PG&E 2011 Annual Report Download - page 98

Download and view the complete annual report

Please find page 98 of the 2011 PG&E annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

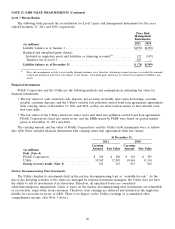

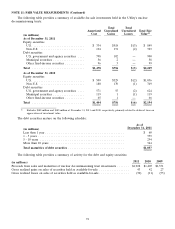

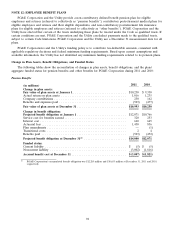

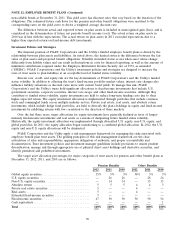

NOTE 12: EMPLOYEE BENEFIT PLANS (Continued)

Components of Net Periodic Benefit Cost

Net periodic benefit cost as reflected in PG&E Corporation’s Consolidated Statements of Income for the year

ended December 31, 2011, 2010, and 2009 is as follows:

Pension Benefits

2011 2010 2009

(in millions)

Service cost for benefits earned ................................ $320 $279 $259

Interest cost .............................................. 660 645 624

Expected return on plan assets ................................ (669) (624) (579)

Amortization of prior service cost .............................. 34 53 53

Amortization of unrecognized loss .............................. 50 44 101

Net periodic benefit cost ................................... 395 397 458

Less: transfer to regulatory account(1) .......................... (139) (233) (294)

Total ................................................. $ 256 $ 164 $ 164

(1) The Utility recorded $139 million, $233 million, and $295 million for the years ended December 31, 2011, 2010, and 2009,

respectively, to a regulatory account as the amounts are probable of recovery from customers in future rates.

Other Benefits

2011 2010 2009

(in millions)

Service cost for benefits earned .................................. $ 42 $ 36 $30

Interest cost ............................................... 91 88 87

Expected return on plan assets .................................. (82) (74) (68)

Amortization of transition obligation .............................. 26 26 26

Amortization of prior service cost ................................ 27 25 16

Amortization of unrecognized loss (gain) ........................... 4 3 3

Net periodic benefit cost ....................................... $108 $104 $ 94

There was no material difference between PG&E Corporation and the Utility for the information disclosed

above.

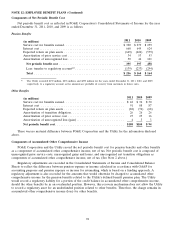

Components of Accumulated Other Comprehensive Income

PG&E Corporation and the Utility record the net periodic benefit cost for pension benefits and other benefits

as a component of accumulated other comprehensive income, net of tax. Net periodic benefit cost is composed of

unrecognized prior service costs, unrecognized gains and losses, and unrecognized net transition obligations as

components of accumulated other comprehensive income, net of tax. (See Note 2 above.)

Regulatory adjustments are recorded in the Consolidated Statements of Income and Consolidated Balance

Sheets to reflect the difference between pension expense or income calculated in accordance with GAAP for

accounting purposes and pension expense or income for ratemaking, which is based on a funding approach. A

regulatory adjustment is also recorded for the amounts that would otherwise be charged to accumulated other

comprehensive income for the pension benefits related to the Utility’s defined benefit pension plan. The Utility

would record a regulatory liability for a portion of the credit balance in accumulated other comprehensive income,

should the other benefits be in an overfunded position. However, this recovery mechanism does not allow the Utility

to record a regulatory asset for an underfunded position related to other benefits. Therefore, the charge remains in

accumulated other comprehensive income (loss) for other benefits.

94