Travelers 2007 Annual Report Download - page 133

Download and view the complete annual report

Please find page 133 of the 2007 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

|

|

The effect of a particular risk factor on estimates of claim liabilities cannot be isolated in most

cases. For example, estimates of potential claim settlements may be impacted by the risk associated

with potential court rulings, but the final settlement agreement typically does not delineate how much

of the settled amount is due to this and other factors.

The evaluation of data is also subject to distortion from extreme events or structural shifts,

sometimes in unanticipated ways. For example, the timing of claims payments in one geographic region

will be impacted if claim adjusters are temporarily reassigned from that region to help settle

catastrophe claims in another region.

While some changes in the claim environment are sudden in nature (such as a new court ruling

affecting the interpretation of all contracts in that jurisdiction), others are more evolutionary.

Evolutionary changes can occur when multiple factors affect final claim values, with the uncertainty

surrounding each factor being resolved separately, in stepwise fashion. The final impact is not known

until all steps have occurred.

Sudden changes generally cause a one-time shift in claim liability estimates, although there may be

some lag in reliable quantification of their impact. Evolutionary changes generally cause a series of

shifts in claim liability estimates, as each component of the evolutionary change becomes evident and

estimable.

Actuarial methods for analyzing and estimating claims and claim adjustment expense reserves.

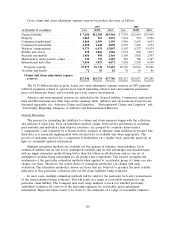

The principal estimation and analysis methods utilized by the Company’s actuaries are the paid

development method, the case incurred development method, the Bornhuetter-Ferguson (BF) method,

and average value analysis combined with the reported claim development method. The BF method is

usually utilized for more recent accident periods, with a transition to other methods as the underlying

claim data becomes more voluminous and therefore more credible. These are typically referred to as

traditional actuarial methods. (See Glossary for an explanation of these methods.)

While these are the principal methods utilized throughout the Company, those evaluating a

particular component for a product line have available to them the full range of methods developed

within the casualty actuarial profession. The Company’s actuaries are also continually monitoring

developments within the profession for advances in existing techniques or the creation of new

techniques that might improve current and future estimates.

Some components of product line reserves are susceptible to relatively infrequent large claims that

can materially impact the total estimate for that component. In such cases, the Company’s actuarial

analysis generally isolates and analyzes separately such large claims. The reserves excluding such large

claims are generally analyzed using the traditional methods described above. The reserves associated

with large claims are then analyzed utilizing various methods, such as:

• Estimating the number of large claims and their average values based on historical trends from

prior accident periods, adjusted for the current environment and supplemented with actual data

for the accident year analyzed to the extent available.

• Utilizing individual claim adjuster estimates of the large claims, combined with continual

monitoring of the aggregate accuracy of such claim adjuster estimates. (This monitoring may

lead to supplemental adjustments to the aggregate of such claim estimates.)

• Utilizing historic longer-term average ratios of large claims to small claims, and applying such

ratios to the estimated ultimate small claims from traditional analysis.

• Ground-up analysis of the underlying exposure (typically used for asbestos and environmental).

121