Xcel Energy 2011 Annual Report Download - page 105

Download and view the complete annual report

Please find page 105 of the 2011 Xcel Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

|

|

95

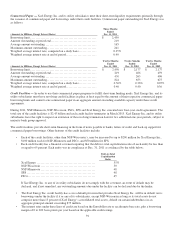

6. Income Taxes

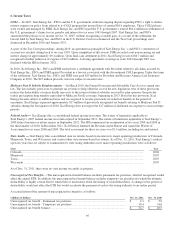

COLI — In 2007, Xcel Energy Inc., PSCo and the U.S. government settled an ongoing dispute regarding PSCo’s right to deduct

interest expense on policy loans related to its COLI program that insured lives of certain PSCo employees. These COLI policies

were owned and managed by PSRI. Xcel Energy Inc. and PSCo paid the U.S. government a total of $64.4 million in settlement of

the U.S. government’s claims for tax, penalty and interest for tax years 1993 through 2007. Xcel Energy Inc. and PSCo

surrendered the policies to its insurer on Oct. 31, 2007, without recognizing a taxable gain. As a result of the settlement, the

lawsuit filed by Xcel Energy Inc. and PSCo in the U.S. District Court was dismissed and the Tax Court proceedings were

dismissed in December 2010 and January 2011.

As part of the Tax Court proceedings, during 2010, an agreement in principle of Xcel Energy Inc.’s and PSCo’s statements of

account was reached, dating back to tax year 1993. Upon completion of this review, PSRI recorded a net non-recurring tax and

interest charge of approximately $9.4 million. Upon final cash settlement in 2011, Xcel Energy received $0.7 million and

recognized a further reduction of expense of $0.3 million. A closing agreement covering tax years 2003 through 2007 was

finalized with the IRS in January 2012.

In 2010, Xcel Energy Inc., PSCo and PSRI entered into a settlement agreement with Provident related to all claims asserted by

Xcel Energy Inc., PSCo and PSRI against Provident in a lawsuit associated with the discontinued COLI program. Under the terms

of the settlement, Xcel Energy Inc., PSCo and PSRI were paid $25 million by Provident and Reassure America Life Insurance

Company in 2010. The $25 million proceeds were not subject to income taxes.

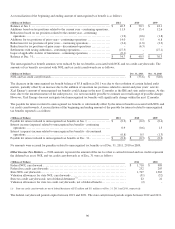

Medicare Part D Subsidy Reimbursements — In March 2010, the Patient Protection and Affordable Care Act was signed into

law. The law includes provisions to generate tax revenue to help offset the cost of the new legislation. One of these provisions

reduces the deductibility of retiree health care costs to the extent of federal subsidies received by plan sponsors that provide

retiree prescription drug benefits equivalent to Medicare Part D coverage, beginning in 2013. Based on this provision, Xcel

Energy became subject to additional taxes and was required to reverse previously recorded tax benefits in the period of

enactment. Xcel Energy expensed approximately $17 million of previously recognized tax benefits relating to Medicare Part D

subsidies during the first quarter of 2010. Xcel Energy does not expect the $17 million of additional tax expense to recur in future

periods.

Federal Audit — Xcel Energy files a consolidated federal income tax return. The statute of limitations applicable to

Xcel Energy’s 2007 federal income tax return expired in September 2011. The statute of limitations applicable to Xcel Energy’s

2008 federal income tax return expires in September 2012. The IRS commenced an examination of tax years 2008 and 2009 in

the third quarter of 2010. In December 2011, Xcel Energy finalized the Revenue Agent Report and signed the Waiver of

Assessment for tax years 2008 and 2009. The total assessment for these tax years was $1.4 million, including tax and interest.

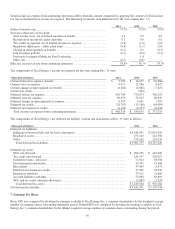

State Audits — Xcel Energy files consolidated state tax returns based on income in its major operating jurisdictions of Colorado,

Minnesota, Texas, and Wisconsin, and various other state income-based tax returns. As of Dec. 31, 2011, Xcel Energy’s earliest

open tax years that are subject to examination by state taxing authorities in its major operating jurisdictions were as follows:

State Year

Colorado................................................................

................................

2006

Minnesota ................................................................

...............................

2007

Texas................................................................................................

....

2007

Wisconsin ................................................................

...............................

2007

As of Dec. 31, 2011, there were no state income tax audits in progress.

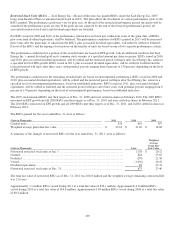

Unrecognized Tax Benefits —The unrecognized tax benefit balance includes permanent tax positions, which if recognized would

affect the annual ETR. In addition, the unrecognized tax benefit balance includes temporary tax positions for which the ultimate

deductibility is highly certain but for which there is uncertainty about the timing of such deductibility. A change in the period of

deductibility would not affect the ETR but would accelerate the payment of cash to the taxing authority to an earlier period.

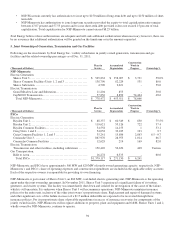

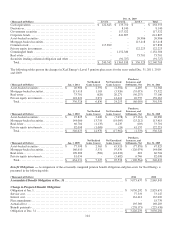

A reconciliation of the amount of unrecognized tax benefit is as follows:

(Millions of Dollars) Dec. 31, 2011

Dec. 31, 2010

Unrecognized tax benefit - Permanent tax positions................................

...........

$

4.3 $

5.9

Unrecognized tax benefit - Temporary tax positions ................................

..........

30.4 34.6

Unrecognized tax benefit balance ................................

...........................

$

34.7 $

40.5