Target 2009 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2009 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

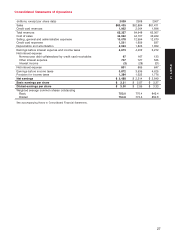

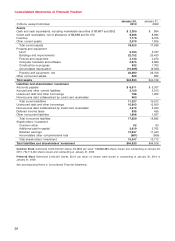

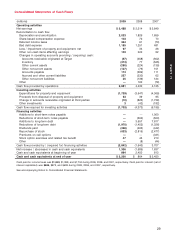

Item 7A. Quantitative and Qualitative Disclosures About Market Risk

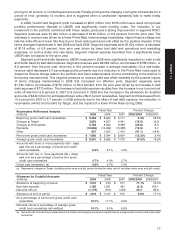

Our exposure to market risk results primarily from interest rate changes on our debt obligations, some of

which are at a LIBOR-plus floating rate, and on our credit card receivables, the majority of which are assessed

finance charges at a Prime-based floating rate. To manage our net interest margin, we generally maintain

levels of floating-rate debt to generate similar changes in net interest expense as finance charge revenues

fluctuate. The degree of floating asset and liability matching may vary over time and in different interest rate

environments. At January 30, 2010, the amount of floating-rate credit card assets exceeded the amount of net

floating-rate debt obligations by approximately $1 billion. As a result, based on our balance sheet position at

January 30, 2010, the annualized effect of a 0.1 percentage point decrease in floating interest rates on our

floating rate debt obligations, net of our floating rate credit card assets and marketable securities, would be to

decrease earnings before income taxes by approximately $1 million. See further description in Note 20 of the

Notes to Consolidated Financial Statements.

We record our general liability and workers’ compensation liabilities at net present value; therefore, these

liabilities fluctuate with changes in interest rates. Periodically, in certain interest rate environments, we

economically hedge a portion of our exposure to these interest rate changes by entering into interest rate

forward contracts that partially mitigate the effects of interest rate changes. Based on our balance sheet

position at January 30, 2010, the annualized effect of a 0.5 percentage point decrease in interest rates would

be to decrease earnings before income taxes by approximately $9 million.

In addition, we are exposed to market return fluctuations on our qualified defined benefit pension plans.

The annualized effect of a one percentage point decrease in the return on pension plan assets would

decrease plan assets by $22 million at January 30, 2010. The value of our pension liabilities is inversely related

to changes in interest rates. To protect against declines in interest rates we hold high-quality, long-duration

bonds and interest rate swaps in our pension plan trust. At year end, we had hedged approximately

50 percent of the interest rate exposure of our funded status.

As more fully described in Note 14 and Note 26 of the Notes to Consolidated Financial Statements, we are

exposed to market returns on accumulated team member balances in our nonqualified, unfunded deferred

compensation plans. We control the risk of offering the nonqualified plans by making investments in life

insurance contracts and prepaid forward contracts on our own common stock that offset a substantial portion

of our economic exposure to the returns on these plans. The annualized effect of a one percentage point

change in market returns on our nonqualified defined contribution plans (inclusive of the effect of the

investment vehicles used to manage our economic exposure) would not be significant.

We do not have significant direct exposure to foreign currency rates as all of our stores are located in the

United States, and the vast majority of imported merchandise is purchased in U.S. dollars.

Overall, there have been no material changes in our primary risk exposures or management of market

risks since the prior year.

24