Travelers 2007 Annual Report Download - page 90

Download and view the complete annual report

Please find page 90 of the 2007 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

|

|

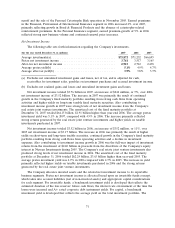

$111 million of earned premiums in 2005. Earned premiums in 2005 were reduced by $67 million of

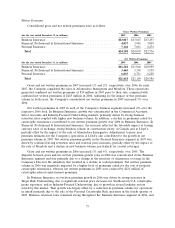

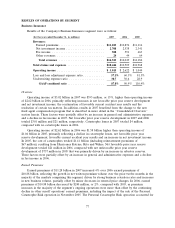

reinstatement premiums related to catastrophe losses.

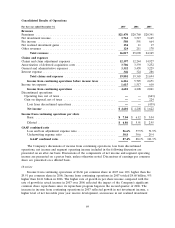

Net Investment Income

Refer to the ‘‘Net Investment Income’’ section of the ‘‘Consolidated Results of Operations’’

discussion herein for a description of the factors contributing to the increase in the Company’s net

investment income in 2007 and 2006.

Fee Income

National Accounts is the primary source of fee income due to its service businesses, which include

claim and loss prevention services to large companies that choose to self-insure a portion of their

insurance risks, and claims and policy management services to workers’ compensation residual market

pools. The $83 million and $72 million declines in fee income in 2007 and 2006, respectively, primarily

resulted from lower serviced premium volume due to the depopulation of workers’ compensation

residual market pools, the impact of lower loss costs on fee income due to workers’ compensation

reforms, primarily in California, and lower new business volume due to increased competition.

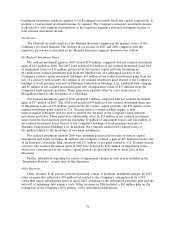

Claims and Expenses

Claims and claim adjustment expenses in 2007 of $6.67 billion declined by $180 million, or 3%,

from the 2006 total of $6.85 billion, primarily reflecting an increase in net favorable prior year reserve

development and continued favorable current accident year results, partially offset by an increase in

business volume.

Net favorable prior year reserve development totaled $301 million in 2007, compared with

$21 million in 2006. The 2007 total was primarily driven by better than expected loss development for

recent accident years in the commercial multi-peril, general liability, commercial automobile and

property product lines. The commercial multi-peril and general liability product lines experienced better

than anticipated loss development that was attributable to several factors, including improved legal and

judicial environments, as well as enhanced risk control, underwriting and claim process initiatives. The

commercial automobile product line experienced better than expected loss development due to more

favorable legal and judicial environments, claim handling initiatives focused on the automobile line of

insurance and improvements in auto safety technology. The property product line experienced fewer

than expected late reported claims related to non-catastrophe weather events that occurred late in

2006, as well as better than expected frequency and severity due in part to changes in the marketplace,

such as higher deductibles and lower policy limits. In addition, the property product line experienced

better than expected large loss outcomes which were partially attributable to favorable litigation

resolutions. Net total prior year reserve development in 2007 included a $185 million increase to

environmental reserves. The Company’s completion of its annual in-depth asbestos claim review in the

third quarter of 2007 and its quarterly asbestos reserve reviews throughout the year resulted in no

change to the Company’s asbestos reserves in 2007. (Refer to the ‘‘Asbestos Claims and Litigation’’ and

‘‘Environmental Claims and Litigation’’ sections herein for additional discussion.)

In 2006, net favorable prior year reserve development in the commercial multi-peril, general

liability, property and commercial automobile lines of business was largely offset by increases totaling

$275 million to asbestos and environmental reserves and reserve strengthening for assumed reinsurance

business in runoff. The commercial multi-peril and liability lines of business experienced better than

anticipated loss development in 2006 that was attributable to several factors, including improving legal

and judicial environments, as well as enhanced risk control, underwriting and claim process initiatives.

The favorable prior year reserve development in 2006 in the property line of business primarily

reflected less ‘‘demand surge’’ inflation than originally estimated for 2005 accident year non-catastrophe

78