Travelers 2007 Annual Report Download - page 94

Download and view the complete annual report

Please find page 94 of the 2007 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

|

|

National Accounts. Net written premiums of $1.06 billion in 2007 declined 7% from 2006,

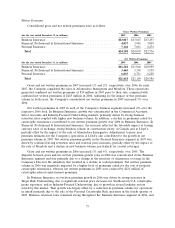

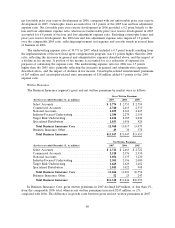

primarily reflecting competitive market conditions that resulted in lower business volume. Net written

premiums in 2006 declined by $95 million, or 8%, from 2005, primarily reflecting a reduction in

premiums related to favorable loss experience on business priced on a loss-sensitive basis and lower

new business volume, partially offset by the decline in ceded premiums at Discover Re due to a change

in the structure of reinsurance coverage.

Industry-Focused Underwriting. Net written premiums of $2.30 billion in 2007 increased 5% over

2006. The increase was driven by the Construction business unit, where favorable economic conditions

contributed to higher new business volume; the Oil & Gas business unit, due to increased business

retention rates and continued strong renewal price changes; and the Public Sector unit, due to an

increase in retention rates. In addition, continued strong new business volume and business retention

rates in the Agribusiness business unit contributed to premium growth in 2007. Net written premiums

in the Technology business unit in 2007 were level with 2006. Net written premiums of $2.20 billion in

2006 increased by 6% over 2005, driven by growth in the Construction and Oil & Gas business units.

Favorable economic conditions in these industry sectors, significant increases in business retention rates

and continued strong new business volume contributed to the increase in premium volume in 2006 in

these two business units. The remaining three business units in this market—Technology, Agribusiness

and Public Sector—all achieved lesser degrees of net written premium growth over 2005.

Target Risk Underwriting. Net written premiums of $1.67 billion in 2007 grew 2% over 2006,

driven by increases in the Inland Marine and National Property business units. Strong growth in new

business volume accounted for the increase in Inland Marine net written premium volume, whereas

National Property’s premium volume growth was driven by continued strong business retention rates

and a decline in premiums ceded for catastrophe reinsurance coverage, partially offset by a decrease in

renewal price changes, which were negative. Growth in these two business units was partially offset by a

decline in Excess Casualty net written premiums. Net written premiums of $1.63 billion in 2006

increased by 10% over 2005, driven by strong growth in the National Property and Inland Marine

business units. Significant renewal price increases, particularly for Southeastern U.S. catastrophe-prone

exposures, and strong business retention rates were the primary factors accounting for net written

premium growth in these two business units in 2006. The Ocean Marine business unit also contributed

to net written premium growth in 2006, primarily due to a decrease in the amount of business ceded.

Specialized Distribution. Net written premiums of $1.02 billion in 2007 declined less than 1% from

2006. The decline was primarily due to premium reductions in the National Programs business unit,

driven by reductions in new business volume and business retention rates due to competitive market

conditions. These reductions were largely offset by premium growth in the Northland business unit due

to strong business retention rates and new business volume. Net written premium volume in 2006 of

$1.02 billion increased 13% over 2005, primarily driven by the transfer of certain national small

business insurance programs from Select Accounts to the National Programs business unit. In addition,

Northland also experienced premium growth in 2006, primarily resulting from higher business retention

rates and new business volume in commercial trucking, its primary line of business.

In Business Insurance Other, the decline in 2007 and 2006 net premium volume compared with

2005 reflected the impact of business in runoff and the sale of the Company’s Personal Catastrophe

Risk operation in November 2005. The runoff healthcare, reinsurance and international business

acquired in the merger produced minimal written premium volume in 2007, 2006 and 2005.

82