Priceline 2015 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2015 Priceline annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

|

|

deferred merchant bookings and travel service provider payables seasonally depending on the absolute level of our merchant transactions during the last few weeks

of every quarter.

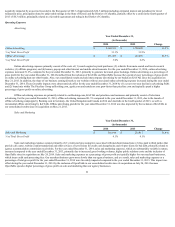

Net cash provided by operating activities for the year ended December 31, 2015 , was $3.1 billion , resulting from net income of $2.6 billion and a

favorable impact of $558.9 million for non-cash items not affecting cash flows, partially offset by net unfavorable changes in working capital and other assets and

liabilities of $8.0 million . The changes in working capital for the year ended December 31, 2015 , were primarily related to a $166.2 million increase in accounts

payable, accrued expenses and other current liabilities, offset by a $68.7 million increase in accounts receivable and $81.6 million increase in prepaid expenses and

other current assets. The increase in these working capital balances was primarily related to increases in business volumes. Non-cash items were primarily

associated with stock-based compensation expense, depreciation and amortization, amortization of debt discount and deferred income taxes.

Net cash provided by operating activities for the year ended December 31, 2014, was $2.9 billion, resulting from net income of $2.4 billion and a

favorable impact of non-cash items not affecting cash flows of $518.0 million, slightly offset by net unfavorable changes in working capital and other assets and

liabilities of $25.4 million. The changes in working capital for the year ended December 31, 2014, were primarily related to a $203.9 million increase in accounts

payable, accrued expenses and other current liabilities, offset by a $182.2 million increase in accounts receivable and $48.9 million increase in prepaid expenses

and other current assets. The increase in these working capital balances was primarily related to increases in business volumes. Non-cash items were primarily

associated with stock-based compensation expense, depreciation and amortization, amortization of debt discount and deferred income taxes.

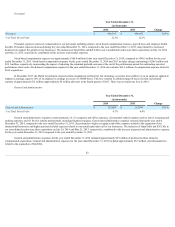

Net cash used in investing activities was $3.9 billion for the year ended December 31, 2015 . Investing activities for the year ended December 31, 2015

were affected by net purchases of investments of $3.6 billion , $140.3 million used for acquisitions, net of cash acquired, partially offset by net proceeds of $5.2

million for the settlement of foreign currency contracts. Net cash used in investing activities was $2.3 billion for the year ended December 31, 2014. Investing

activities for the year ended December 31, 2014 were affected by payments of $2.5 billion for acquisitions, net of cash acquired, and net cash payments of $80.3

million for the settlement of foreign currency contracts slightly offset by net sales of investments of $350.3 million and a change in restricted cash of $9.3 million.

Cash invested in the purchase of property and equipment was $173.9 million and $131.5 million in the years ended December 31, 2015 and 2014 , respectively.

The increase in 2015 was related to additional data center capacity and new offices to support growth and geographic expansion, principally related to our

Booking.com business.

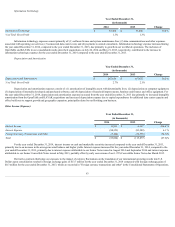

Net cash used in financing activities was $730.0 million for the year ended December 31, 2015 . Cash used in financing activities for the year ended

December 31, 2015 primarily consisted of treasury stock purchases of $3.1 billion , payments of $147.6 million related to the conversion of Senior Notes and

payment of $10.7 million related to the settlement of the acquisition-date estimated contingent liability related to an acquisition, primarily offset by the total

proceeds of $2.4 billion from the issuance of Senior Notes, excess tax benefits on stock-based awards of $101.5 million and the exercise of employee stock options

of $20.9 million . Net cash provided by financing activities was approximately $1.4 billion for the year ended December 31, 2014. Cash provided by financing

activities for the year ended December 31, 2014 primarily consisted of total proceeds of $2.3 billion from the issuance of Convertible Senior Notes and Euro

denominated Senior Notes, excess tax benefits on stock-based awards of $23.4 million and the exercise of employee stock options of $16.4 million, partially offset

by treasury stock purchases of $750.4 million and payments of $125.1 million related to the conversion of Senior Notes.

Contingencies

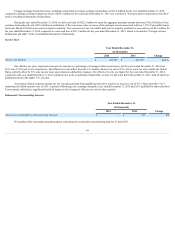

French tax authorities recently concluded an audit that started in 2013 of the years 2003 through 2012 to determine whether Booking.com is in

compliance with its tax obligations in France, and Booking.com received a formal assessment in December 2015. While we believe that Booking.com has been,

and continues to be, in compliance with French tax law, as a result of the audit the French tax authorities claim that Booking.com has a permanent establishment in

France and seek to recover unpaid income taxes and VAT of approximately 356 million Euros, the majority of which would represent penalties and interest. We

intend to contest any such assessment. If we are unable to resolve the matter with the French authorities, we would expect to challenge the assessment in the

French courts. In order to contest the assessment in court, we may be required to pay, upfront, the full amount or a significant part of any such assessment, though

any such payment would not constitute an admission by us that we owe the taxes. French authorities may decide to also audit subsequent tax years, which could

result in additional assessments. See Part I Item IA Risk Factors - " We may have exposure to additional tax liabilities. "

A number of U.S. jurisdictions have initiated lawsuits against online travel companies, including us, related to, among other things, the payment of travel

transaction taxes (e.g., hotel occupancy taxes, excise taxes, sales taxes, etc.). In addition, a number of U.S. states, counties and municipalities have initiated audit

proceedings, issued proposed tax assessments or started

66