:

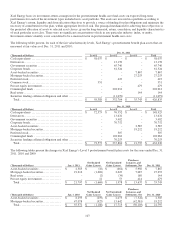

Dec. 31, 2011

(Thousands of Dollars) Level 1 Level 2 Level 3 Total

Cash equivalents ................................

..................

$

147,590 $

- $

- $

147,590

Derivatives................................

........................

- 8,011 - 8,011

Government securities ................................

.............

- 301,999 - 301,999

Corporate bonds................................

...................

- 606,001 - 606,001

Asset-backed securities ................................

............

- - 31,368 31,368

Mortgage-backed securities................................

.........

- - 73,522 73,522

Common stock ................................

....................

68,553 - - 68,553

Private equity investments................................

..........

- - 159,363 159,363

Commingled funds ................................

................

- 1,292,569 - 1,292,569

Real estate ................................

........................

- - 37,106 37,106

Securities lending collateral obligation and other

.....................

- (55,802) - (55,802)

Total ................................

...........................

$

216,143 $

2,152,778 $

301,359 $

2,670,280